Good morning. US equity futures are broadly lower, SPX -37pts, we’re set to open at 5518. USD is -0.02% at DXY 104.15. The precious metals are a little higher, Gold +$5, with Silver +0.3%. WTIC is +0.5% in the $77s.

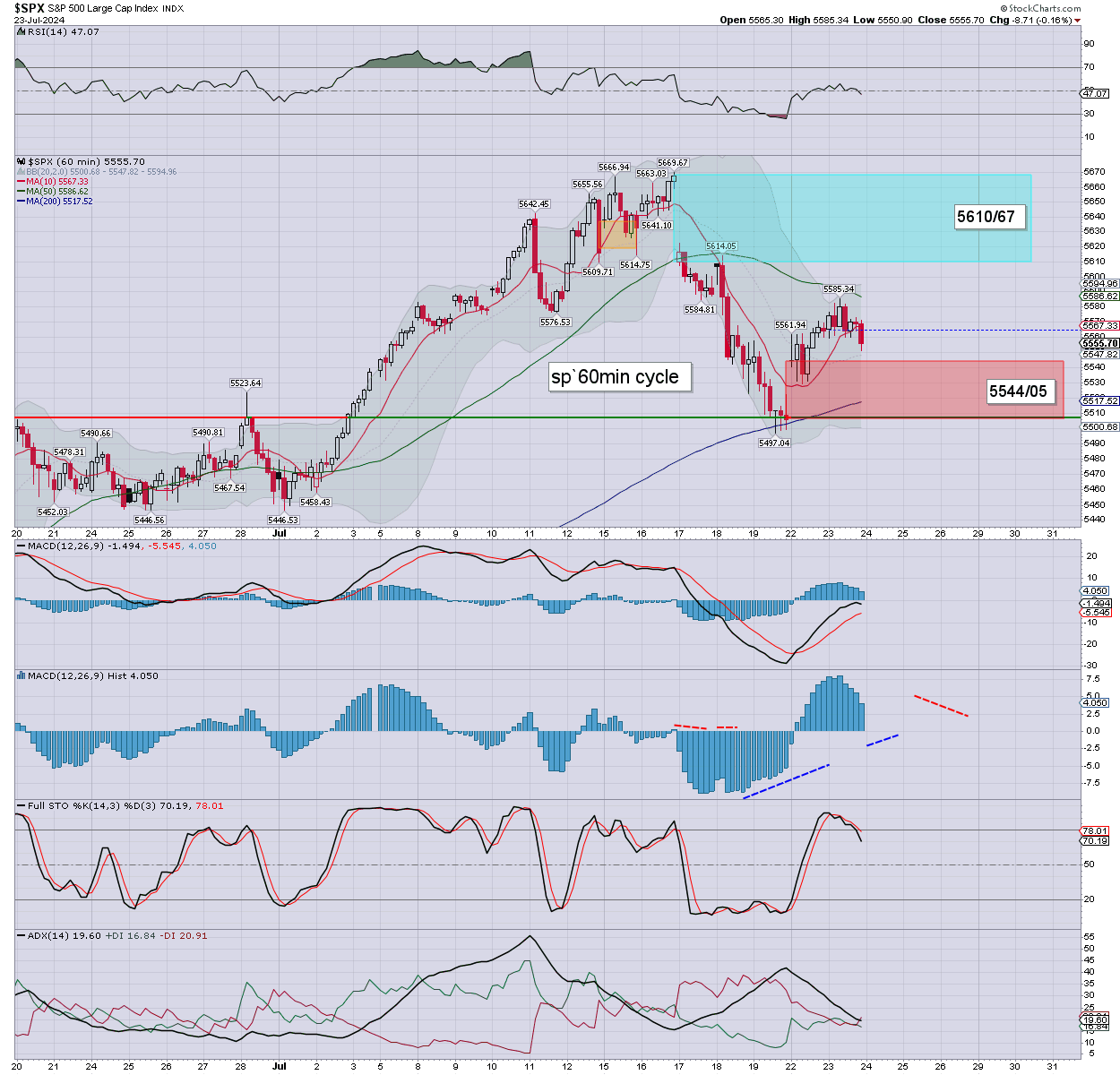

sp’60min

Summary

Yesterday saw considerable chop, settling a little weak. S/t momentum weakened across the day, if still settling on the moderately high side.

Overnight futures have turned broadly lower, pressured by world markets, and somewhat by Tesla.

Ohh, and lets be clear, Tesla earnings were ‘mixed’ at best. I even saw someone else on X last night also note the valuation is ludicrous, with an FPE somewhere north of 100. On any basis… crazy.

In any case… we’re set to open -40pts or so, to tag red gap.

Two scenarios:

1. straight down to the 5440s

2. bounce from red gap, tag upside teal gap, and then resume lower to the 5440s.

I’m guessing the latter, as it’d cause max confusion, and if anything… Mr Market likes to wash out the most number of bulls AND bears. It should be an interesting day.

—

Early movers

AMD -1.3%… sustainably under the 200dma.

–

BSX +1.0%, EPS 62cents vs 58est. Rev’ y/y +14.5% to $4.1bn vs 4.0est. Positive guidance.

–

CB +0.9%, post earnings gains

CMG +0.1%, earnings due in AH

–

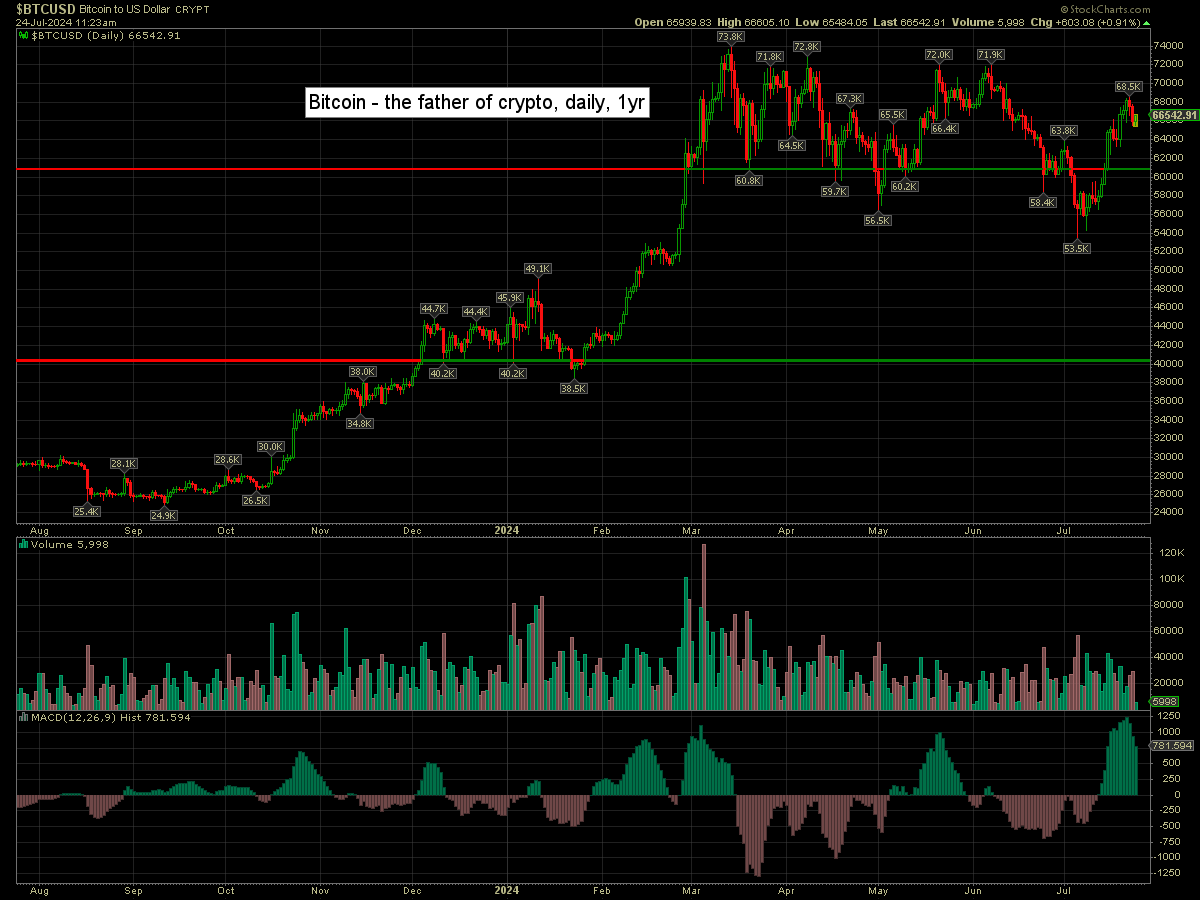

COIN +1.1%

Bitcoin is currently +0.9% at $66542

–

CRWD +0.8%, Crowdstrike blames ‘bug in quality control process’ caused the ‘bad data’ in a recent update. Wedbush, 385>315

–

DB -4.6%, garbage earnings.

DIS -0.3%

DJT -3.3%

ENPH +3.7%, post earnings gains

–

F -1.3%, in sympathy with Tesla. Earnings due in AH

FCX +0.2%, with copper u/c at $4.15

–

GD -0.7%, EPS $3.26 vs 3.28est. Rev’ y/y +18.0% to $12.0bn vs 11.5est. Broadly fine on higher defense demand.

–

GOOGL -3.6%, post earnings depression

GOLD +0.5%

INTC -0.9%

META -2.1%, concerns about EU regulators

MU -1.8%

NEM +0.6%… earnings due in AH

–

NFLX -0.5%

NVDA -1.7%

RIVN -3.4%, in sympathy with Tesla

SAN +2.2%, post earnings gains

SNAP -2.1%

–

SPOT +0.8%, Morgan Stanley, 370>400, Goldman, 320>425, Macquarie, 345>395

–

STX +4.8%, post earnings gains

–

T +2.7%, EPS 57cents inline. Rev’ y/y -0.3% to $29.8bn vs 30.0est. Guidance held.

–

TGT -0.5%

–

THC +5.1%, EPS $2.31 vs 1.90est. Rev’ y/y +0.4% to $5.1bn vs 5.0est. Positive guidance

–

TMO -3.1%, EPS $5.37 vs 5.12est. Rev’ y/y -1.4% to $10.5bn inline. Guidance inline.

–

TSLA -8.2%, post earnings upset

–

TXN +1.3%, post earnings gains

–

UNG -3.8%, with Natgas $2.11

V -3.4%, post earnings depression

–

VIX +4.0% at 15.30

–

VRT-3.3%, EPS 67cents vs 57est. Rev’ y/y +12.6% to $1.95bn vs 1.94est. Positive guidance.

—

Overnight markets

Asian markets were broadly lower, whilst European markets are leaning weak…

Japan: -1.1% to 39154

China: -0.5% to 2901

Germany: currently -0.7% at 18426

UK: currently -0.2% to 8153

—

Have a good Wednesday