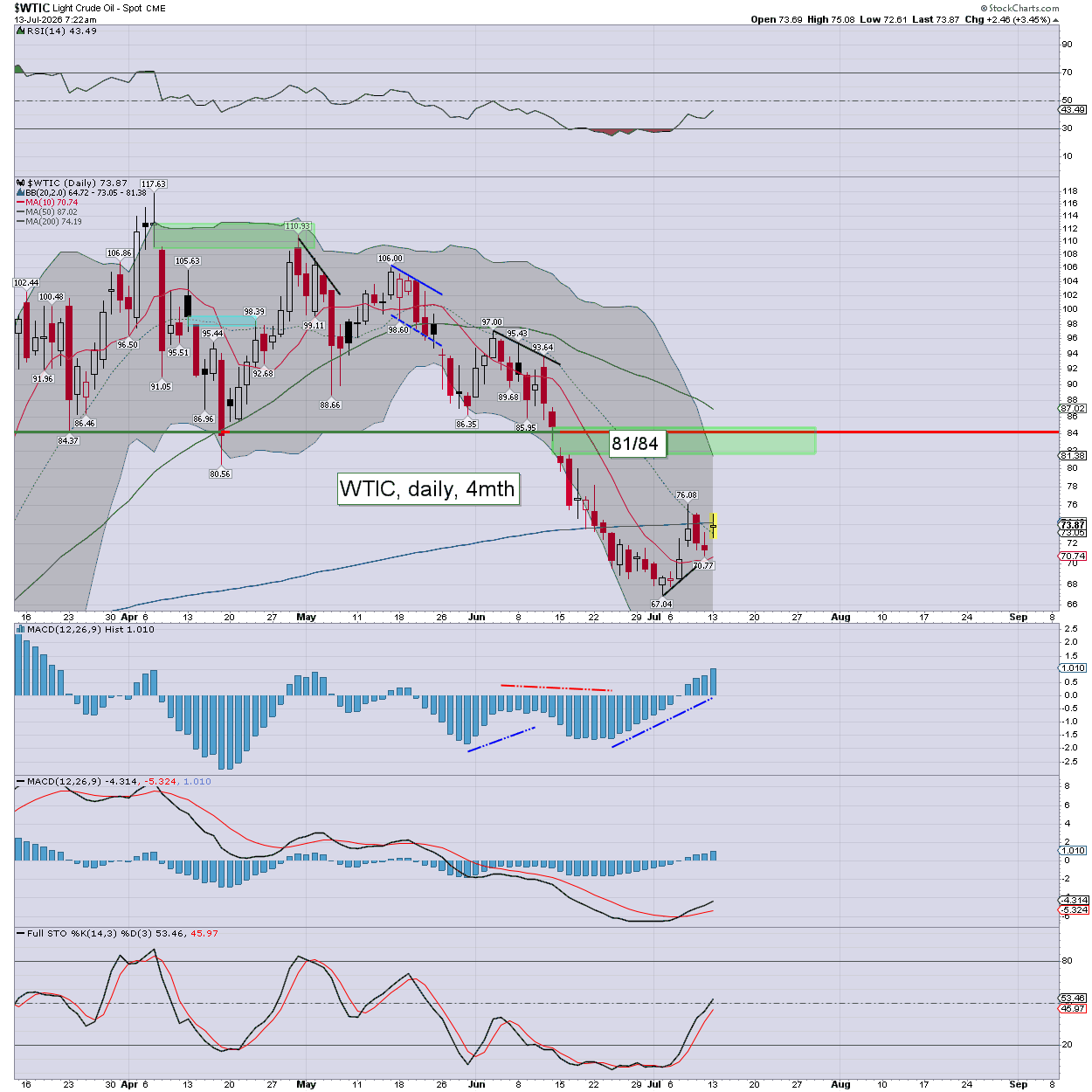

Good morning. US equity futures are leaning weak, SPX -20pts, we’re set to open at 7555. USD is -0.04% at DXY 100.72. The precious metals are sig’ lower, Gold -1.1%, with Silver -2.0%. WTIC is +3.4% at $73.87.

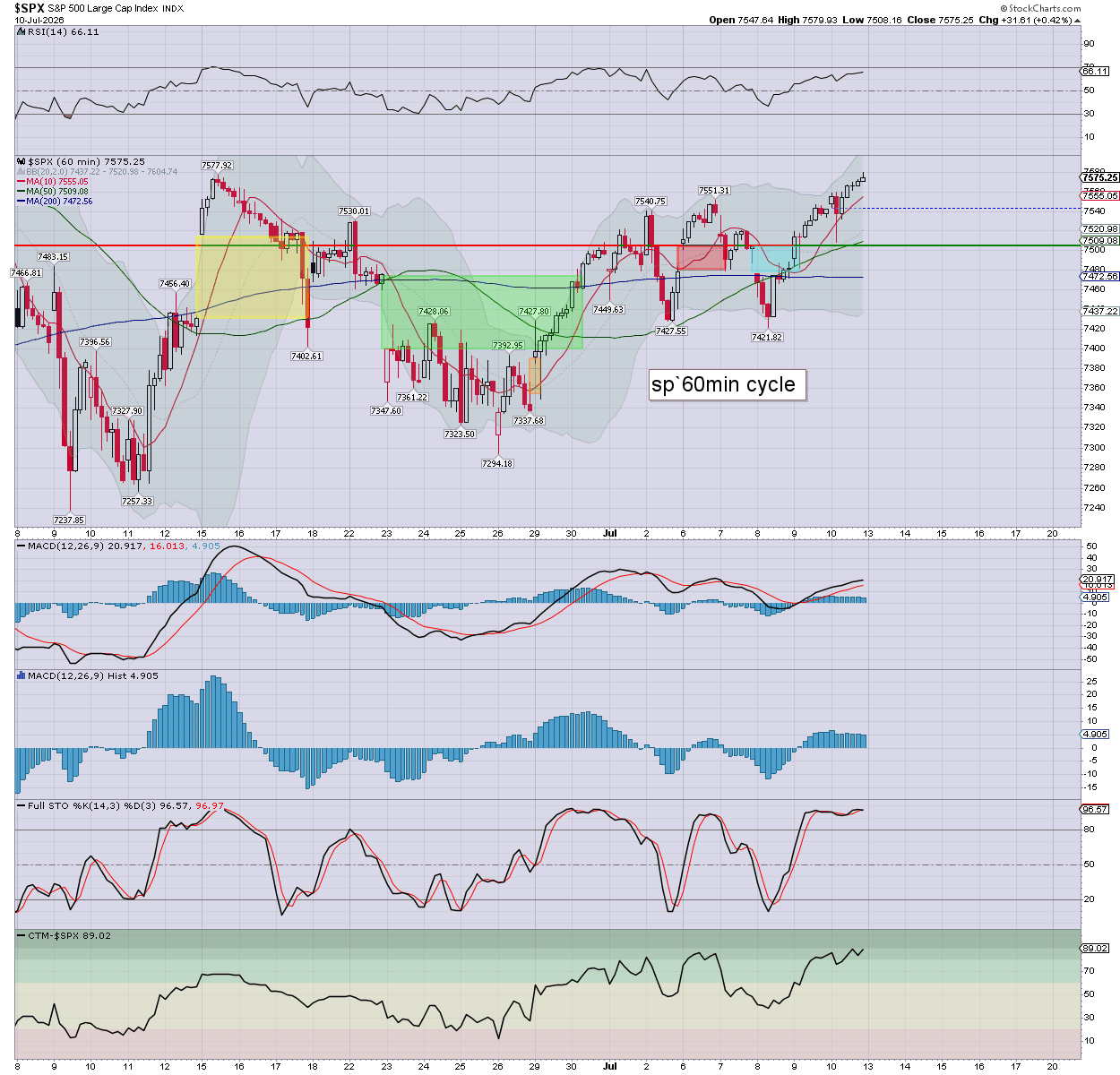

sp’60min

WTIC, daily

Oil is naturally higher on weekend attacks. For now though, its still relatively minor, and the market is not taking any of it seriously. S/t structure of a bull flag is playing out though, and I’d be open to 81/84 within a few days.

—

Summary

Last week ended on a positive note, with the SPX settling just 45pts below the recent hist’ high of 7620. S/t momentum settled moderately positive.

Overnight futures have been leaning weak, pressured by weekend war headlines, and South Korea. We’re set to open -20pts or so.

Yours truly did not complete my accounts this weekend, and I’ve no business doing anything until that is done.

—

Early movers

AAPL +0.2%

AG -1.5%

AMAT -3.6%, Mr Burry will be pleased.

AMD -2.1%

ASTS -1.2%

BAC +0.2%, earnings early Tues’

CDE -1.2%

–

COIN -0.9%

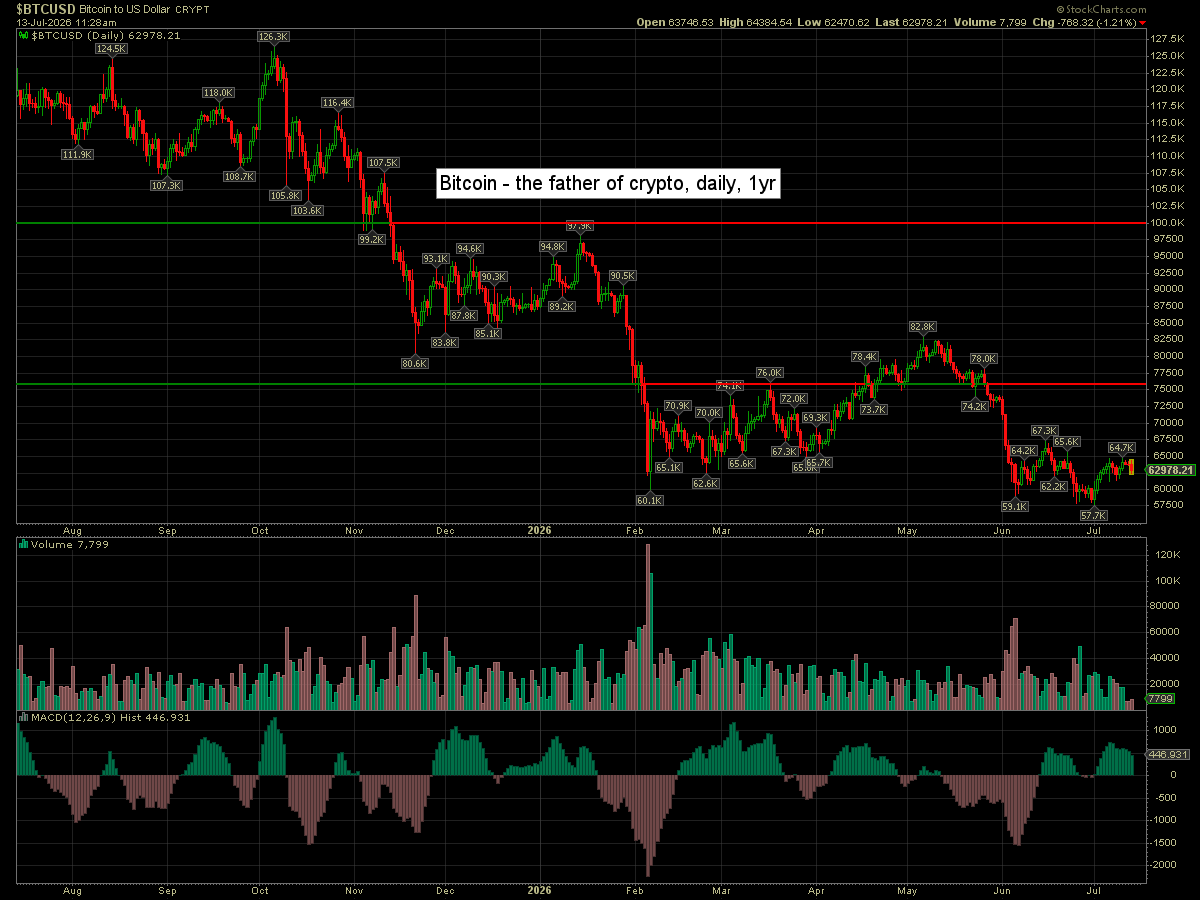

Bitcoin is -1.2% at $62K. S/t cyclically high, and prone to net downside for at least a few days.

–

CVX +1.0%

HL -1.4%

INTC -2.7%

IREN -2.0%

JPM +0.2%, earnings early Tues’

–

MGM +2.4%, deal talks with Barry Diller

MSTR -2.0%

MU -4.3%

NEM -0.6%

NFLX +0.4%, earnings Thurs’ AH

NOK -0.3%

NVDA -1.2%

–

OXY +1.7%

PAAS -0.4%

RKLB -0.5%

SHOP +2.6%, Jefferies, hold>buy, 140>160

–

SKHY ** , ticker change from SKHYV

–

SNDK -4.5%

SPCX -0.8%

STX -3.4%

TSLA -0.6%

UAL -0.3%

UNG -2.0%, with Natgas $2.88

–

VIX +8.4% at 16.30

–

WDC -4.7%

XOM +1.1%

—

Overnight markets

Asian had a very rough start to the week, whilst Europe is flat lining. The disparity is … odd.

Japan: -1.9% to 67242

China: -2.1% to 3913

South Korea: -8.9% to 6806

–

Germany: currently +0.14% at 25102

France: currently +0.02% at 8340

UK: currently -0.15% at 10481

—

Today will be an Open Day, with my posts available to all.

Its the best (and free) type of advertising I can get.

Have a good Monday