Good morning. US equity futures are leaning weak, SPX -15pts, we’re set to open at 6129. USD is -0.2% at DXY 106.83. The precious metals are leaning upward, Gold +0.3% (printing a new hist’ high of $2973), with Silver +1.0% at $33.65. WTIC is +0.5% in the mid $72s.

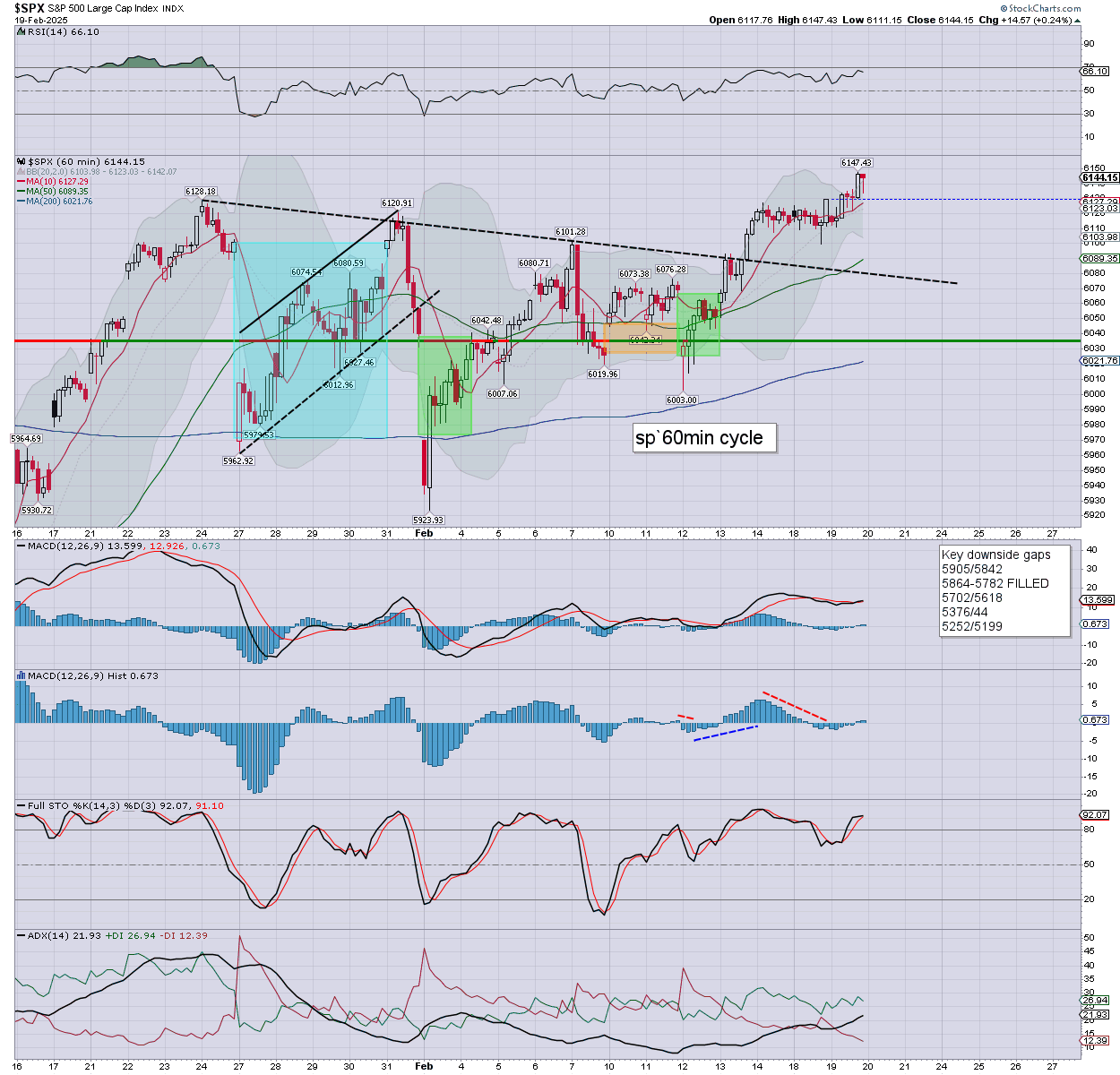

sp’60min

Summary

Yesterday opened a little weak, but the market leaned back upward, the SPX printing a new hist’ high of 6147. S/t momentum settled fractionally positive.

Overnight futures have been leaning a little weak, we’re set to open -15pts or so. The s/t cyclical setup favours the bears. Right now, an OPEX pin around 6100 looks most likely.

Yours truly remains interested in picking back up SMR from 20/19s.

—

Early movers

AG +2.8%, EPS 3cents vs 4est. Rev’ y/y +25.9% to $172.3M vs 159.0est.

–

BABA +10.6%, EPS $2.93 vs 2.66est. Rev’ y/y +4.7% to $38.4bn vs 38.2est.

–

BAX +7.6%, EPS 58cents vs 52est. Rev’ y/y +0.9% to $2.75bn vs 2.67est.

–

BILI +13.0%, EPS 15cents vs 14est. Rev’ y/y +21.7% to $1.06bn vs 1.07est

–

CCJ +2.3%, 36cents vs 32est. Rev ‘y/y +90.8% to $1.18bn vs 1.08est.

–

CLF +0.5%

–

COIN +0.5%

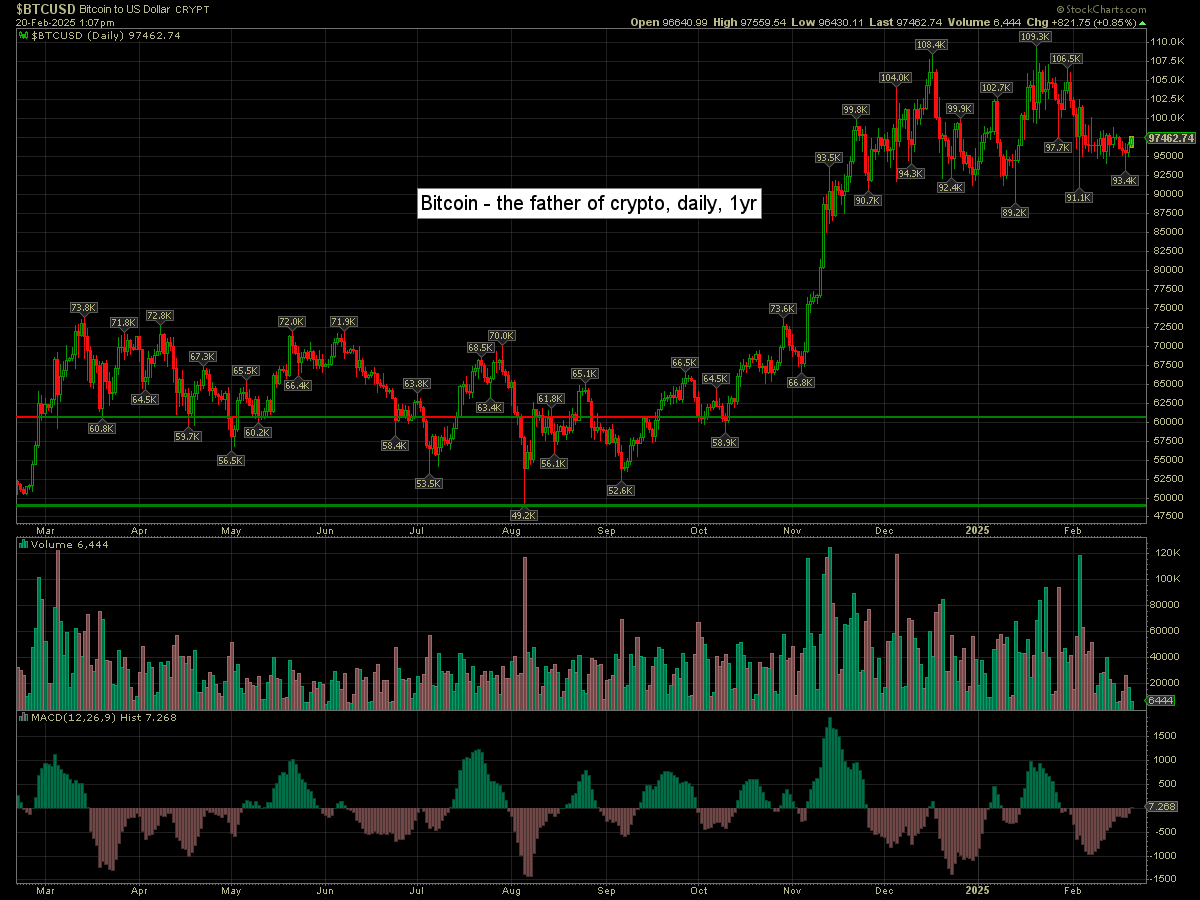

Bitcoin is +0.8% at $97462

–

CVNA -8.4%, post earnings upset

–

CWAN +17.8%, EPS 13cents vs 11est. Rev’ y/y +27.7% to $126.4M vs 120.3est.

–

ENVX -5.9%, post earnings depression

EXAS -2.9%, post earnings depression

–

FCX +1.0%, with copper +5cents to $4.60

GOLD +1.1%

INTC -1.3%

IQ -8.3%, $300M convert’ corp’ debt offering

NBIS -5.0%

–

NEM +0.9%

NXPI +3.6%, Citi, neutral>buy, 210>290, Mizuho, outperform, 240>255

–

OXY +0.4%

PLTR -4.0%, s/t bubble burst, with the CEO looking to sell $1.2bn of stock

–

SHAK +8.8%, EPS 26cents vs 24est. Rev’ y/y +14.8% to $328.7M vs 327.9est.

–

SMCI -1.7%

SMR +1.5%

TECK +1.8%

TGT -2.4%, in sympathy with Walmart

TSLA +0.3%

–

U -8.7%, EPS -30cents vs -37est. Rev’ y/y -25.0% to $457M vs 433est. Soft guidance

–

UNG -3.4%, with Natgas $4.14

VALE +2.4%, post earnings gains

–

VIX +2.2% at 15.60

–

WMT -8.3%, EPS 66cents vs 64est. Rev’ y/y +4.2% to $180.6bn vs 180.0est. Soft guidance

–

WRD -4.7%

—

Overnight markets

Asian markets were weak, whilst European markets are moderately mixed…

Japan: -1.2% to 32678

China: -0.02% to 3350

Germany: currently +0.4% at 22520

UK: currently -0.4% at 8674

—

Have a good Thursday