Good morning. US equity futures are flat, SPX u/c, we’re set to open at 6263. USD is -0.1% at DXY 97.11. The precious metals are broadly higher, Gold +0.3%, with Silver +1.1%. WTIC is -0.5% in the low $68s.

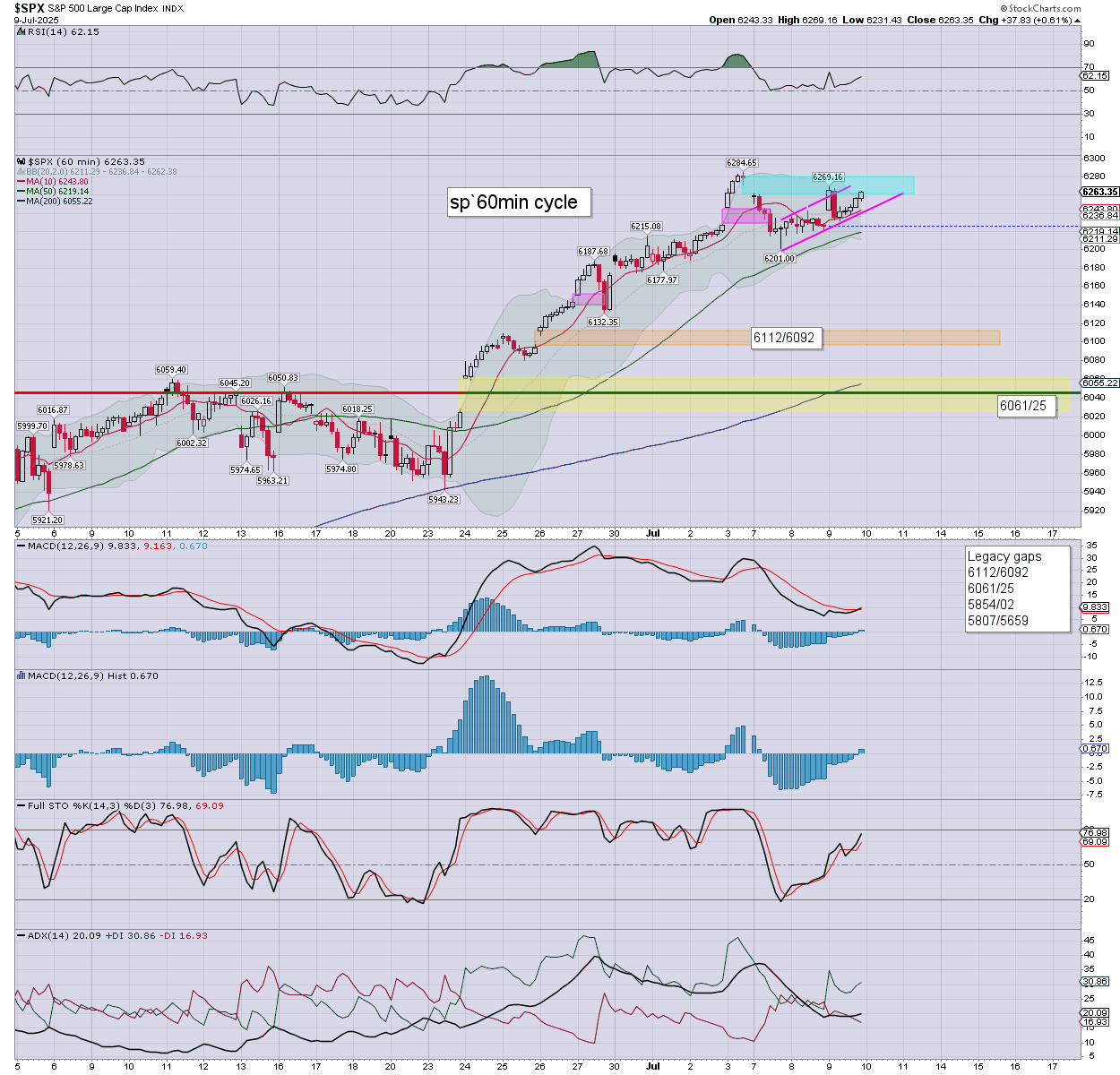

sp’60min

Summary

Yesterday saw an opening downside reversal, but there was no follow through, with a secondary push upward to settle moderately higher. S/t momentum turned fractionally positive.

Overnight futures have been subdued, we’re set to open flat. The s/t cyclical setup marginally favours the bears.

—

Early movers

AAL +7.1%, pulled upward by Delta

AAPL -0.5%, as Lightshed Partners argue (on CNBC) CEO Cook should be replaced

–

AEM +0.3%

AMD +1.6%, HSBC, hold>buy, 100>200

–

CAG -3.0%, EPS 56cents vs 58est. Rev’ y/y -4.3% to $2.78bn vs 2.83est. The annual drop in sales is worse… considering inflation.

–

CLF +2.6%

–

COIN +0.1%, Wainwright, buy>sell, 305>300

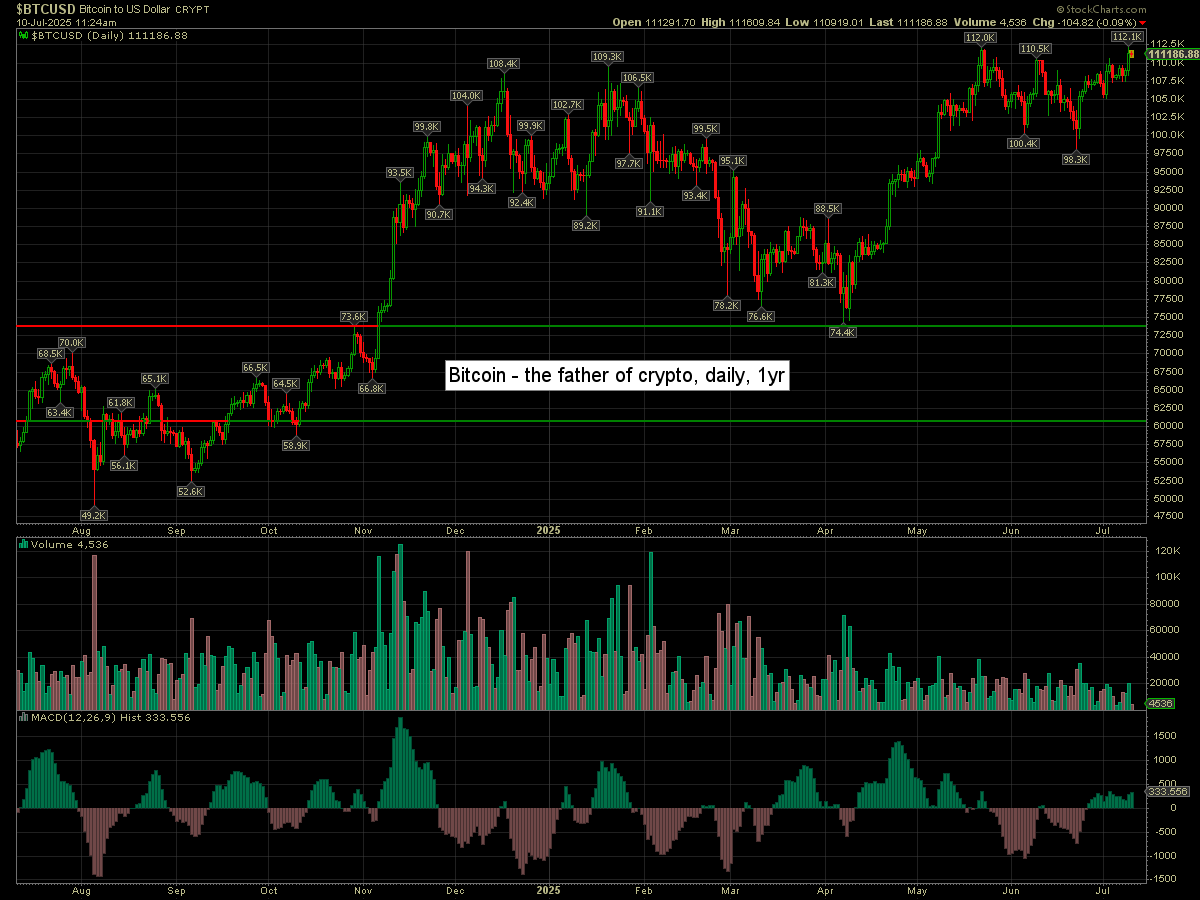

Bitcoin printed a new hist’ high of $112007, if currently -0.1% at $111K

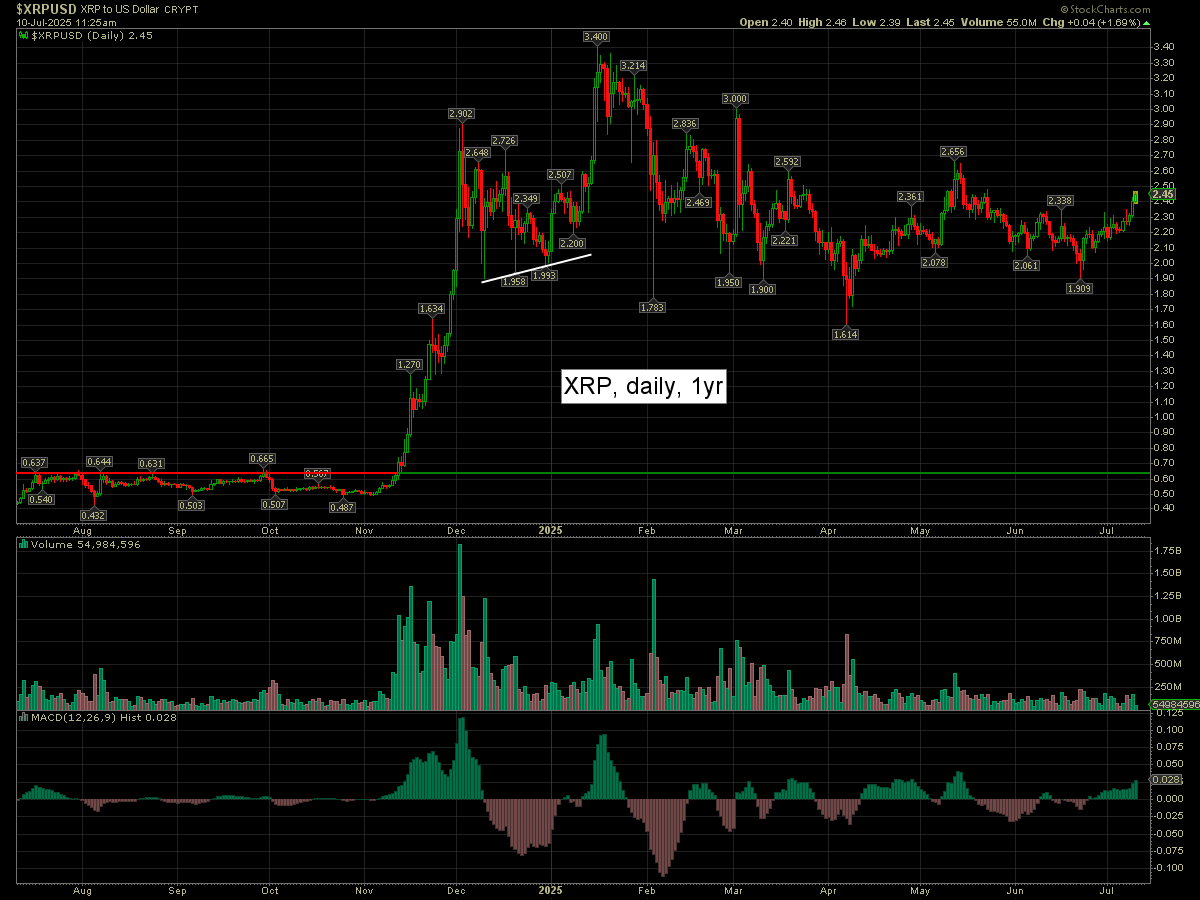

XRP is +4cents at $2.45

–

CRCL +2.8%, working with Jack Ma’s Ant group

CRSP +5.0%

–

DAL +11.9%, EPS $2.10 vs 2.05est. Rev’ y/y -0.1% to $16.65bn vs 15.45est. F/y guidance restored. Delta argues demand has stabilised, if remaining soft.

–

ERJ -5.6%

FCX +2.6%, with copper +14cents to $5.62

INTC +0.5%

KLG +52.0%, chatter that Ferrero might buy WK Kellog

–

MBLY -3.9%, Intel is selling its stake

–

MP +40.4%, DoD contract for rare earths

NEM +0.5%

NVDA +0.8%

–

RIO +3.3%, higher copper

ROKU +2.7%, Keybanc, sector-weight>overweight, $115

SCCO +2.0%, copper

–

SMPL -3.5%, EPS 51cents vs 50est. Rev’ y/y +13.8% to $380.9M vs 381.7est.

–

T -1.0%, dragged down by T-Mobile

TSLA +1.1%

UAL +7.9%, pulled upward by sister Delta

–

VIX +0.2% at 15.98

–

VZ -1.6%, dragged down by T-Mobile

WDAY -1.7%, Piper Sandler, neutral>underweight, 255>235

—

Overnight markets

Asian markets were moderately mixed, whilst European markets are broadly mixed…

Japan: -0.4% to 39646

China: +0.5% to 3509

Germany: currently +0.1% at 24575

UK: currently +1.2% at 8971

—

Have a good Thursday