Good morning. US equity futures are a little higher (ahead of CPI), SPX +13pts, we’re set to open at 6545. USD is +0.2% at DXY 97.60. The precious metals are moderately lower, Gold -0.5%, with Silver -0.4%. WTIC is -0.9% in the low $63s.

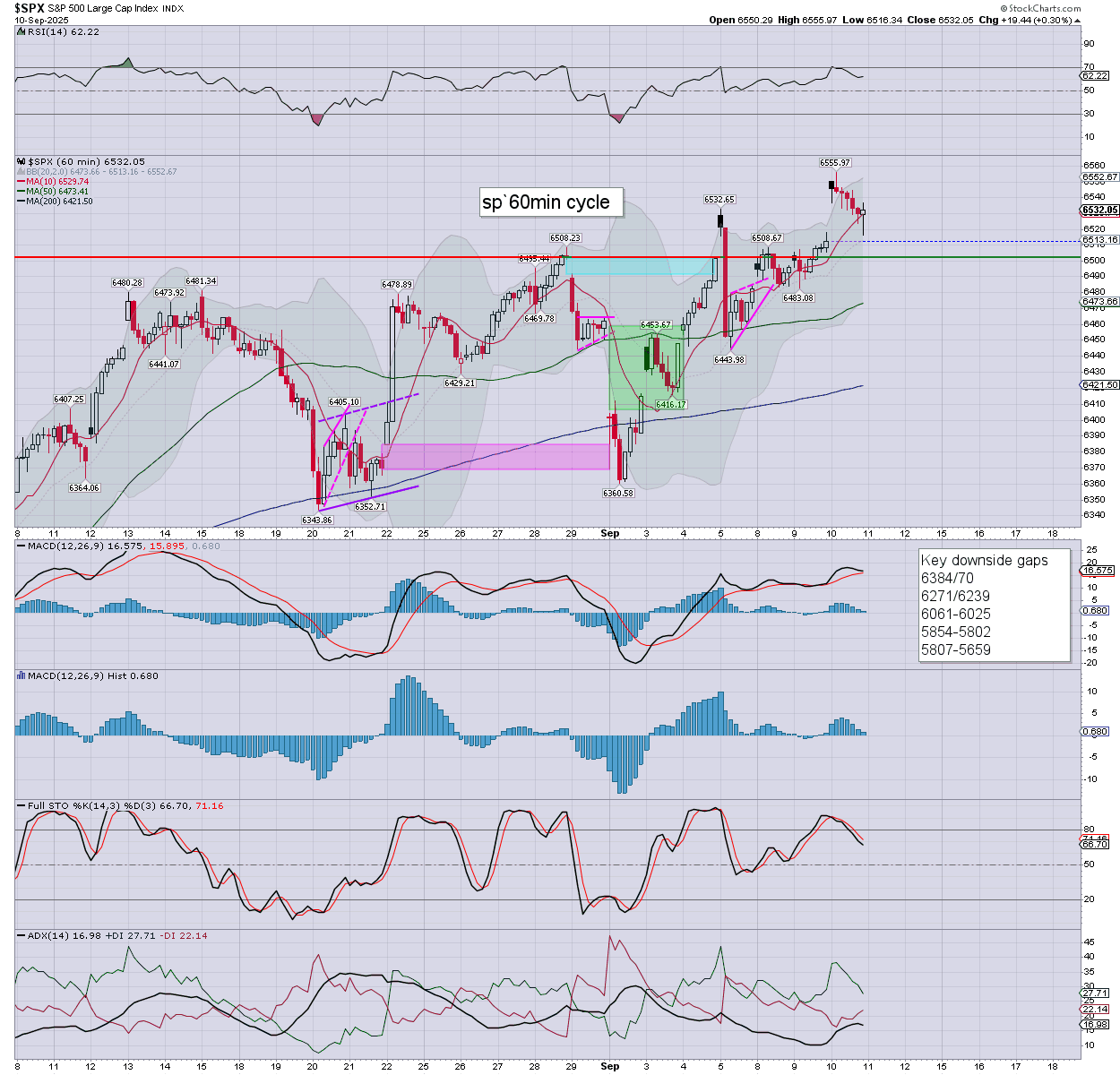

sp’60min

Summary

Yesterday saw a new hist’ high of 6555, if cooling back to settle at 6532. S/t momentum weakened across the afternoon, settling fractionally positive.

Overnight futures have been subdued, if leaning upward… especially helped by Asian markets.

There appears little reason not to expect 6555 to be printed above… whether today or before the Fed.

Even the bolder bears are going to sit back until next Wed’, 2.05pm, and then re-assess. The smarter bulls are arguably just raising their stops.

The notion of a ‘straight run up’ into year end/early 2026 is ludicrous. I have to expect a multi-week washout… if only to around SPX 6K.

The CPI is due 8.30am EDT, consensus:

Headline y/y: 2.9% vs 2.7% prior

Core y/y: 3.1% vs 3.1% prior

Even if inflation is above estimates, its clear that the Fed will still cut rates by -25bps next week. I expect a ‘sell the news’ outcome, regardless of the decision, and whatever Powell might say.

—

Early movers

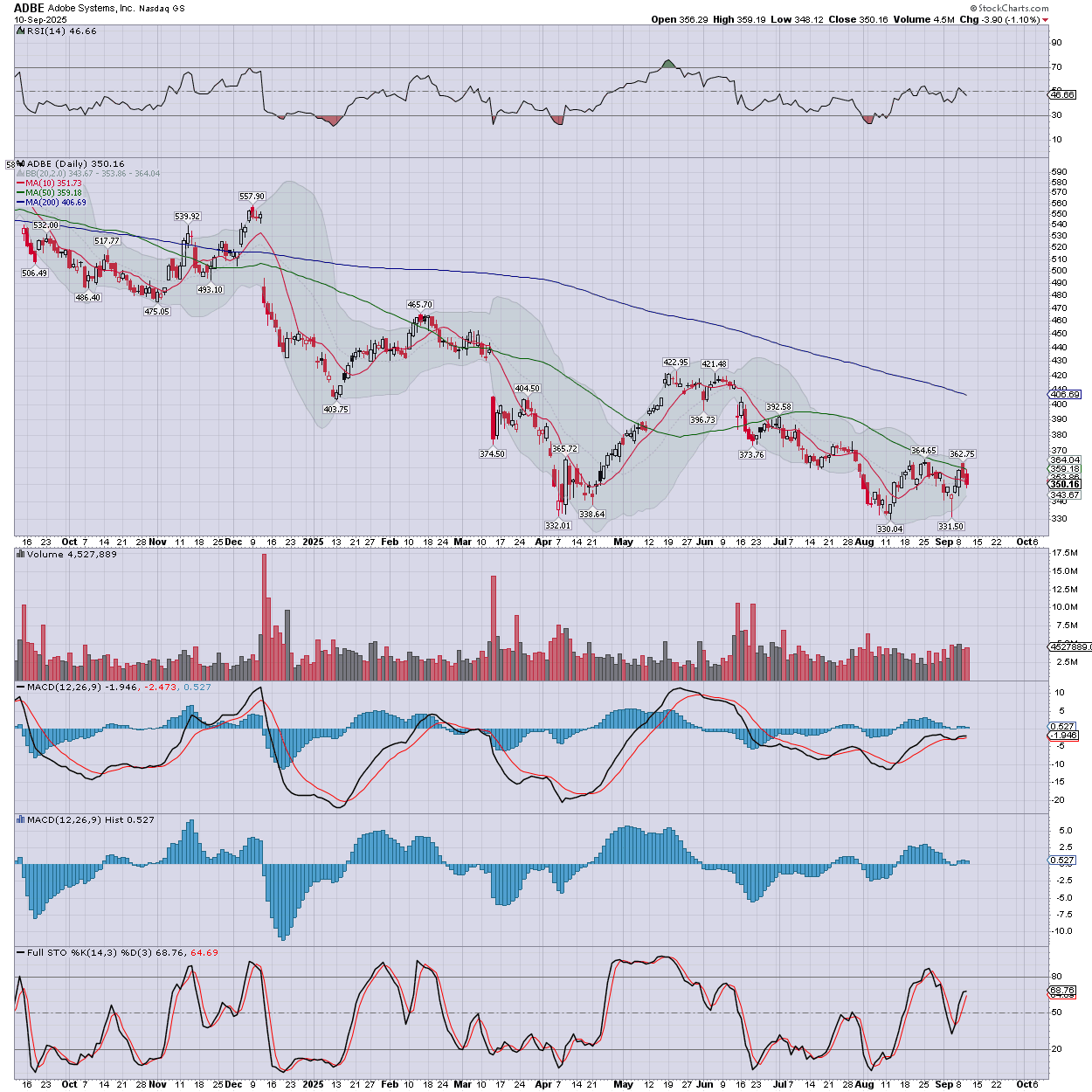

ADBE +2.1%, earnings due in AH

The technical setup favours the bears, for what is m/t horror from the Jan’2024 $638s.

–

AMD -1.2%

AMZN +0.7%

BABA +2.6%, strong China stocks

BMNR +4.8%

CELH +2.4%, Goldman, buy, $72

CNC +3.6%

–

COIN +0.8%

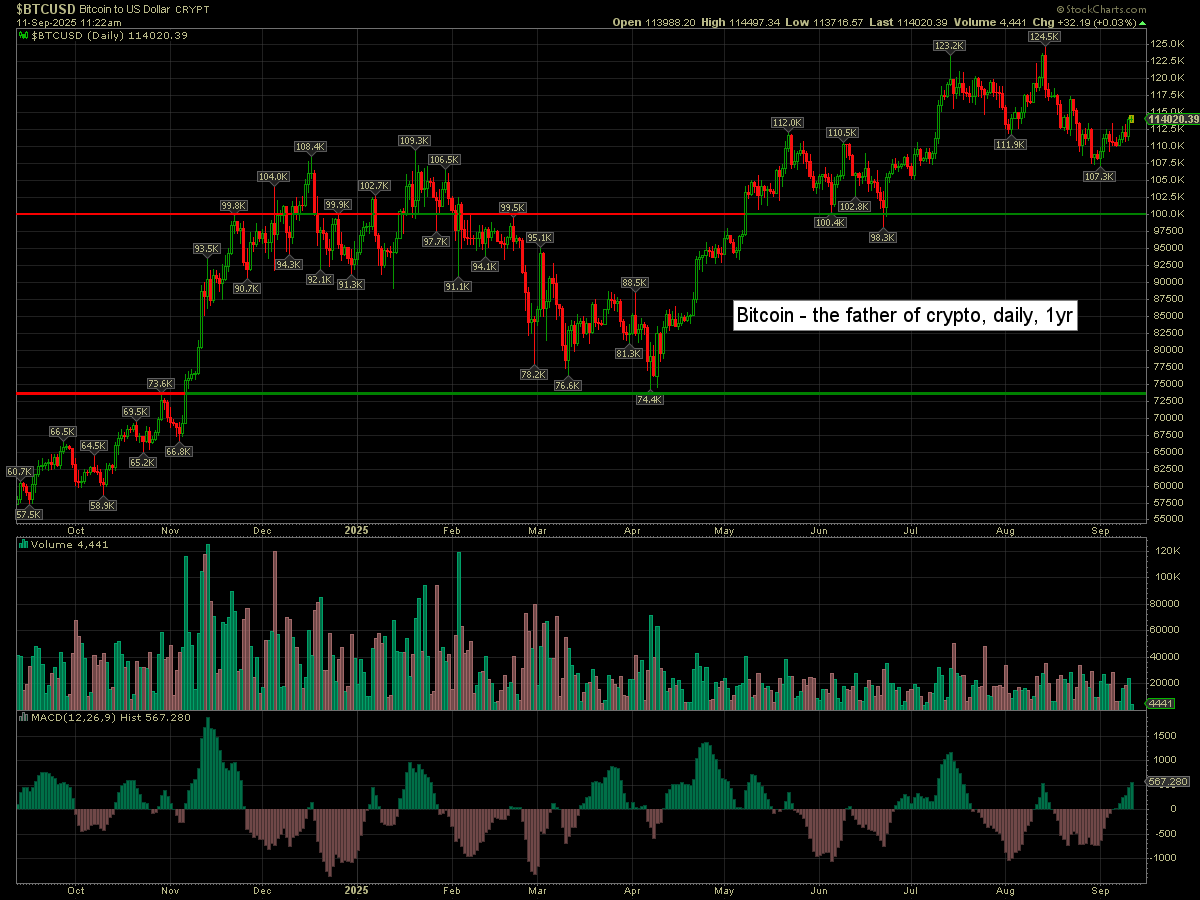

Bitcoin is fractionally higher, +$32 at $114K

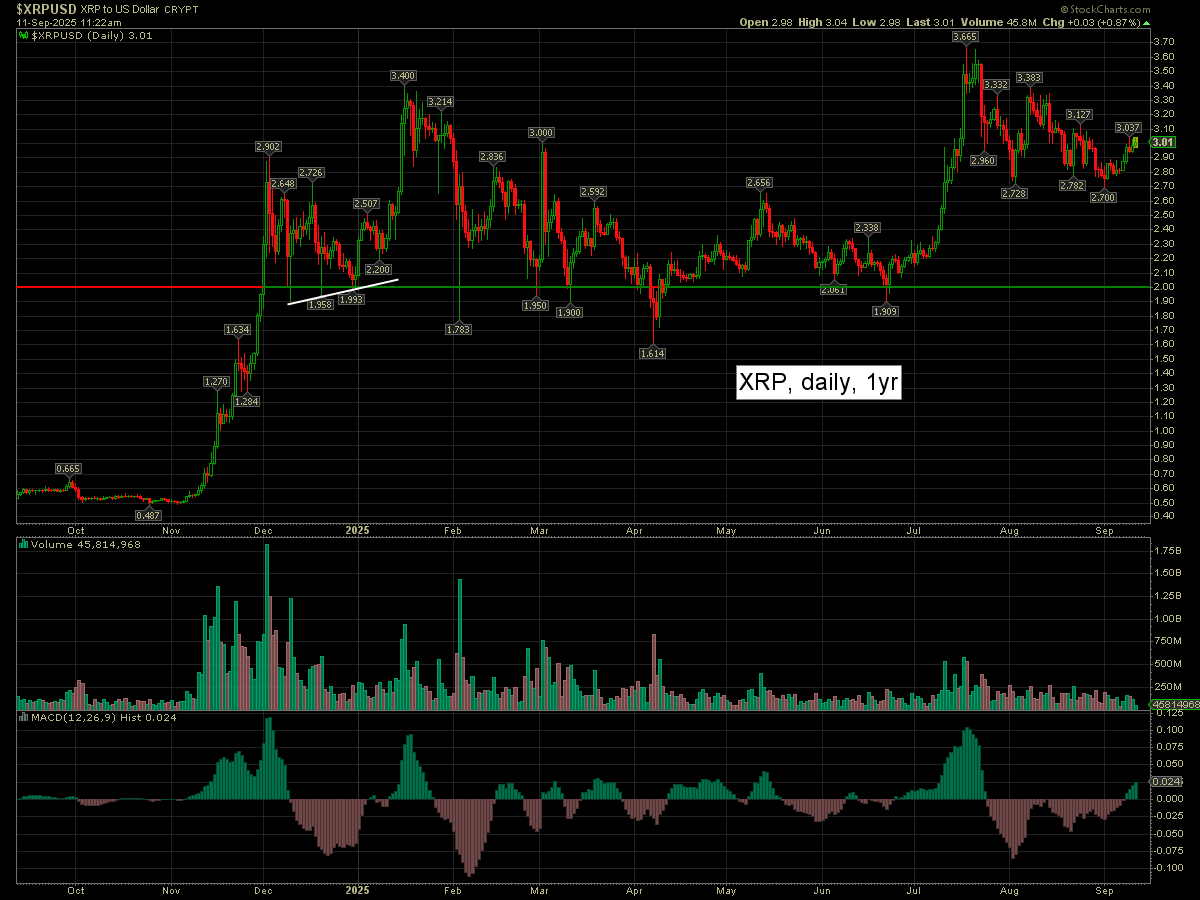

XRP is +3cents at $3.01. I’d look for post Fed cooling into mid Oct’

–

CRWV +2.6%

CWD -6.6%, fading hysteria

–

ENVX -16.0%, $300M convert’ corp’ debt offering

–

FDX -1.0%, BofA, buy>neutral, 245>240

GME -1.3%… yesterday’s black candle to play out

JOBY +2.0%

–

KLAR -1.5%, day two. A filthy UK financial… to be left well alone.

–

MU +2.4%, Citi, buy, 150>175

NEM -0.7%

NIO +1.6%

NVDA +0.5%

–

NVO -1.0%

OCTO -7.1%, fading hysteria

ONDS +2.3%

–

RCAT +8.0%, the ‘Black widow’ drone has been added to the ‘NATO catalogue’. Just reflect on the latter notion for a moment… as the blood thirsty psychos flip through the pages of a catalogue… shopping for weapons to kill.

–

SMR +2.1%

–

SWBI +3.7%, as assassinations are a positive for gun sellers

–

TSLA +1.2%

–

UPS -1.7%, BofA, neutral>underperform, 91>83.

The stock remains l/t horror from the Feb’2022 $197s.

My target remains $75, as looks realistic in October.

–

VIX -1.5% at 15.12

–

XPEV +1.0%, strong China stocks

—

Overnight markets

Asian markets were sig’ higher, whilst European markets are leaning upward…

Japan: +1.2% to 44372… a new historic high.

China: +1.6% to 3875

Germany: currently +0.2% at 23672

UK: currently +0.5% at 9272

—

Have a good Thursday