Good morning. US equity futures are leaning weak, SPX -15pts, we’re set to open at 5836. USD is +0.4% at DXY 104.37. The precious metals are mixed, Gold u/c (if printing a new hist’ high of $2772), with Silver -1.0% (cooling to $34.63). WTIC is -1.3% in the mid $70s.

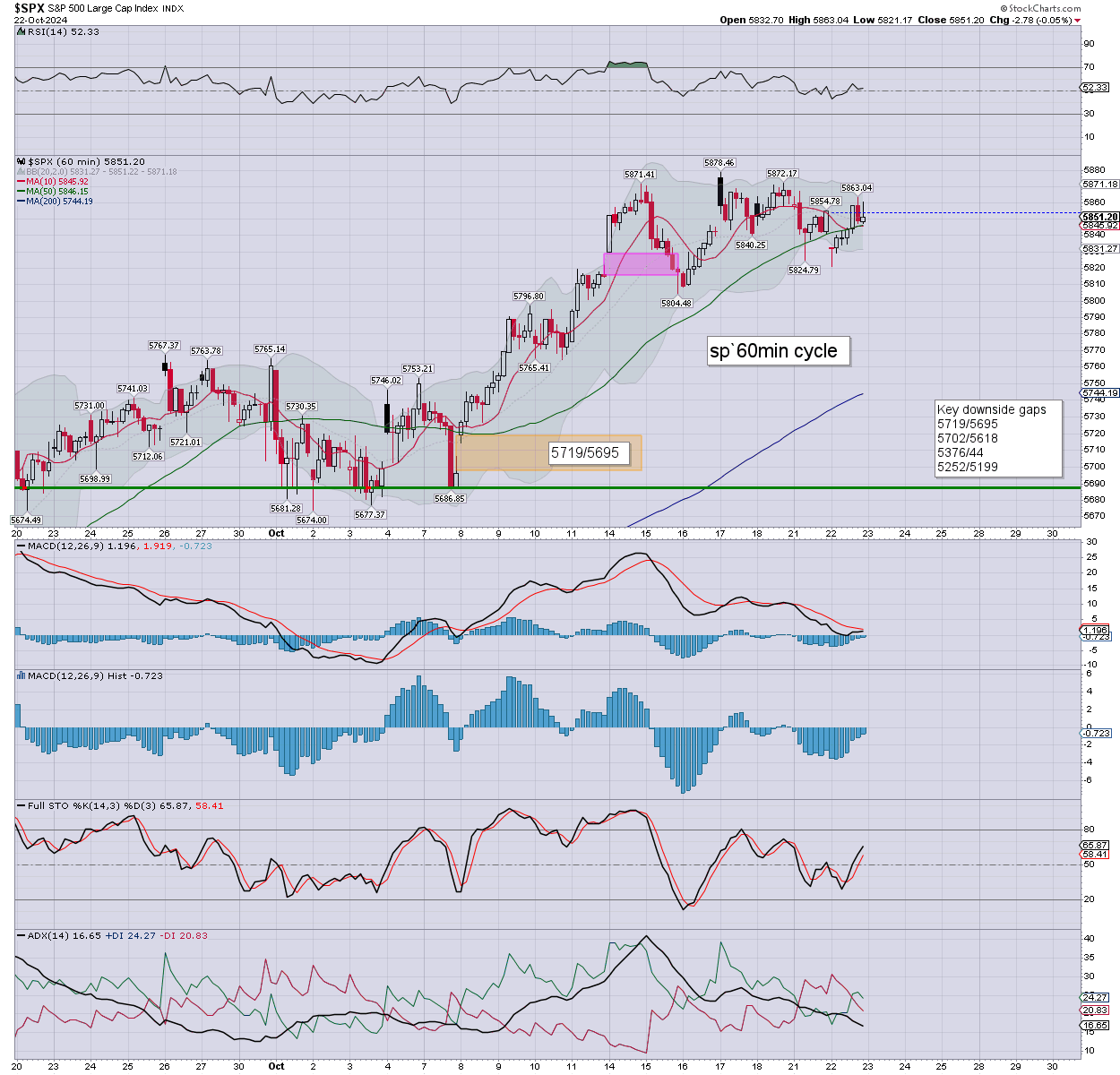

sp’60min

Summary

Yesterday opened on a weak note, but there was a recovery… if still settling fractionally lower. S/t momentum settled fractionally negative.

Overnight futures have been leaning on the weaker side, we’re set to open -15pts or so. The s/t cyclical setup favours the bulls, and it won’t take much to see indexes turn positive.

Today’s big event… Tesla earnings, due in AH. I wonder if Elon ever gets stressed about the laggy stock price? Perhaps he is more focused on Starship test’6, seemingly due within the next four weeks!

—

Early movers

AAPL -0.5%

AG -1.3%

ARM -3.5%, ending deal with QCOM

–

BA -0.6, EPS -$10.44 vs -10.34est. Rev’ y/y -1.7% to $17.8bn vs 17.9bn. Boeing touts an order book of $500bn

–

BSX +1.1%, EPS 63cents vs 59est. Rev’ $4.209bn vs 4.039est.

–

COIN -2.2%

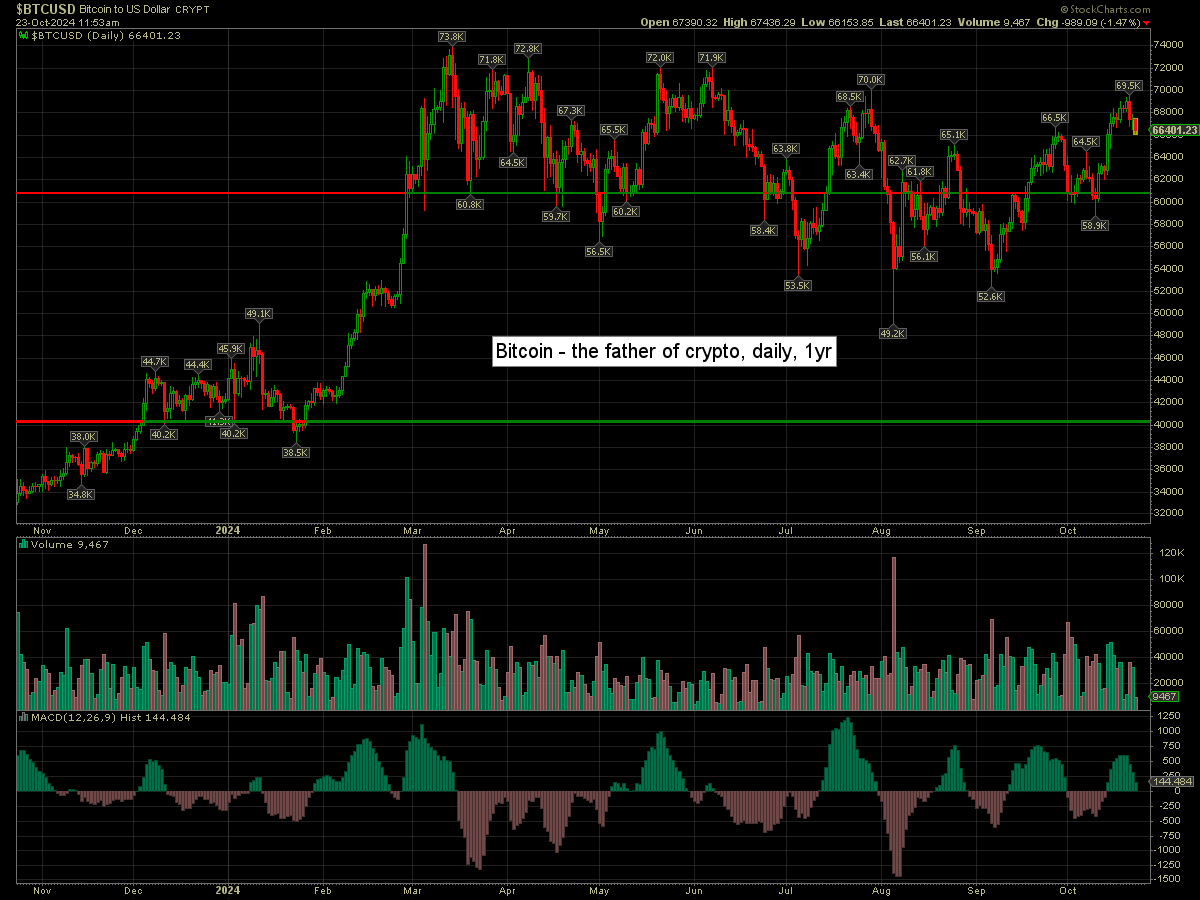

Bitcoin is -1.5% at $66401

–

DJT +3.5%, another day closer

ENPH -15.4%, post earnings upset

FCX -1.6%, with copper -4cents to $4.34

FSLR -1.2%, in sympathy with sister Enphase

–

GD -1.0%, EPS $3.35 vs 3.53est. Rev’ y/y +10.4% to $11.67bn v 11.64est.

–

GOLD +0.2%

–

KO -2.1%, EPS 77cents vs 74est. Rev’ y/y -0.4% to $11.9bn vs 11.6est.

–

LRN +24.1%, EPS 94cents vs 20est. Rev’ y/y +14.8% to $551M vs 506est.

–

MCD -6.8%, E-coli problems, which have harmed dozens, and maybe killed one.

–

NNE -1.9%

NVDA -0.7%

OKLO -4.2%

QCOM -3.3%, lost deal with ARM

RUM +7.5%

–

SAVE +26.5%, spurious gain for a company that has no realistic hope of a l/t future

–

SBUX -3.5%, earnings (Tues’ AH), EPS 80cents vs 1.03est. Rev’ y/y -3.2% to $9.07bn vs 9.37est. Guidance dropped.

–

SMR -3.3%

SNAP +2.4%

STX -4.1%, post earnings depression

–

T +3.3%, EPS 60cents vs 57est. Rev’ y/y -0.05% to $30.21bn vs 30.45est. Global COMPS y/y-7.0%

–

TSLA -0.5%, earnings due in AH

TXN +2.6%, post earnings gains

UAL -0.4%

–

VIX +1.1% at 18.58

–

VRT -7.3%, EPS 76cents vs 69est. Rev’ y/y +19.0% to $2.074bn vs 1.977est. Positive guidance.

–

WGO -7.0%, EPS 28cents vs 89est. Rev’ y/y -6.5% to $721M vs 719est. Soft guidance

–

XOM -0.4%

—

Overnight markets

Asian markets were mixed, whilst European markets are leaning a little weak…

Japan: -0.8% to 38104

China: +0.5% to 3302

Germany: currently -0.1% to 19397

UK: currently -0.4% to 8274

—

Have a good Wednesday