Good morning. US equity futures are broadly flat (ahead of CPI), SPX -1pt, we’re set to open at 6067. USD is -0.01% at DXY 107.82. The precious metals are leaning weak, Gold -0.4%, with Silver -0.2%. WTIC is -0.8% in the mid $72s.

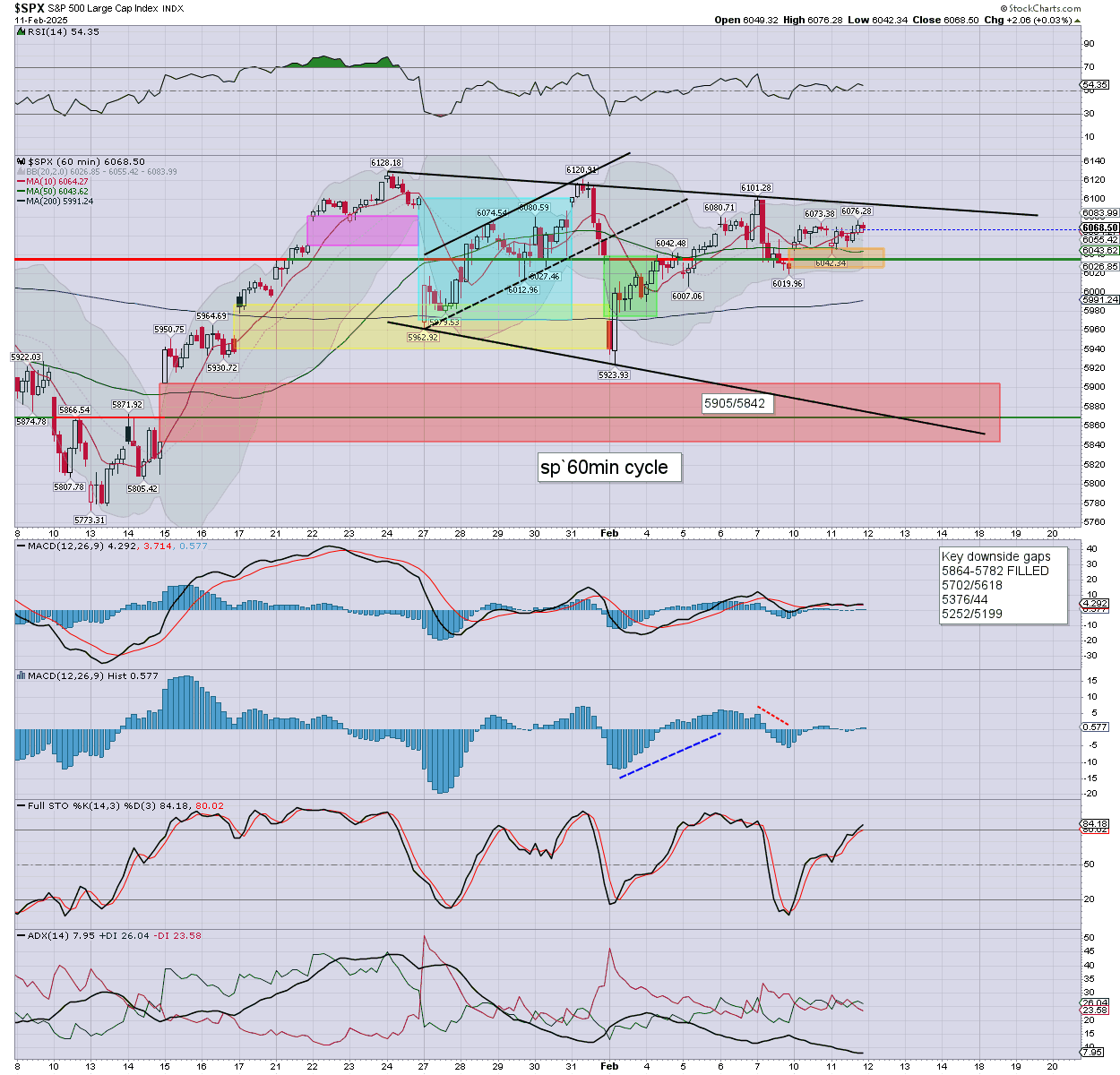

sp’60min

Summary

Yesterday saw considerable chop, with the SPX settling effectively flat. S/t momentum settled fractionally positive.

Overnight futures have been very subdued, we’re set to open broadly flat. However, the CPI data is due 8.30am EST, and will likely be market moving.

Consensus:

Headline y/y: 2.9% vs 2.9% prior

Core y/y: 3.2% vs 3.2% prior

In theory, we should lean weak, and washout to around 5900. That target will be dropped if a break AND hold >6100.

Yours truly holds INTC and OXY, with a shopping cart to buy back SMR, CLF, or maybe something else. I resolutely wait for 5900.

—

Early movers

AG -0.5%

AUR +2.0%, earnings due in AH

BABA +3.5%

CLF +0.5%

CFLT +13.9%, post earnings leap

–

COIN +1.5%, earnings due Thurs’ AH

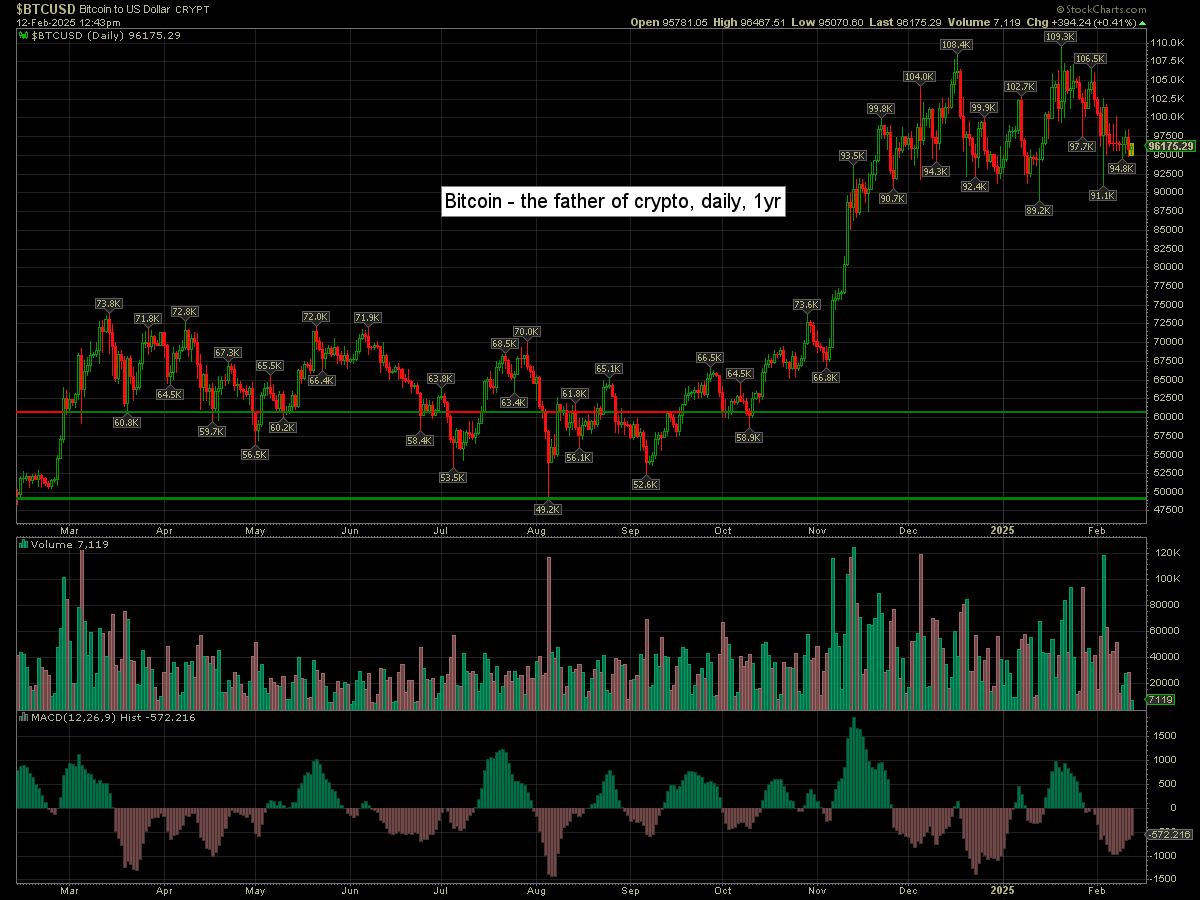

Bitcoin is +0.4% at $96175

–

CVS +11.3%, EPS $1.19 vs 0.93est. Rev’ y/y +4.1% to $97.71bn vs 97.19est.

–

DASH +5.9%, post earnings gains

FCX +0.1%, with copper +1cent to $4.61

GILD +4.4%, post earnings gains

–

GOLD +1.3%, EPS 46cents vs 41est. Rev’ y/y +19.2% to $3.64bm vs 3.98est. $1bn buyback. Divi’ 10cents

–

GNRC +3.0%, EPS $2.80 vs 2.50est. Rev’ y/y +16.1% to $1.235bn vs 1.241est.

–

INTC +5.5%, 🙂

–

KHC -4.7%, EPS 84cents vs 78est. Rev’ y/y -4.1% to $6.58bn vs 6.66est. Kraft Heinz touts a ‘challenging year’, with weak guidance. No soup for YOU !

–

LYFT -13.8%, post earnings horror

–

MCY +21.9%, EPS $1.82 vs 0.64est, and vs 3.46 prior yr. Rev’ y/y -0.1% to $1.366bn

–

NVDA +0.4%

NXPI +3.1%, Morgan Stanley, equal-weight>overweight, 231>257

NVO -2.3%

–

OXY +0.7%

SMCI +9.7%, post earnings jump

SMR +0.8%

–

STAA -34.7%, EPS -69cents vs -16est. Rev’ y/y -35.8% to $48.9M vs 77.2est, and vs 76.2 prior yr. Staar cites weak China demand

–

TDC -13.9%, EPS 53cents vs 43est. Rev’ y/y -10.5% to $409M vs 414est.

–

TSLA +1.7%

UBER -1.5%, in sympathy with LYFT

–

UPST +26.5%, post earnings leap

VSAT +1.9%, dead cat bouncing

–

VIX -0.4% at 15.96

–

VRT -9.1%, EPS 99cents vs 82est. Rev’ y/y +25.8% to $2.34bn vs 2.15est.

–

WAB -5.3%, EPS $1.68 vs 1.72est. Rev’ y/y +2.3% to $2.583bn vs 2.618est. Weak guidance

–

WAT -8.7%, EPS $4.10 vs 4.03est. Rev’ y/y +6.5% to $872M vs 857est.

–

XOM -0.9%

Z -5.6%, post earnings depression

—

Overnight markets

Asian markets were moderately higher, whilst European markets are a little higher…

Japan: +0.4% to 38963

China: +0.8% to 3346

Germany: currently +0.3% at 22109

UK: currently +0.03% at 8779

—

Have a good Wednesday