Good morning. US equity futures are moderately lower, SPX -30pts, we’re set to open at 5910. USD is -0.5% at DXY 99.44. The precious metals are mixed, Gold +0.5%, with Silver u/c. WTIC is +0.3% in the mid $62s (printing $64.19).

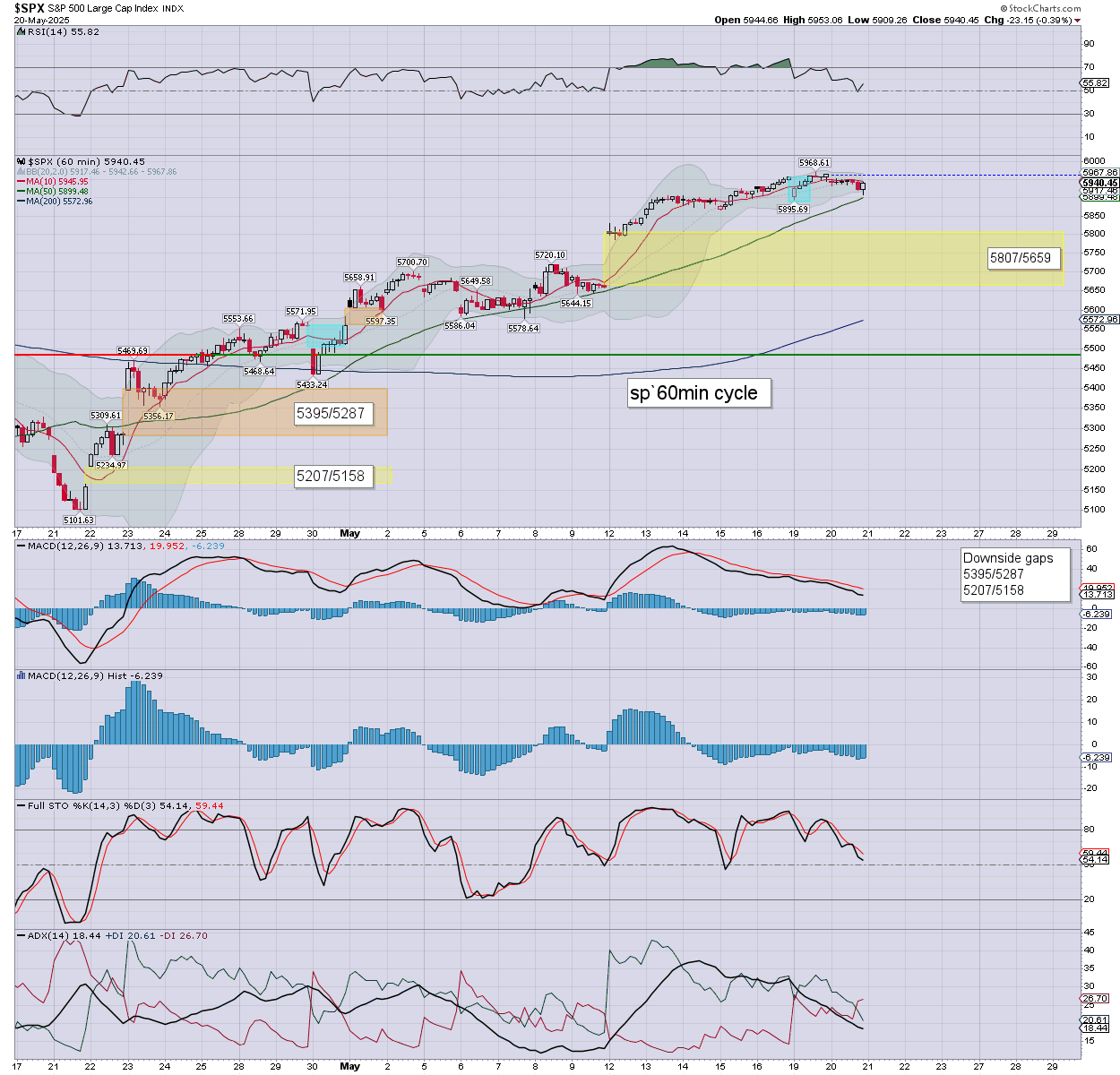

sp’60min

Summary

Yesterday saw weak leaning chop. S/t momentum settled on the moderately negative side.

Overnight futures have been leaning weak, we’re set to open -30pts or so. Basic target remains a tag of yellow gap… that begins at 5807.

Thursday threatens some drama, with daily VIX momentum prone to turning positive. I’d keep in mind Friday will likely be subdued… as its the lead into a three day weekend. So if the bears are going to get anything… it’ll be tomorrow.

—

Early movers

AAPL -0.3%

AFRM -1.2%

AG +0.7%

AMZN -0.8%

ASTS -0.9%

B +0.7%

–

BIDU +2.3%, EPS $2.55 vs 1.96est. Rev’ y/y +2.4% to $4.47bn vs 4.30est.

–

CLF -0.5%

–

COIN +0.2%

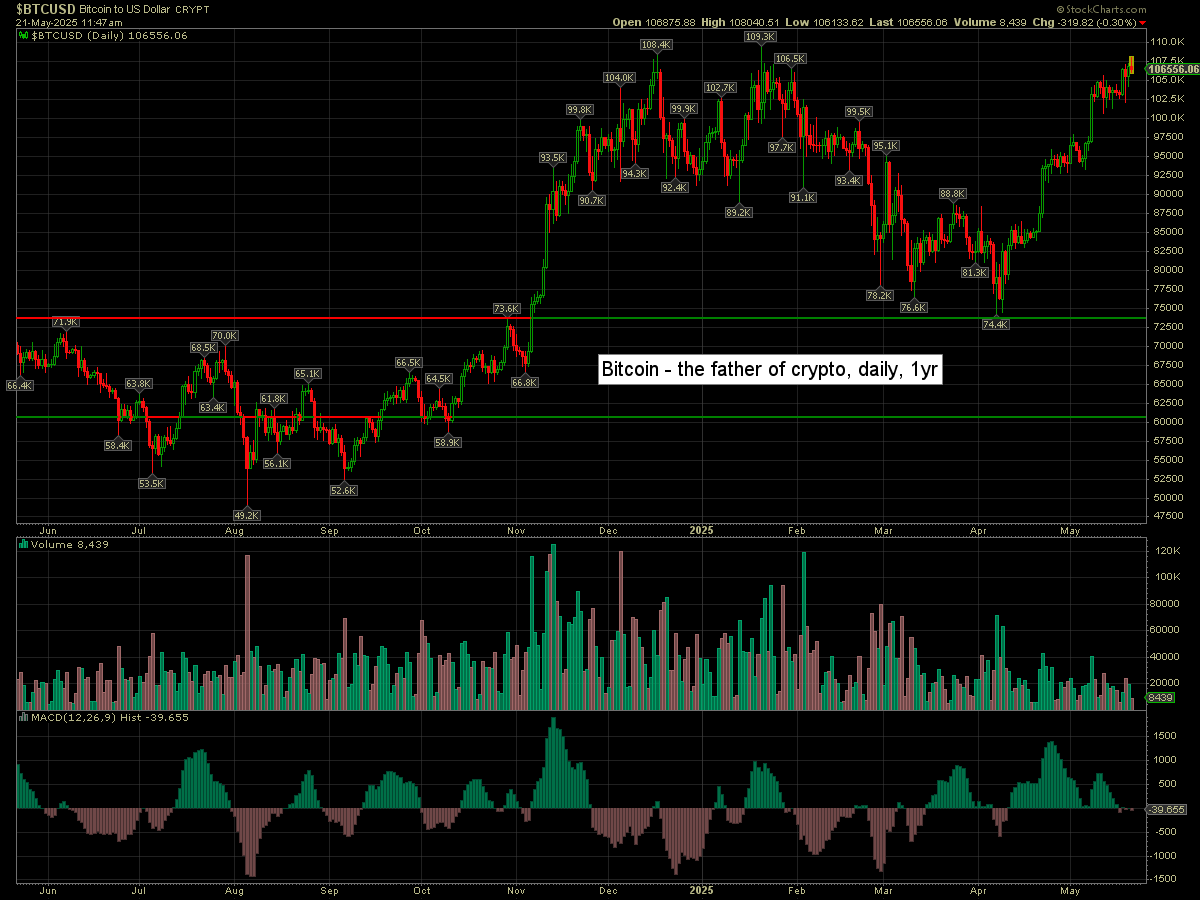

Bitcoin printed a new cycle high of $108K, if currently -0.3% at $106K

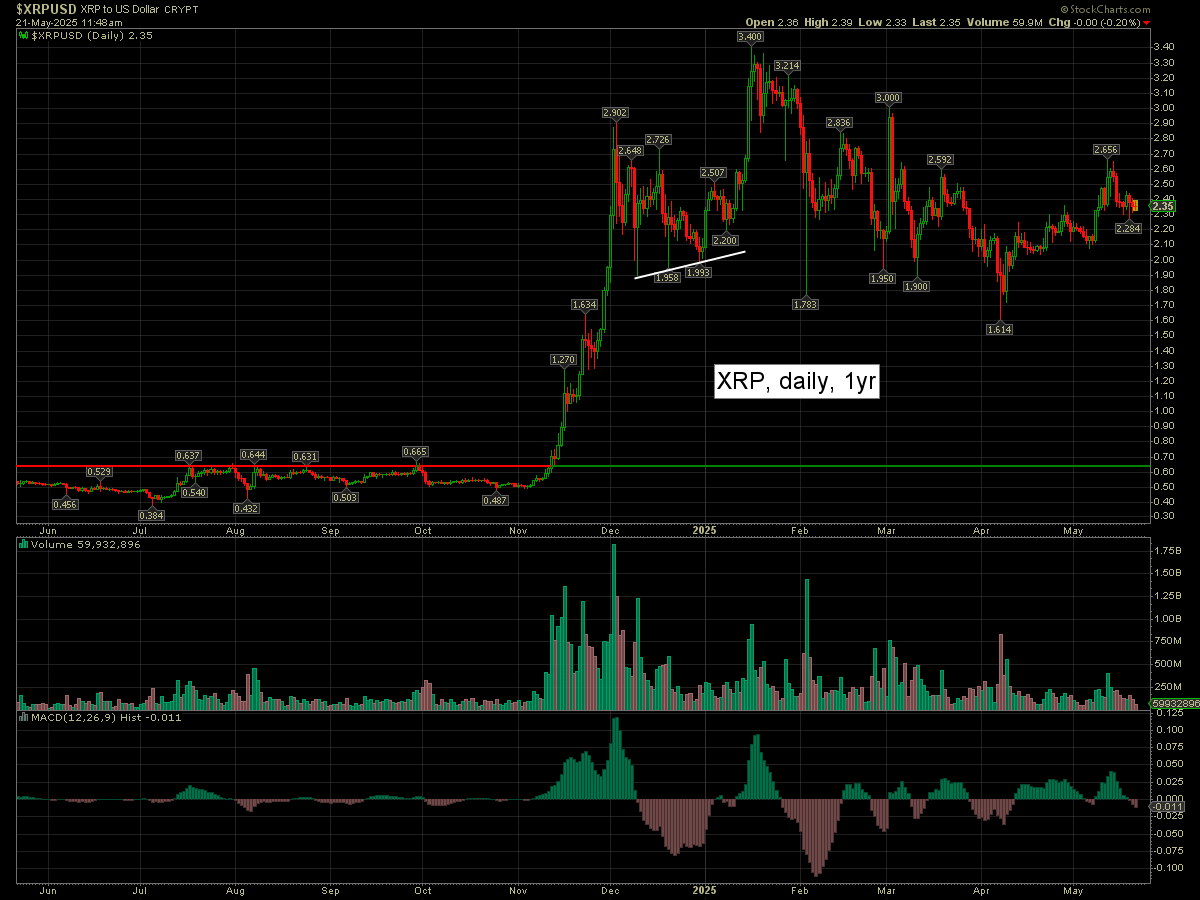

XRP is u/c at $2.35. I’ve no interest in buying unless <$2.20, with SPX around 5800.

–

GOOGL +0.4%, Loop Capital excited about ‘Smartglasses’

LMT +1.1%, background war drums?

–

MDT -1.2%, EPS $1.62 vs 1.58est. Rev’ y/y +3.9% to $8.93bn vs 8.82est. Medtronic plans to spin off its Diabetes business.

–

NVDA -0.9%

OXY +0.3%

–

PANW -3.9%, earnings (Tues’ AH), EPS 80cents vs 77est. Rev’ y/y +15.3% to $2.29bn vs 2.28est. Positive guidance… but the market still isn’t satisfied.

–

RTX +1.4%

SMR -1.2%

–

TGT -3.4%, EPS $1.30 vs 1.64est. Rev’ y/y -2.8% to $23.85bn vs 24.32est. A double miss. Guidance cut, with Target warning ‘tariffs remain a headwind’ The annual decline in sales isn’t exactly a surprise… as the consumer is BROKEN

–

TJX -1.6%, EPS 92cents vs 90est. Rev’ y/y +5.1% to $13.11bn vs 13.00est. COMPS +3.0%

–

TOL +3.8%, EPS $3.50 vs 2.83est. Rev’ y/y -4.5% to $2.71bn vs 2.48est. COMPS -3.8%

–

TSLA +0.7%

–

TTWO -4.0%, $1bn secondary offering… to help pay to finish GTA VI ?

–

UAL -0.9%

UNG +1.9%, with Natgas $3.45

UNH -6.5%

–

VIX +2.6% at 18.55

–

XPEV +5.1%, EPS -6cents vs -21est. Rev’ $2.18bn vs 0.906 prior yr.

–

WRD +2.5%

—

Overnight markets

Asian markets were a little mixed, whilst European markets are a touch lower…

Japan: -0.6% to 37298

China: +0.2% to 3387

Germany: currently -0.2% at 23985

UK: currently -0.05% at 8776

—

Have a good Wednesday