Good morning. US equity futures are leaning weak, SPX -20pts, we’re set to open at 6046. USD is -0.04% at DXY 108.15. The precious metals are weak, Gold -0.3% (if printing a new hist’ high of $2968), with Silver -1.2% at $32.14. WTIC is +1.2% in the mid $73s.

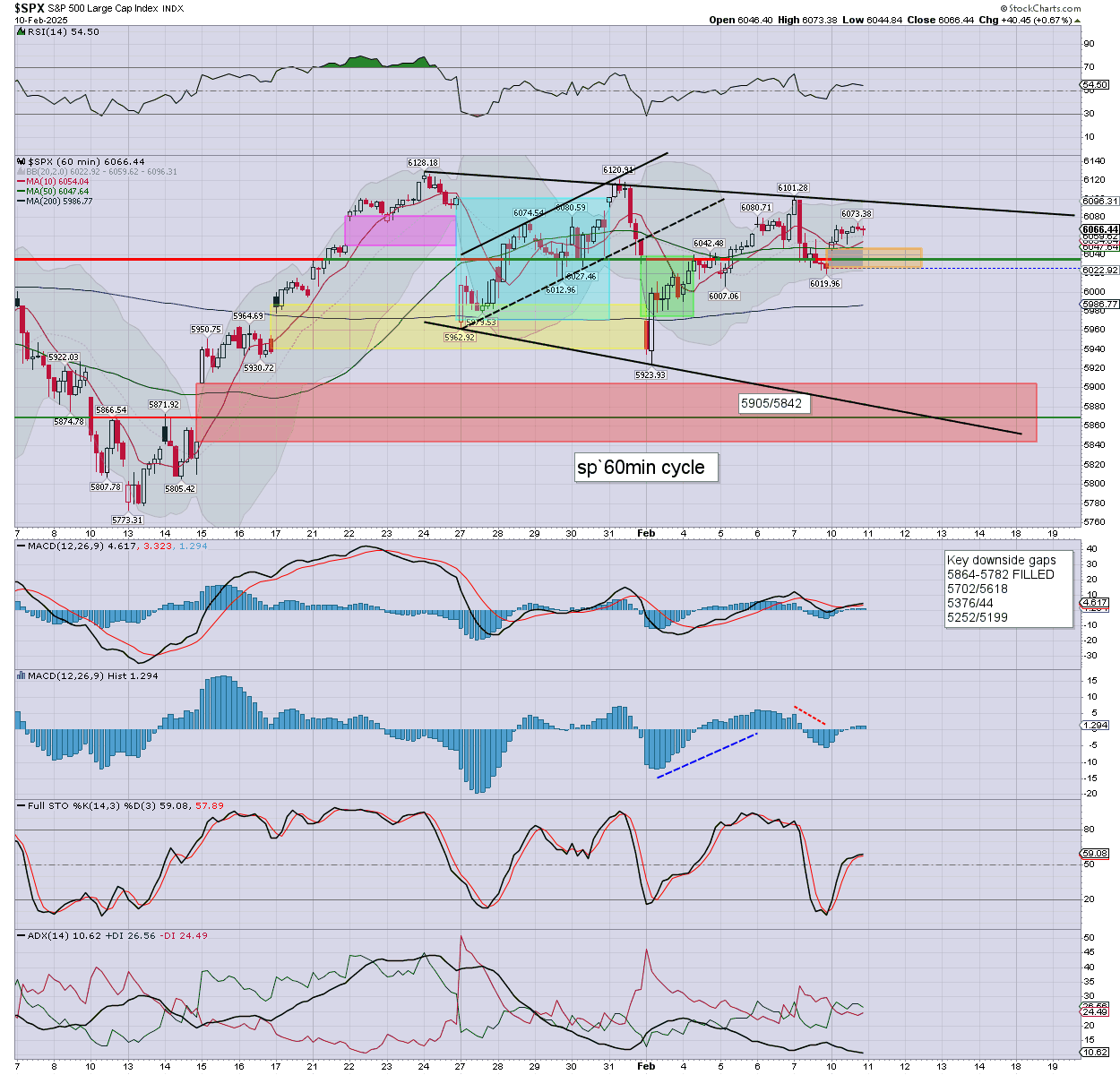

sp’60min

Summary

Yesterday saw early upside, but then flat lining across the day. S/t momentum settled fractionally positive.

Overnight futures have been leaning on the weaker side, we’re set to open -15/20pts. Things turn interesting under last Friday’s low of 6019. Support psy’ 6K. Big target remains a tag, or full fill of red gap… starting at 5905. Considering the Powell, CPI, and PPI, that really isn’t bold.

Today’s big event will be the Powell, who will be speaking to the political hacks 10am>1pm. Mr Market will certainly be listening! I’ll highlight a live feed (via CNBC, youtube) nearer the time.

—

Early movers

AA +1.2%

AAPL -0.4%

AG -1.0%

AMKR -9.2%, post earnings upset

BABA -2.3%

–

CENX +1.5%

CLF +3.2%

CMCO -5.6%, post earnings depression

–

COIN +0.1%

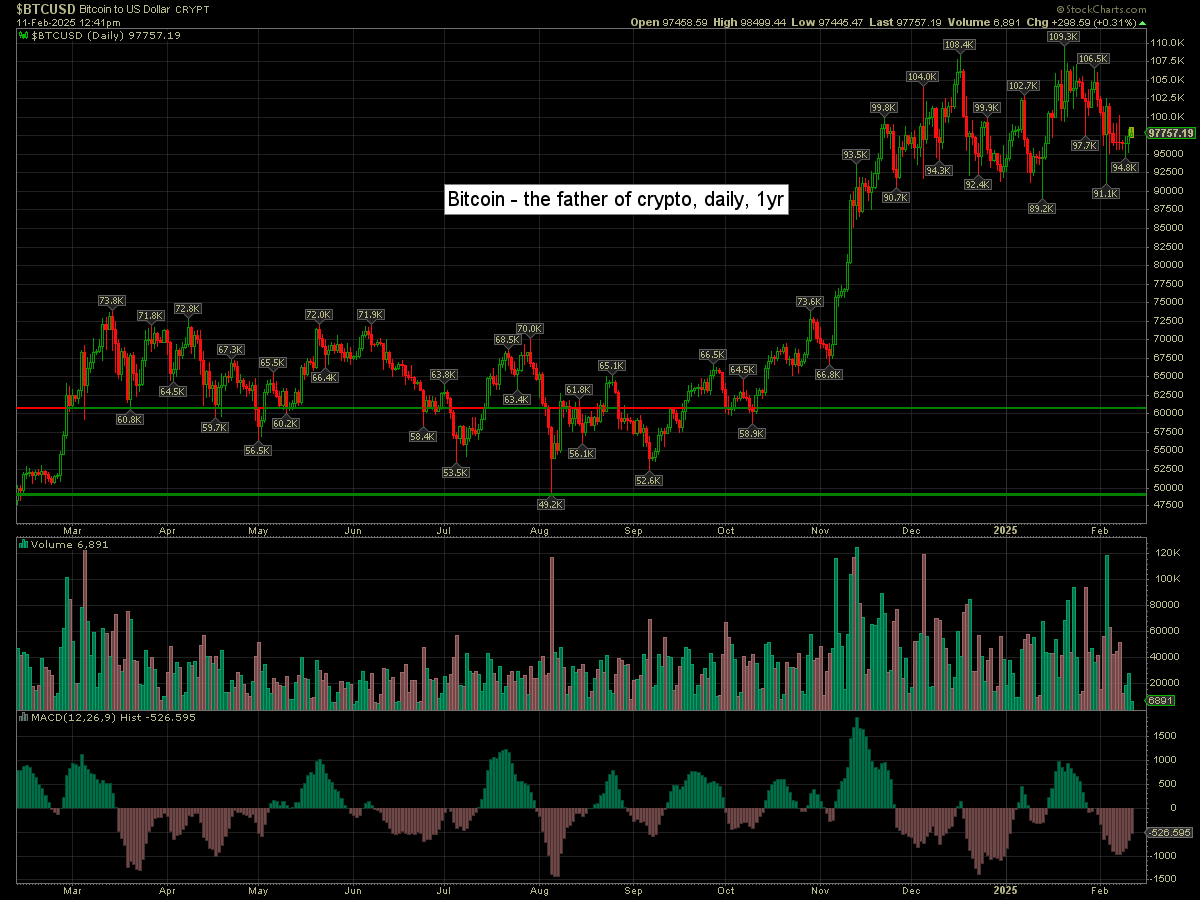

Bitcoin is +0.3% at $97757

–

DD +5.5%, EPS $1.13 vs 0.98est. Rev’ y/y +6.7% to $3.09bn vs 3.06est. DuPont touting a semicon recovery and AI

–

FCX -0.8%, with copper -12cents at $4.57

–

FIS -7.4%, EPS $1.40 vs 1.36est. Rev’ y/y +3.5% to $2.60bn vs 2.63est. Weak guidance. Partnering with Affirm for ‘pay over time’ services.

–

FSLR +1.8%, Mizuho, neutral>outperform, 218>259

FLNC -38.9%, post earnings horror

–

GFS -4.3%, EPS 46cents vs 44est. Rev’ $1.830bn vs 1.829est.

–

GOLF +8.8%, joining the SPX 600 on Thurs’, replacing ‘Retail Opportunity Investments’ (ROIC)

–

GOLD -0.4%

GOOGL -0.4%

HLIT -29.3%, post earnings horror

–

HUM +1.5%, EPS -$2.16 inline. Rev’ y/y +13.5% to $29.19bn vs 28.83est. Medicare Advantage Annual membership y/y -10.0% (550,000).

–

KO +3.3%, EPS 55cents vs 52est. Rev’ y/y +6.0% to $11.50bn vs 1.068est.

–

LSCC +12.5%, post earnings jump

–

MAR -2.1%, EPS $2.45 vs 2.38est. Rev’ y/y +5.5% to $6.42bn vs 6.37est.

–

MU -1.0%

NUE +1.8%

NVDA -0.5%

OXY +0.4%

PSX +5.2%, activist investor Elliott Mgmt’ pushing for ‘more’

–

SHOP -3.5%, EPS 44cents vs 43est, and vs 34 prior yr. Rev’ y/y +31.2% to $2.81bn vs 2.73est.

–

SLB +0.5%

SMCI -2.5%, earnings due in AH

SMR -0.3%

STLD +1.6%

–

TSLA -0.4%

UAL -0.3%

UNG +1.8%, with Natgas $3.50

–

VIX +1.5% at 16.05

–

VSAT -18.5%, news? *I see earnings were last Thurs’

–

XOM +0.4%

WBA -2.2%

WMT +0.3%, Citi, buy, 98>120

—

Overnight markets

Asian markets were moderately mixed, whilst European markets are fractionally mixed…

Japan: CLOSED

China: -0.1% to 3318

South Korea: +0.7% to 2539

–

Germany: currently +0.1% at 21934

France: currently -0.04% at 8003

UK: currently +0.04% at 8771

—

Have a good Tuesday