Good morning. US equity futures are fractionally lower, SPX -6pts, we’re set to open at 6080. USD is +0.2% at DXY 108.20. The precious metals are broadly lower, Gold -0.4% (printing $2750), with Silver -1.5% (printing $30.72). WTIC is +0.3% in the mid $75s.

sp’60min

Summary

Yesterday saw the SPX break a new historic high… if cooling a little into the close. S/t momentum settled fractionally positive.

Overnight futures have been leaning on the weaker side, we’re set to open fractionally lower by -5/10pts. The s/t cyclical setup favours the bears, with three downside gaps.

Yours truly is trying to be patient for Intel earnings… Jan’30th AH. I would like to pick back up SMR from the 22/21s.

—

Early movers

AAL -8.4%, EPS 86cents vs 64est. Rev’ $13.7bn vs 13.39est. Weak guidance. CAPEX limited due to Boeing delivery delays.

–

AAPL +0.2%, Goldman, buy, 286>280

AG -2.0%

AMAT -2.2%

ARM -4.4%

ASTS -15.6%, $400M convert’ corp’ bonds offer.

–

AXP +0.8%, earnings due early Friday

CLF u/c

–

COIN -2.7%

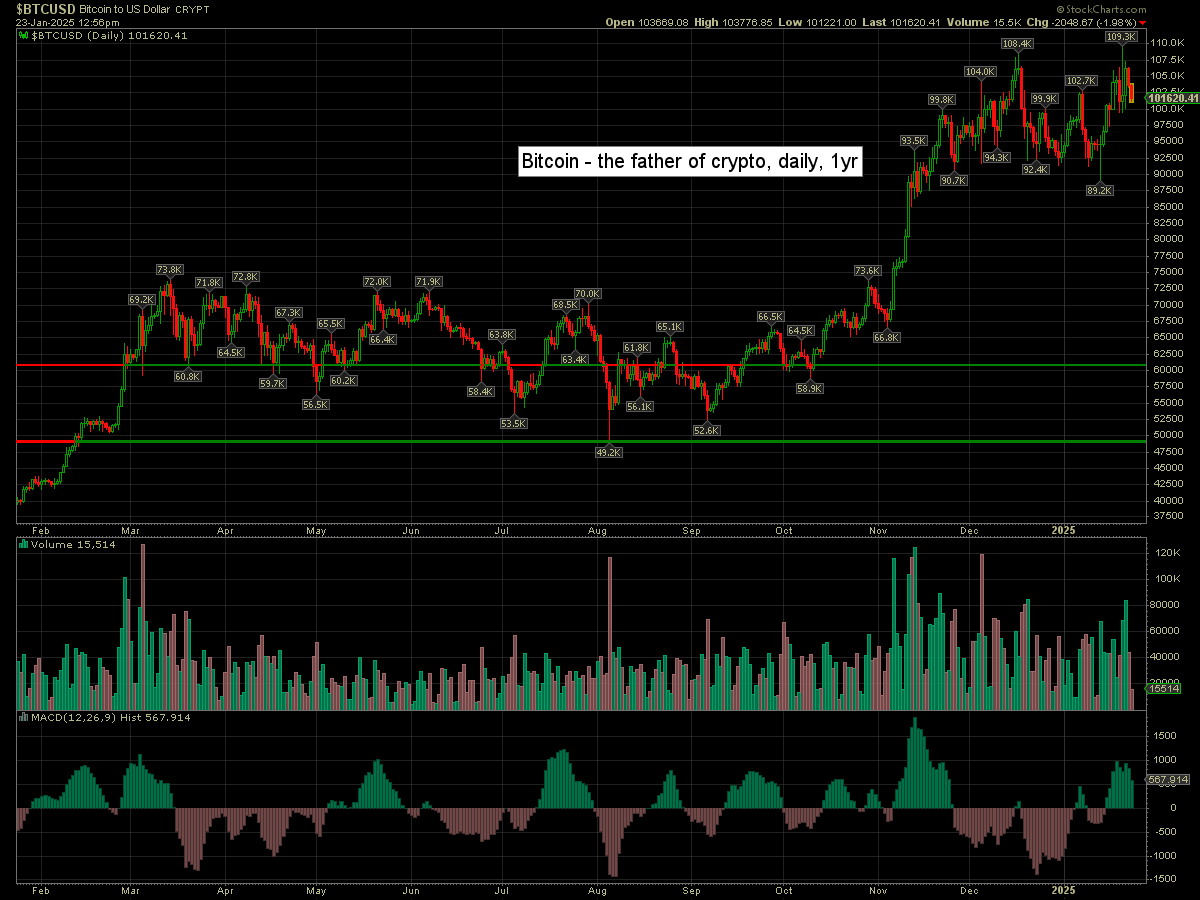

Bitcoin is -2.0% at $101620

–

CVS +1.3%, helped by ELV

DJT -2.4%

EA -17.1%, pre-earnings, cuts guidance

–

ELV +5.2%, EPS $3.84 vs 3.81est. Rev’ y/y +6.0% to $44.99bn vs 44.86est.

–

FCX +0.5%, with copper -3cents to $4.27

–

GE +7.9%, EPS $1.32 vs 1.04est. Rev’ y/y +15.6% to $9.87bn vs 9.60est. $7bn buyback. Divi >30% in 2025

–

GME +1.4%

GOLD -0.5%

INTC -0.7%

KNX +3.6%, post earnings gains

LOGI +2.3%

–

MARA -2.7%

META +0.5%, BofA, buy, 660>710

MU -3.0%

–

NNE -2.6%, cooling nuclear stocks

NVDA -1.7%

OKLO -5.5%

OXY +0.3%

–

PLTR -1.5%

RKLB -2.8%

SMCI -2.1%

SMR -3.7% in the mid $24s

–

TSLA -0.4%

UAL -1.8%

UNH +1.5%, helped by Elevance Health

–

UNP +3.9%, $2.91 vs 2.78est. Rev’ y/y -0.6% to $6.12bn vs 6.14est. Buyback $4.0-4.5bn

–

VIX +1.0% at 15.21

–

XOM +0.4%

—

Overnight markets

Asian and European markets all leaning upward…

Japan: +0.8% to 39958

China: +0.5% to 3230

Germany: currently +0.3% at 21316

UK: currently +0.03% at 8547

—

Have a good Thursday