Good morning. US equity futures are a little weak (ahead of CPI), SPX -13pts, we’re set to open at 5482. USD is -0.2% at DXY 101.01. The precious metals are leaning upward, Gold +0.2% (printing $2558), with Silver +1.4% (printing $29.22). WTIC is +1.5% in the low $67s.

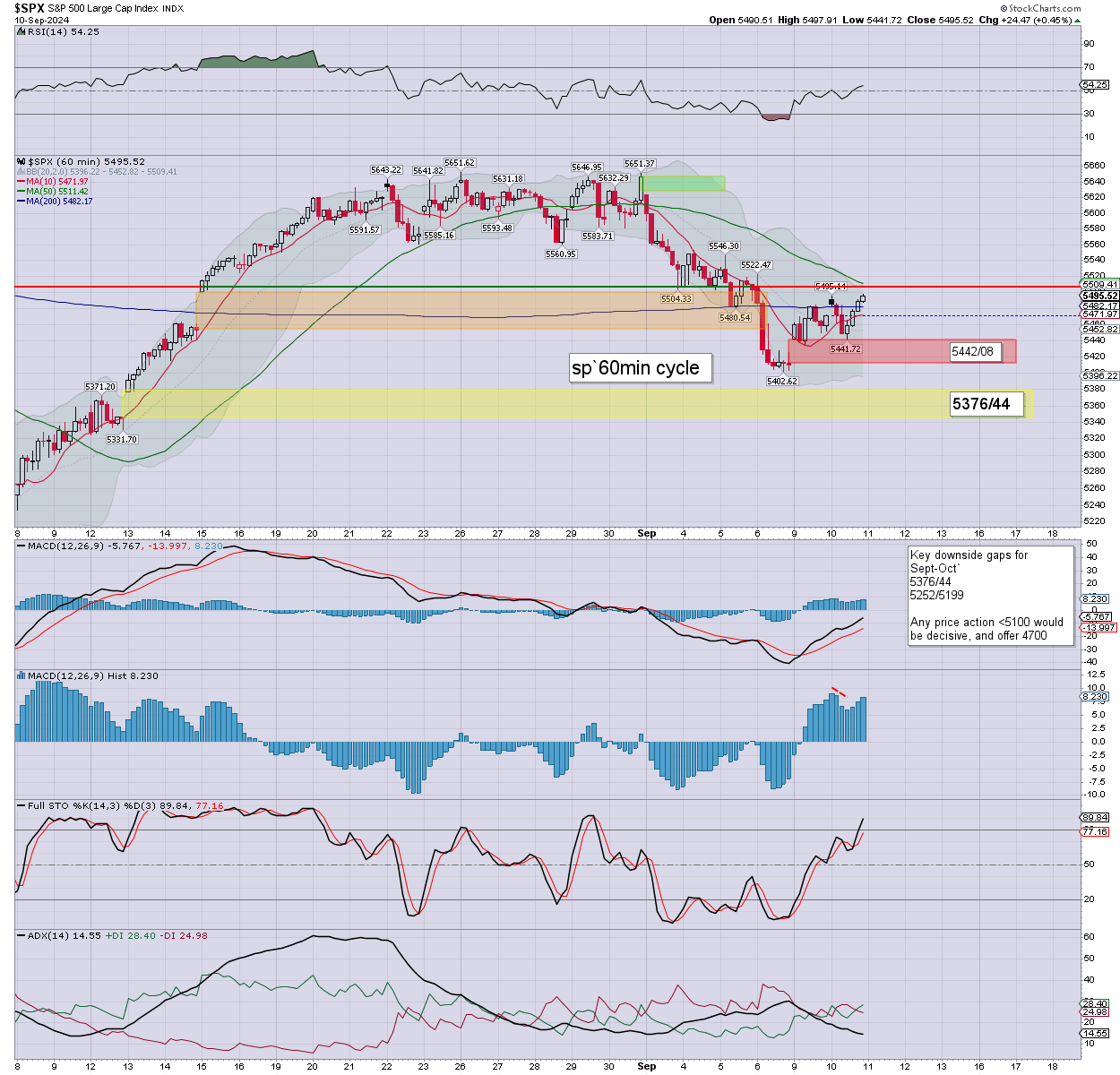

sp’60min

Summary

Yesterday saw a few swings, with indexes settling rather mixed. The SPX saw s/t momentum tick upward into the close, settling on the very high side.

Overnight futures have been leaning a little weak.

CPI is due 8.30am… consensus:

Headline y/y: 2.6% vs 2.9% prior

Core y/y: 3.2% vs 3.2% prior

Some are still hoping for rate cut’1 of -50bps.

On no realistic scenario does that look possible.

Lets see if we get a pre-FOMC washout. Natural target remains a tag of yellow gap, ideally to around the 5350s.

—

Early movers

AAPL -0.2%

ALB +8.1%, major Chinese lithium mine suspends production

ALLY +0.4%, dead cat bouncing

–

ARKB -2.0%

BAC -0.6%

–

COIN -2.2%

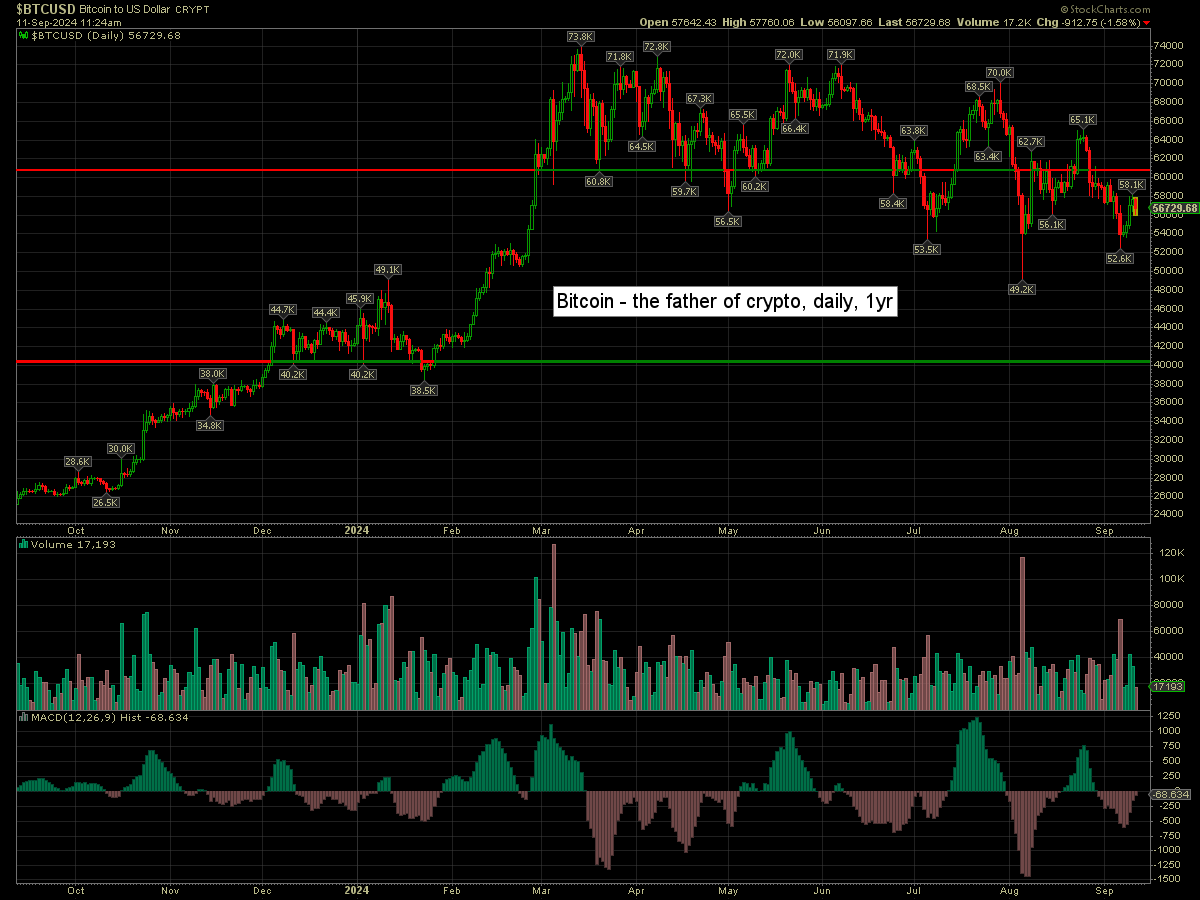

Bitcoin is currently -1.6% at $56729

–

DJT -10.6%, post debate upset

–

FCX +0.8%, with copper +5cents to $4.15

GME -11.0%, post earnings upset

GOLD +0.5%

INTC -0.3%, underlying weakness

–

LAC +8.1%

JPM -0.4%

MARA -3.1%

OXY +0.6%

–

PLL +5.5%

PLTR -2.2%

RIG +3.8%, $232M contract with BP in the Gulf of Mexico

–

RLAY -20.0%, $200M secondary offering

ROKU +2.3%

SLB +0.4%

–

SQM +8.9%

TSLA -0.4%

UNG -0.7%, with Natgas $2.21

–

VIX +1.5% at 19.36

–

XOM +0.6%

—

Overnight markets

Asian markets were broadly lower, whilst European markets are leaning upward…

Japan: -1.5% to 35619

China: -0.8% to 2721

Germany: currently +0.4% at 18343

UK: currently +0.1% at 8212

—

Have a good Wednesday