Good morning. US equity futures are broadly higher, SPX +45pts, we’re set to open at 5617. USD is +0.25% at DXY 103.19. The precious metals are a little mixed, Gold -0.1%, with Silver +0.4%. WTIC is +0.6% in the upper $66s.

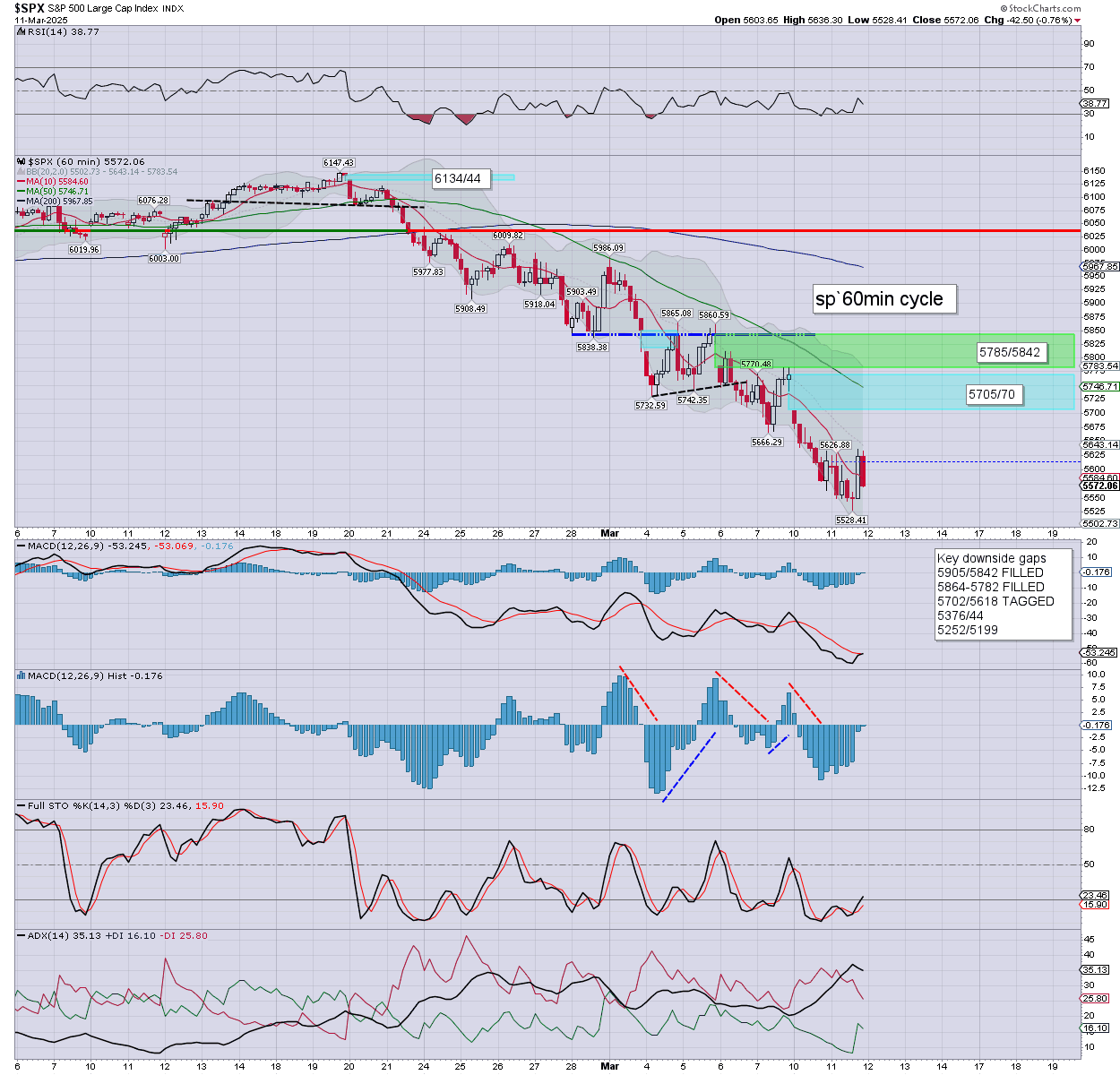

sp’60min

Summary

Yesterday saw the SPX print yet another lower high and lower low. The closing hour was itself typical of underlying weakness. S/t momentum settled fractionally negative.

Overnight futures have been leaning positive. We’re set open +40pts or so into the low 5600s. However.. the CPI data is due 8.30am, and could flip the market back lower.

A more natural floor would be from around 5400. Certainly, the bears are running out of time… ahead of next week’s FOMC.

—

Early movers

AAL +1.3%

AMD +1.7%

AMZN +0.9%

AVGO +1.8%

–

BIDU -1.3%

CCJ +1.9%, Stifel, buy, C$90

CLF +1.0%

–

COIN +0.8%

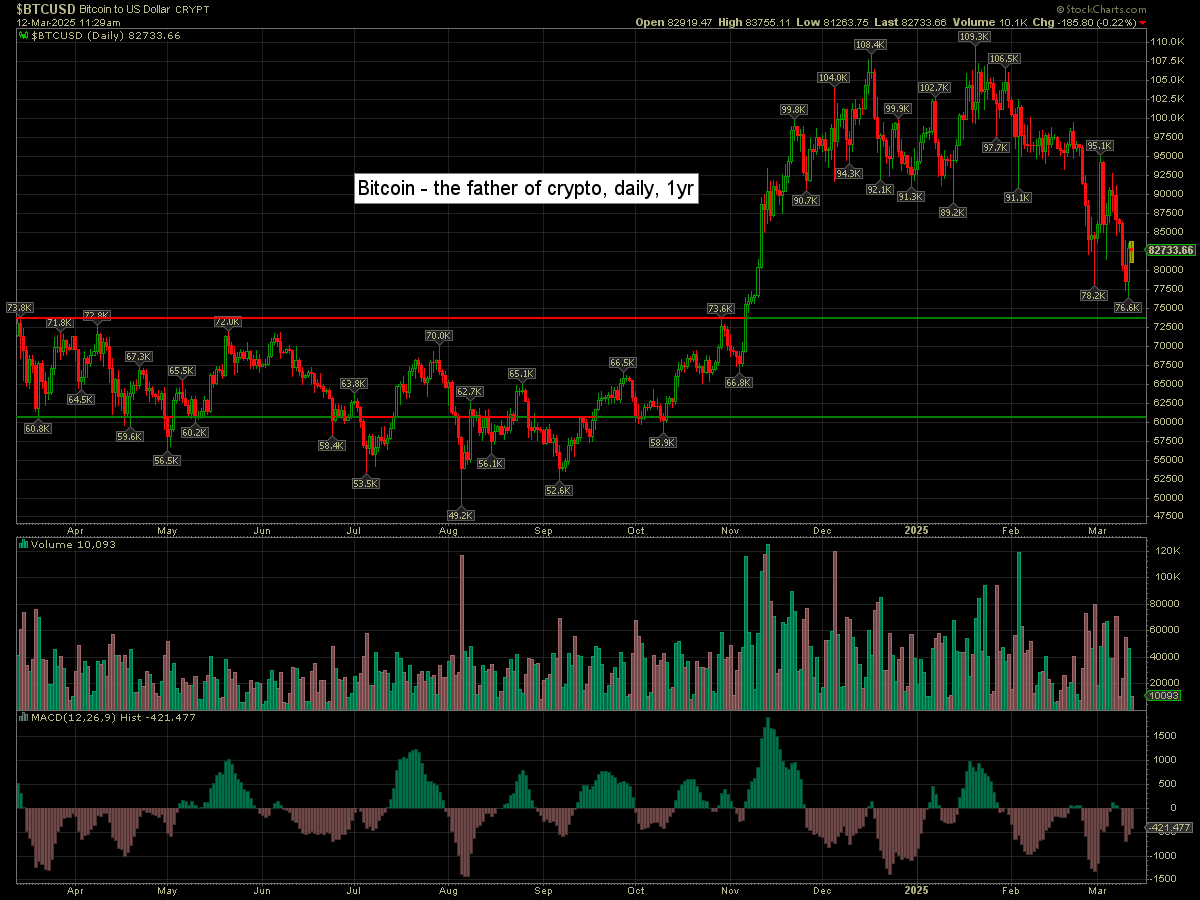

Bitcoin is currently -0.2% at $82733

–

DIS +0.9%

FCX +1.3%, with copper +9cents to $4.86 !

–

FOA -16.5%, post earnings upset

–

GRPN +19.0%, earnings: EPS -$1.20 vs -0.04est. Rev’ $130.4M vs 127.7est. Over-hyped since day one, still not profitable.

–

HOOD +3.2%, Deutsche Bank, buy, 75>61

–

INTC +7.9%, Taiwan Semicon’ proposing a joint venture with Nvidia, AMD, and Broadcom to operate Intel factories.

–

KRE +0.6%

MOMO -11.5%, post earnings upset

MLYS -6.4%, $175M secondary offering

–

MT -3.6%, suing the Indian regime over import restrictions.

NVDA +2.4%

–

NVO -4.8%

OKLO +3.4%

OXY +0.7%

PLTR +4.3%

–

SMCI +3.4%

TSM +1.0%

TSLA +3.7%, with Elon touting he’ll double (US based) production within two years.

–

UAL +0.6%

UEC +1.2%, Stifel, buy, $10.50

UNG -1.3%, with Natgas $4.30

–

VIX -4.0% at 25.83

–

XOM +1.0%

ZIM +4.1%, post earnings gains

ZYXI -34.4%, issues with Tricare suspending payments.

—

Overnight markets

Asian markets were a little mixed, whilst European markets are broadly higher…

Japan: +0.1% to 36819

China: -0.2% to 3371

Germany: currently +1.7% at 22713

UK: currently +0.6% at 8548

—

Have a good Wednesday