Good morning. US equity futures are very significantly lower, SPX -100pts, we’re set to open at 5356. USD is -1.0% at DXY 101.56. The precious metals are mixed, Gold +0.6%, with Silver -0.2%. WTIC is -2.7% in the mid $60s.

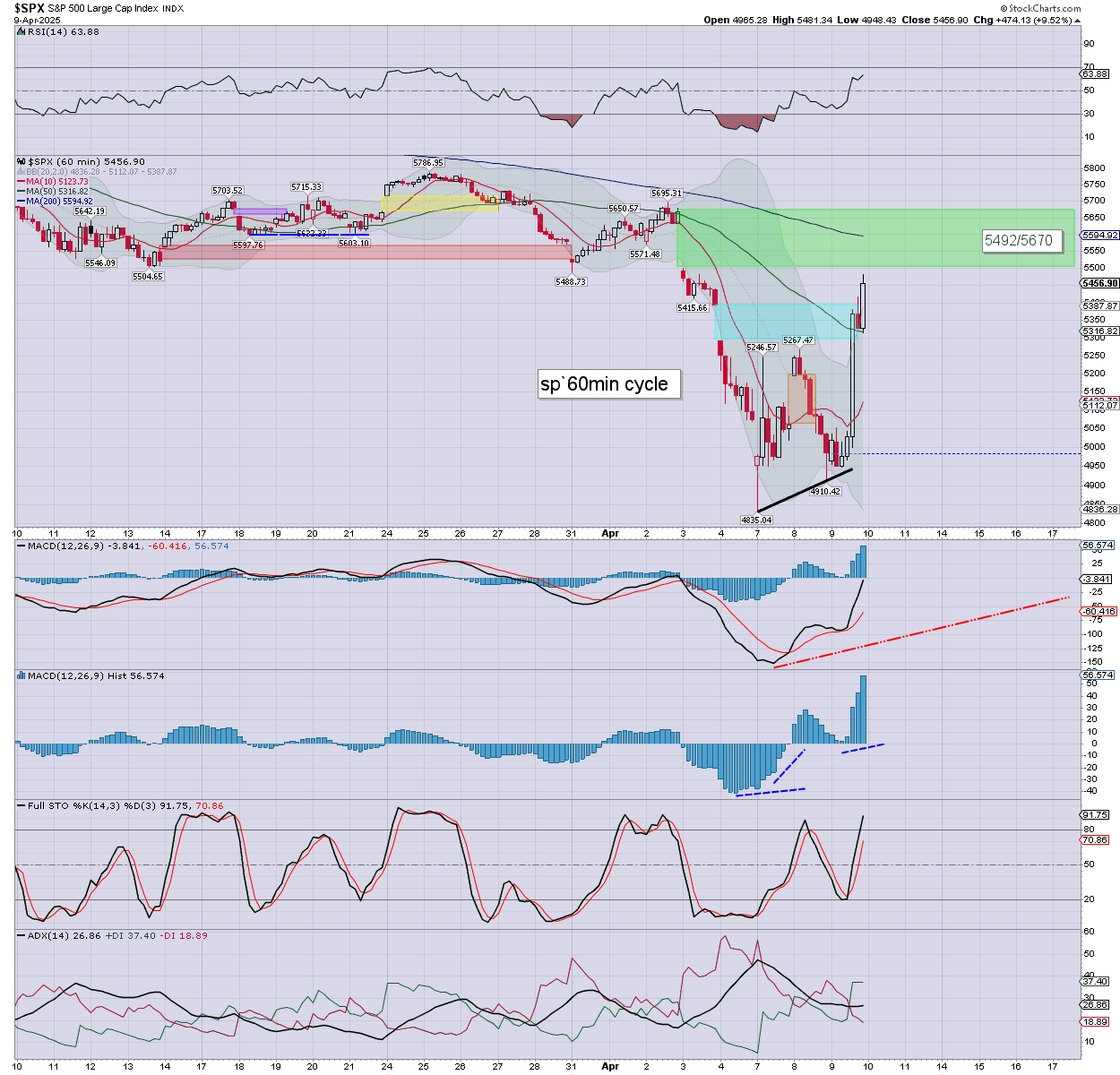

sp’60min

Summary

After yesterday’s monstrous ramp… even if we swing around 100/200pts today, it’ll be a relatively subdued day!

As things are… we’re set to open -100pts or so. Bulls can argue its just a retrace.

The CPI data is due 8.30am, and will be one excuse to recover before the open. Consensus…

Headline y/y: 2.6% vs 2.8% prior

Core y/y: 3.0% vs 3.1% prior

Considering Monday’s low of 4835, the bulls should be content with any net weekly gain (>5074), as seems probable.

—

Early movers

AAL -3%

AAPL -3%

ALB -3%

AMD -3%

AMZN -2%

–

BABA +1.3%

BAC -1.5%

CLF -3%

–

COIN -2.5%

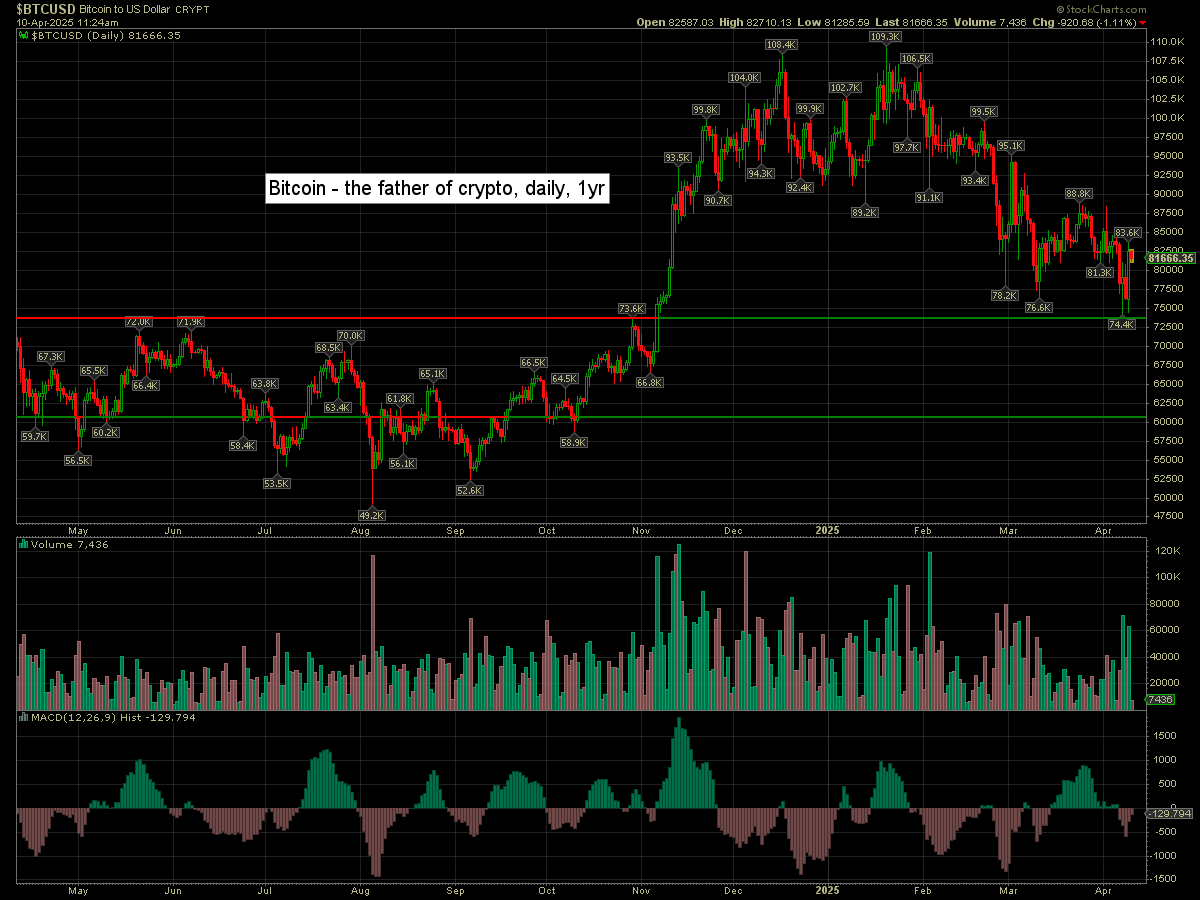

Bitcoin is -1.1% at $81666

–

DIS -2%

DJT +3%

–

F -3.5%

FCX -2%, with copper +15cents to $4.34

GOLD +0.3%

INTC -4%

JPM -1.5%, earnings due early Friday

–

KMX -6.3%, EPS 58cents vs 68est. Rev’ y/y +6.7% to $6.00bn vs 5.96est.

–

MRNA -2%

MSTR -4%

MU -3%

NMAX -2%

NVDA -3%

OXY -3%

–

RCAT -6%, $30M direct stock offering

RIG -4%

SMCI -4%

SMR -3%

SONY +3%

–

STLA -8%

TSLA -4%

UAL -2%

–

VIX +10.6% at 37.20

–

X -10%… as Trump argues US Steel should remain American owned

–

XOM -1%

XPEV +4%

—

Overnight markets

Asian and European markets generally following the USA upward…

Japan: +9.1% to 34609

China: +1.2% to 3223

Germany: currently +5.8% at 20805

UK: currently +4.7% at 8039

—

Have a good Thursday