Good morning. US equity futures are leaning weak, SPX -19pts, we’re set to open at 5694. USD is +0.2% at DXY 100.59. The precious metals are significantly higher, Gold +0.9% (printing a new hist’ high of $2640), with Silver +1.5% (printing $31.67). WTIC is -0.4% in the upper $70s.

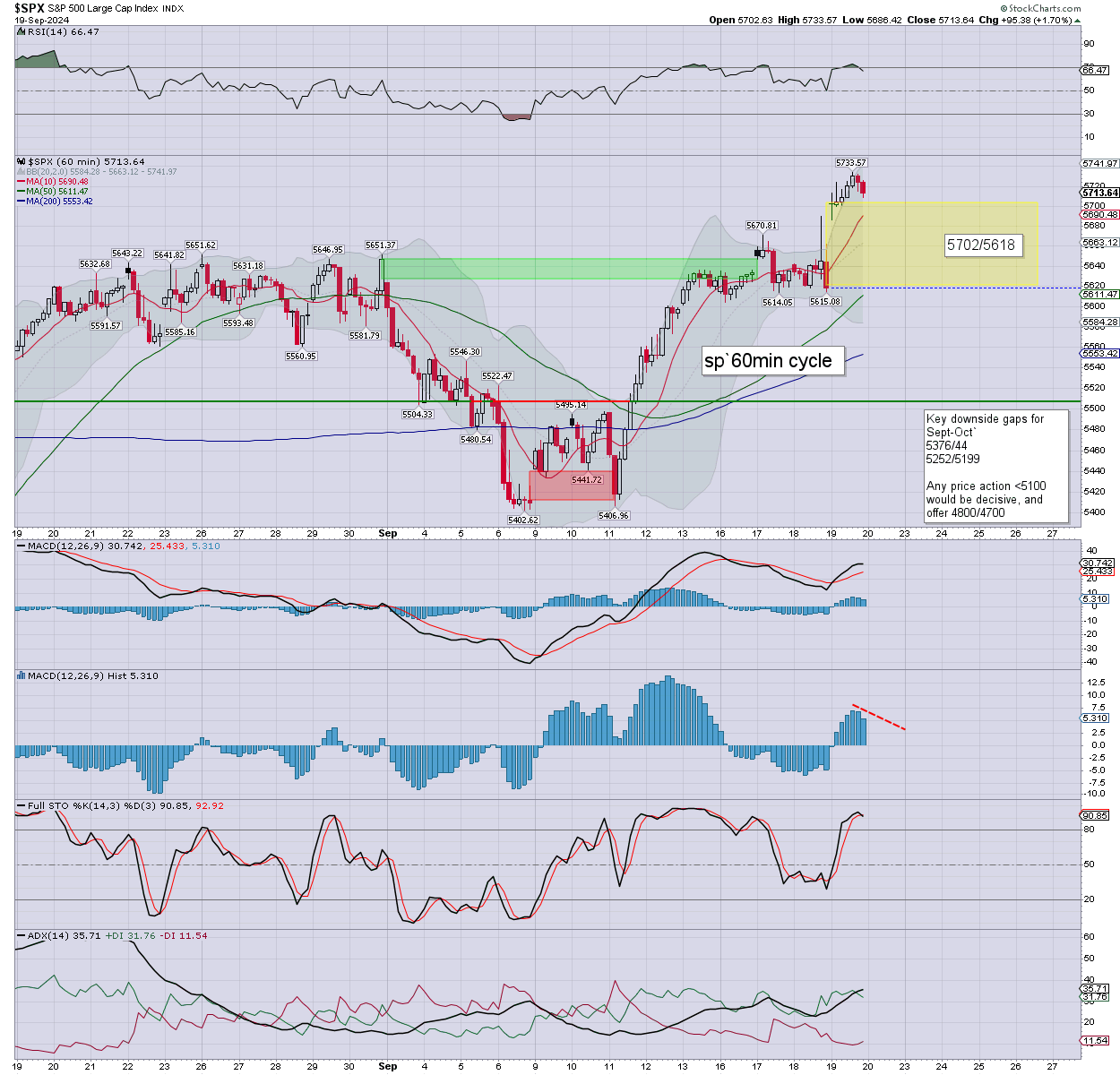

sp’60min

Summary

Yesterday saw a net hist’ high of 5733, with a little cooling into the close, settling at 5713. S/t momentum rolled over, settling on the moderately high side.

Overnight futures have been leaning on the weaker side, we’re set to open -15/20pts.

Today is quadruple option expiration – quad-opex. We can expect considerable chop on VERY HEAVY vol’. There will be some index rebalancing as of the close.

The s/t cyclical setup favours the bears, with momentum prone to turning negative by early afternoon. We should look for a pin around psy’5700, or intermediate psy’5650… on a stretch.

Last Sunday saw Trump shooter’2, and I have to wonder what kind of ‘weekend surprise’ we’ll get this weekend. I’m sure there will be something.

—

Early movers

AAPL -0.5%

AG +2.0%

ALB -1.1%

AMAT -0.9%

BABA +1.0%

–

BAC -0.3%

CCJ +5.7%, news?

CHWY -1.9%

–

COIN +0.9%

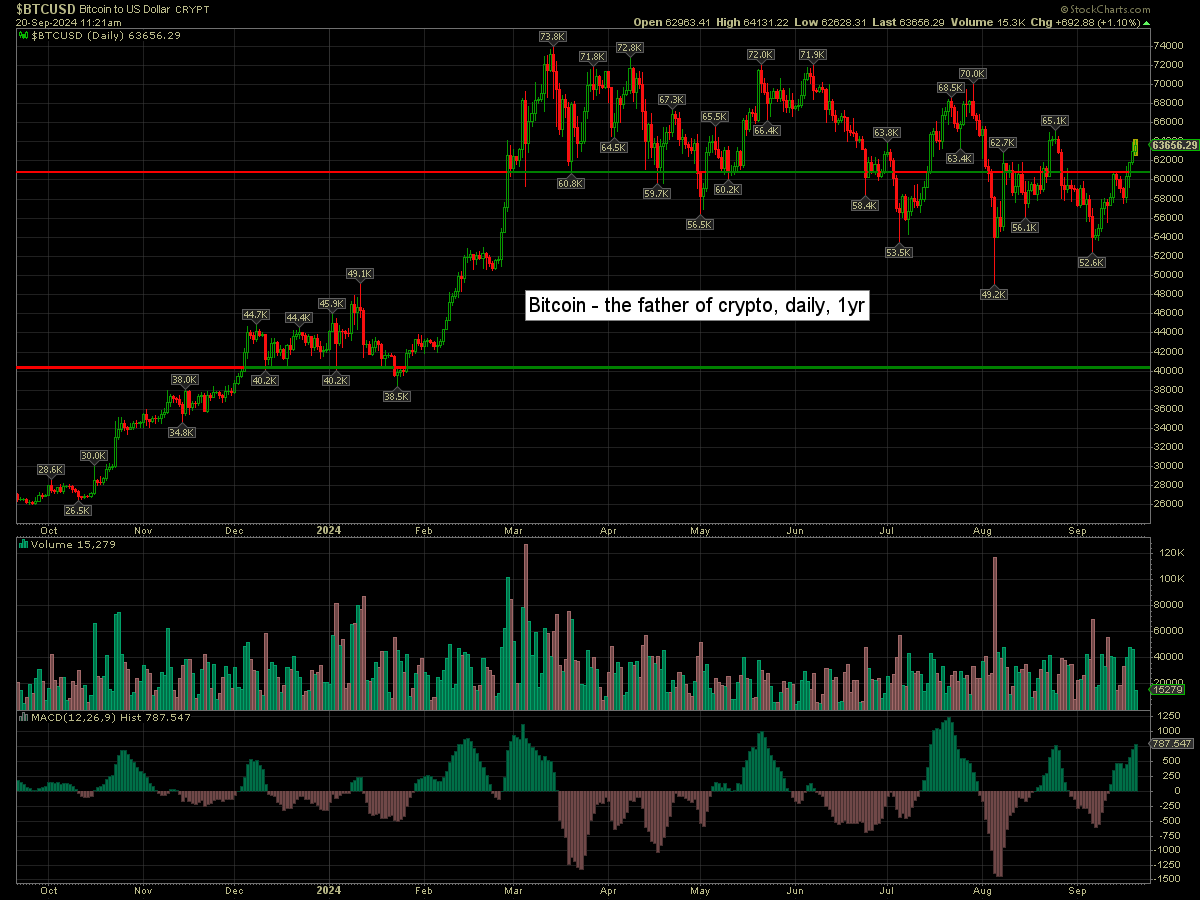

Bitcoin is currently +1.1% at $63656. S/t bullish unless <60k.

–

DJT -4.3%

FCX u/c, with copper +2cents to $4.36

–

FDX -12.6%, post earnings horror

GOLD +1.2%

HAFN -4.9%

INTC -0.8%

–

LEN -2.8%, post earnings depression

MU -0.4%

NEM +1.5%

NKE +6.6%, new CEO (Elliott Hill, as of Oct’14)

–

NVDA -0.9%

PLTR -2.2%, … despite Army contract, $99.8M

TSLA -0.6%

TSM -0.9%

–

UEC +1.5%

UNG +0.1%, with Natgas $2.34

UPS -2.4%, in sympathy with FedEx

–

VFS -1.8%, EPS -33cents vs -22est, and vs -24 prior yr. Rev’ $352M vs 328 prior yr. Lousy.

–

VIX +0.4% at 16.40

—

Overnight markets

Asian markets were rather mixed, whilst European markets are broadly lower…

Japan: +1.5% to 37723

China: +0.03% to 2736

Germany: currently -0.9% at 18838

UK: currently -0.5% at 8287

—

Have a good Friday