Good morning. US equity futures are broadly higher, SPX +35pts, we’re set to open at 5193. USD is +0.2% at DXY 98.21. The precious metals are mixed, Gold +0.9% (printing new hist’ high of $3499), with Silver -0.2%. WTIC is +0.8% in the low $63s.

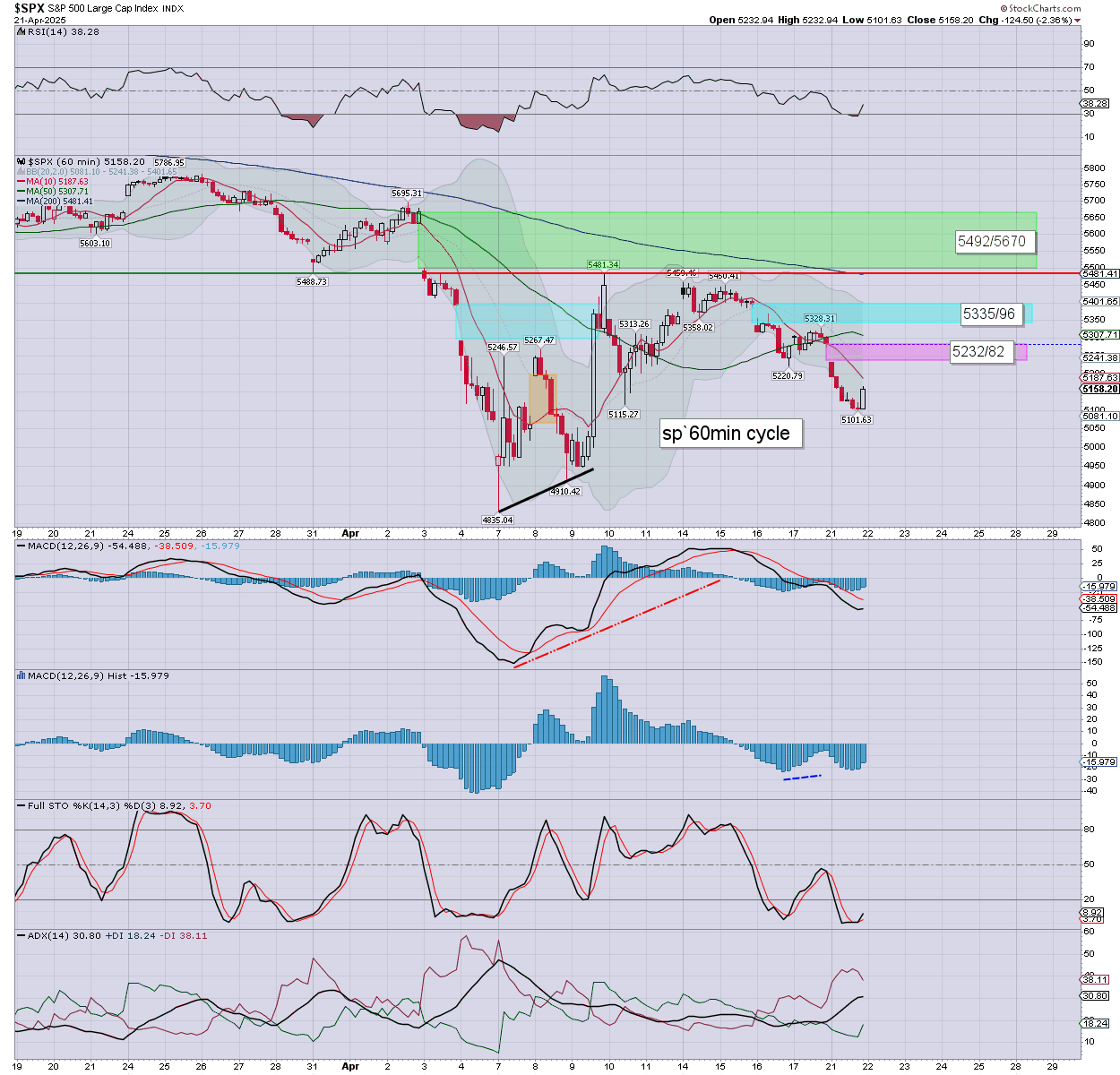

sp’60min

Summary

Yesterday opened sig’ lower, with the market sliding into the mid afternoon, if seeing a late day sig’ bounce. S/t momentum settled on the moderately low side.

Overnight futures have been broadly positive, we’re set to open +35pts or so to the 5190s. The s/t cyclical setup favours the bulls.

—

Early movers

AAPL +0.9%

AMZN +1.0%, BofA, buy, $225

BABA +3.7%

–

BHC +15.5% Icahn and affiliates have ‘cash-settled equity swaps worth around $90M of common stock’.

–

CLF +0.9%

–

COIN +0.6%

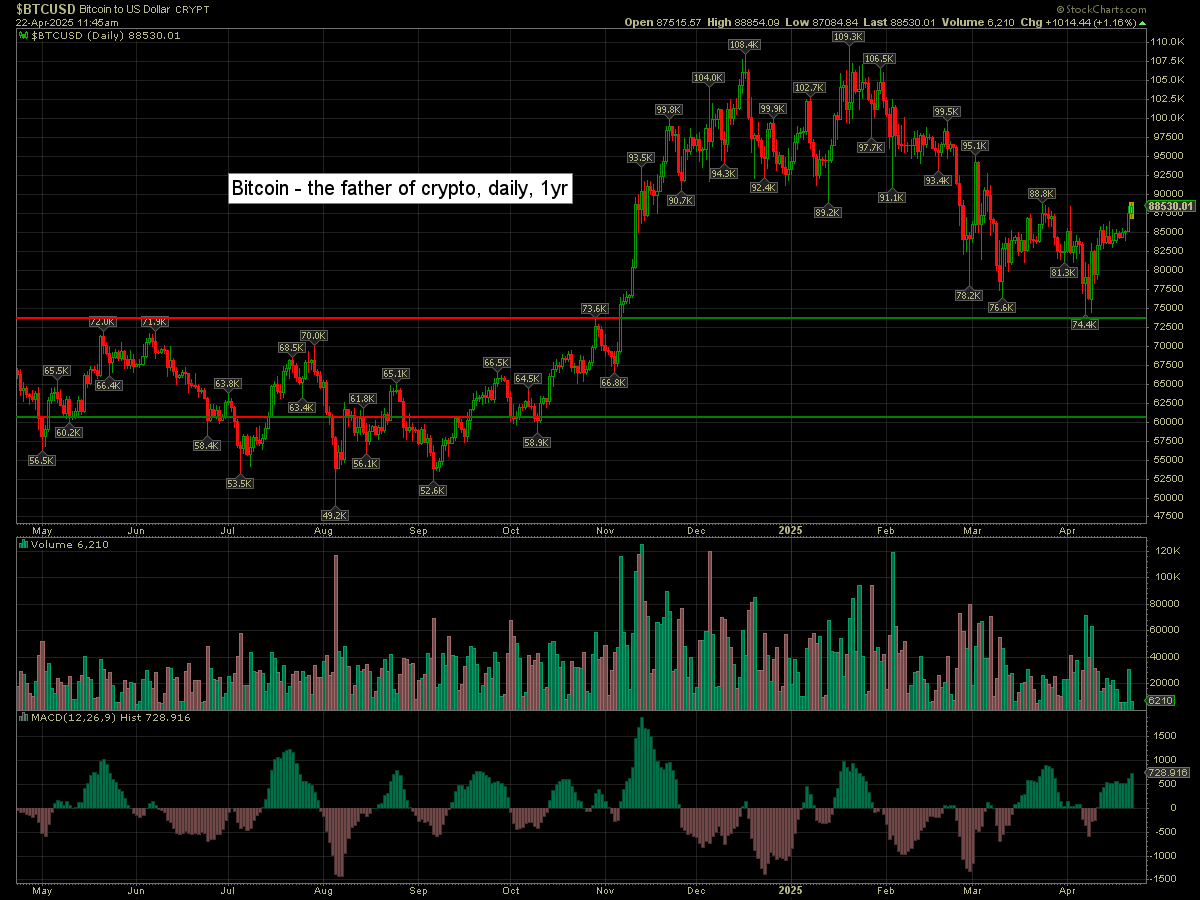

Bitcoin is +1.1% at $88530

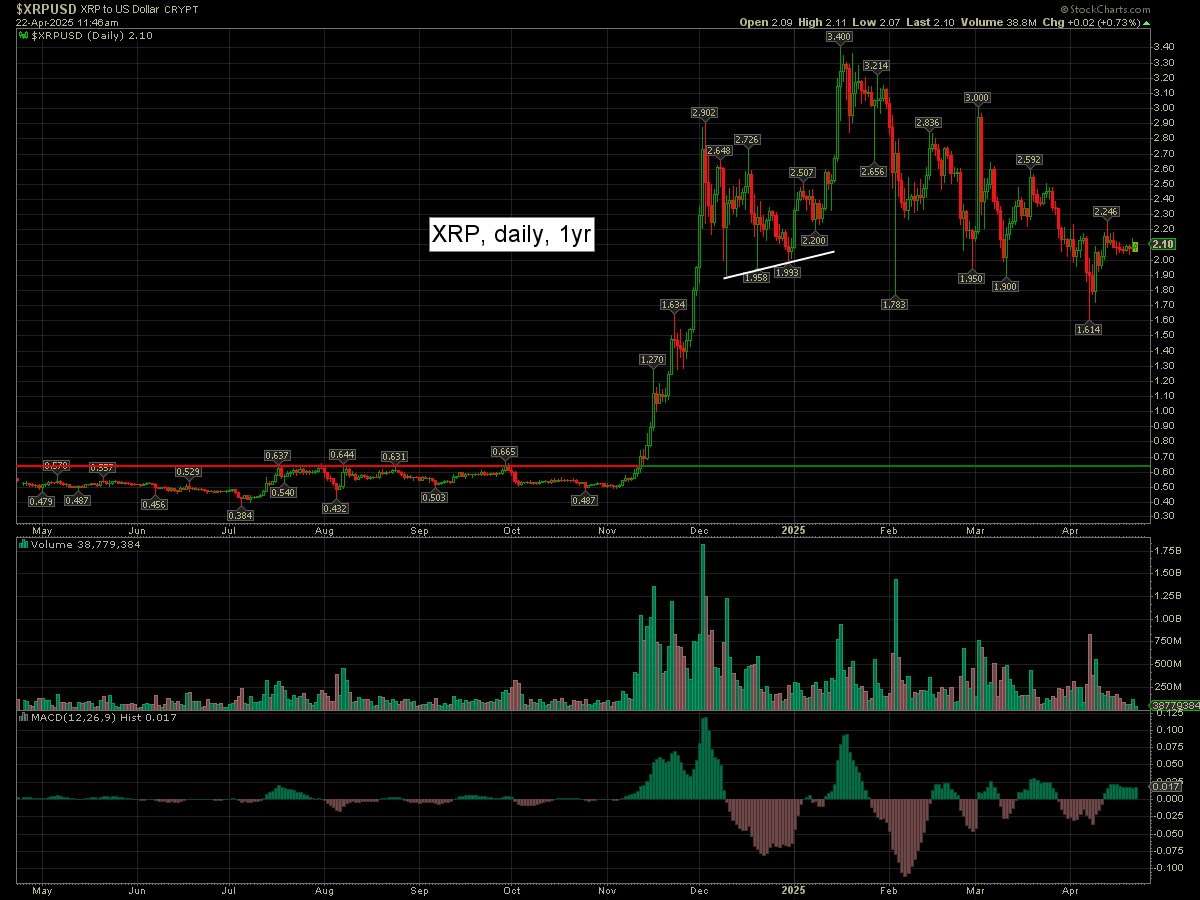

XRP is +2cents to $2.10. I HOLD, looking for a break >2.24

–

DHR +3.0%, EPS $1.88 vs 1.64est. Rev’ y/y -0.9% to $5.7bn vs 5.6est.

–

DVN +3.5%

–

ELV -1.6%, EPS $11.97 vs 11.38est. Rev’ y/y +15.0% to $48.8bn vs 46.3est.

–

FCX +1.1%, with copper +3cents to $4.76

FSLR +6.0%, tariffs on solar cells from Asia

–

GE +2.9%, EPS $1.49 vs 1.26est. Rev’ y/y -43.9% to $9.00bn inline. Backlog $170bn

–

GOOGL +0.7%, earnings Thurs’ AH

–

GOLD +2.0%, selling it’s ‘Alaska gold project’ for up to $1.1bn to John Paulson’s ‘Paulson Advisers and Novagold Resources’ (NG)

–

HAL -1.7%, EPS 60cents inline. Rev’ y/y -6.7% to $5.4bn vs 5.3est.

–

INTC +0.7%, earnings Thurs’ AH

–

KMB -3.6%, EPS $1.93 vs 1.89est. Rev’ y/y -6.0% to $4.84bn vs 4.89est

–

LMT +2.5%, EPS $7.28 vs 6.32est. Rev’ y/y +4.5% to $17.96bn vs 17.79est. Backlog $173bn

–

MMM +3.1%, EPS $1.88 vs 1.77est. Rev’ y/y -22.9% to $5.95bn vs 5.76est. Guidance assumes ’20c-40c tariff sensitivity’.

–

NEM +0.9%

NFLX +0.7%

NG +3.9%, buying Alaska prospects from Barrick Gold

–

NOC -9.6%, EPS $6.06 vs 6.26est. Rev’ y/y -6.6% to $9.46bn vs 9.93est. Backlog $93bn

–

NVDA +0.9%

NVO +1.8%

OXY +1.3%

–

RTX -3.1%, EPS $1.47 vs 1.35est. Rev’ y/y +5.2% to $20.3bn vs 19.8est. Backlog $125bn

–

SMR +1.4%

–

SYF -1.0%, EPS $1.89 vs 1.64est. Rev’ y/y +1.3% to $4.46bn vs 4.56est. $2.5bn buyback and divi +25%, 25>30cents.

–

T -2.8%, in sympathy with VZ

–

TSLA +0.7%, earnings due in AH

TXN -1.3%, Barclays, equal-weight>underweight, 180>125

UAL +0.8%

–

VIX -4.4% at 32.33

–

VZ -4.0%, EPS $1.19 vs 1.15est. Rev’ y/y +1.5% to $33.5bn vs 33.3est.

–

X +0.9%

XPEV +3.3%

—

Overnight markets

Asian markets were a little mixed, whilst European markets are leaning on the weaker side…

Japan: -0.2% to 34220

China: +0.25% to 3299

Germany: currently -0.7% at 21053

UK: currently -0.02% at 8274

—

Have a good Tuesday