Good morning. US equity futures are fractionally higher, SPX +6pts, we’re set to open at 5570. USD is +0.1% at DXY 104.15. The precious metals are leaning upward, Gold +$10, with Silver -0.1%. WTIC is -0.1% in the $82s.

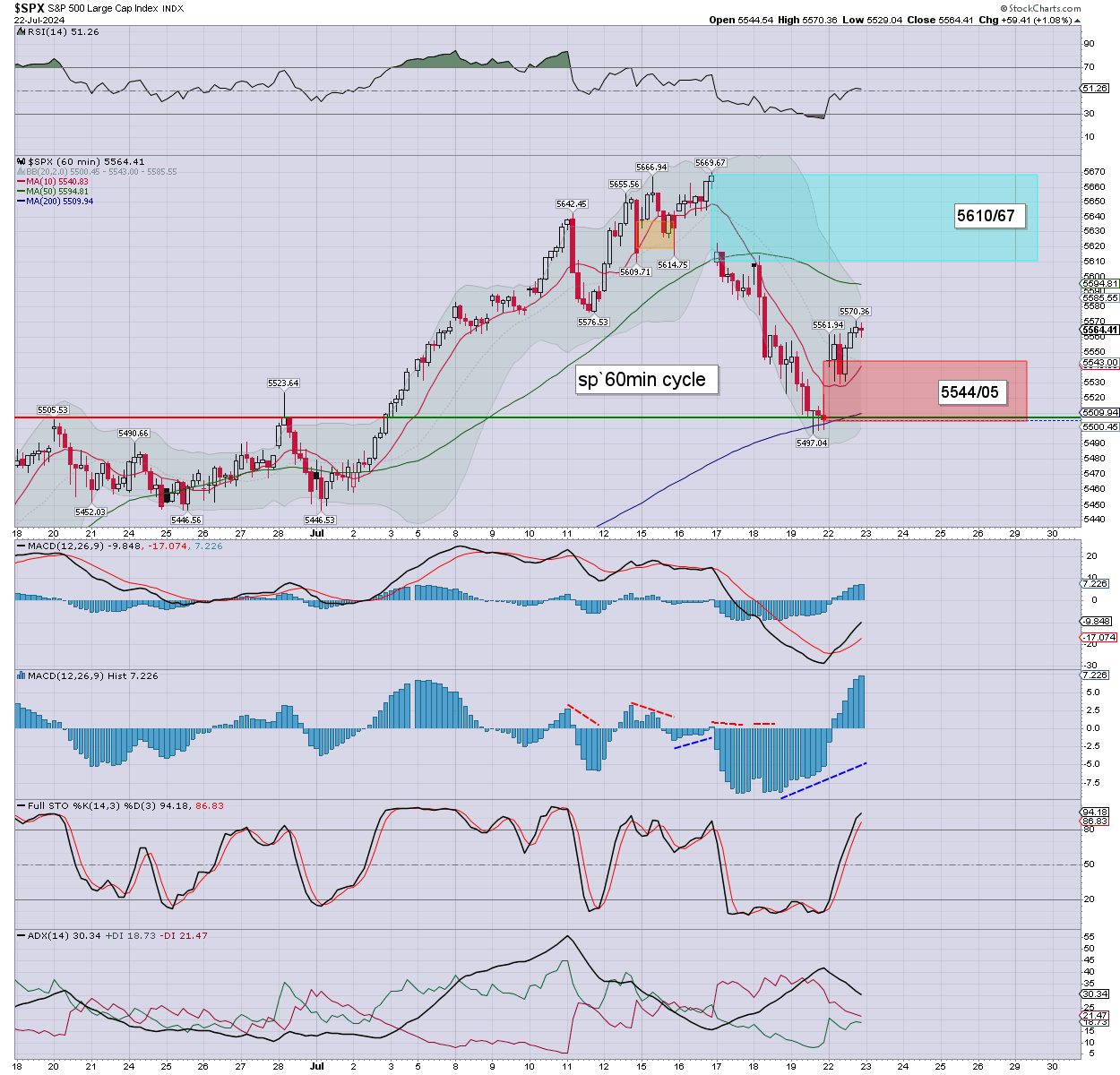

sp’60min

Summary

Yesterday was pretty choppy… if managing significant gains. S/t momentum settled on the high side.

Overnight futures have been subdued, we’re set to open fractionally higher.

I’d be open to some cooling, before a secondary wave higher to tag teal gap, and then resuming lower to the 5450s.

—

Early movers

AMC -1.5%

AMD -0.7%, President Peng leaving in August

–

BABA -1.0%, weak Chinese stocks

BIDU -1.6%

CCK +7.1%, post earnings gains

CELH +0.7%, Jefferies, 98>68

–

CLF +0.2%, earnings (Monday AH): EPS 11cents vs -1est. Rev’ y/y -14.9% to $5.1bn vs 5.2est.

–

CMCSA -0.4%, EPS $1.21 vs 1.12est. Rev’ y/y -2.7% to $29.7bn vs 30.0est.

–

COIN -0.5%, Citi, neutral>buy, 260>345

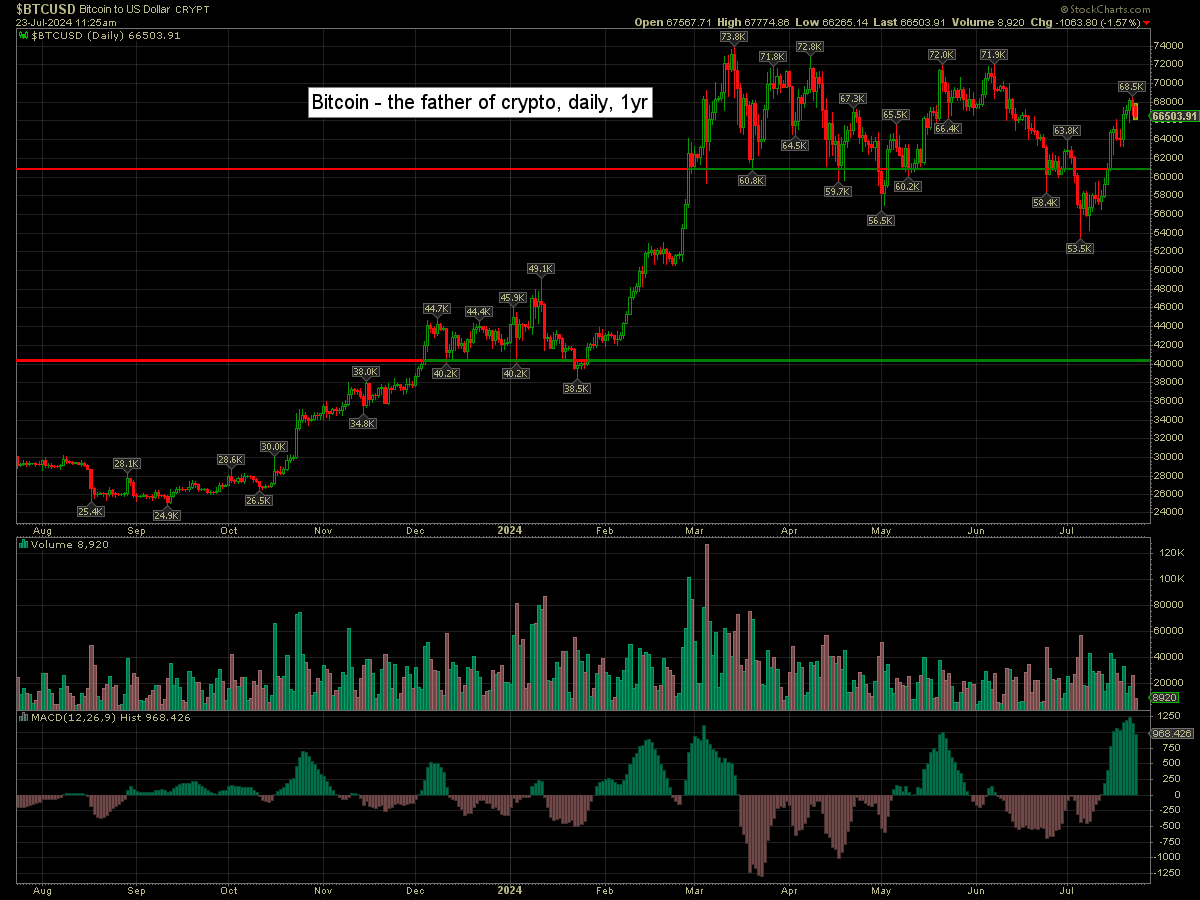

Bitcoin is -1.6% at $68503.

–

CRWD +0.1%, Baird, 350>335, Capital One, 421>340, Truist, 400>325. Having lost the 200dma, all those targets are still ludicrously high.

–

DIS -0.7%, mostly due to Comcast earnings

DJT -3.5%

F +1.8%

–

FCX -0.3%, EPS 46cents vs 40est. Rev’ y/y +15.5% to $6.6bn vs 6.0est. Copper -2cents to $4.17

–

FDX -1.8%, in sympathy with UPS

–

GE +2.1%, EPS $1.20 vs 0.99est. Rev’ y/y +3.9% to $9.1bn vs 8.4est. Guidance raised. Strong engine part demand.

–

GM +4.8%, EPS $3.06 vs 2.71et. Rev’ y/y +7.2% to $48.0bn vs 45.1est. Positive guidance.

–

GOLD +0.6%

–

HCA +7.7%, EPS $5.50 vs 4.93est. Rev’ y/y +10.3% to $17.5bn vs 17.0est. Positive guidance.

–

INTC -0.6%

–

KO +1.5%, EPS 84cents vs 81est. Rev ‘y/y +3.3% to $12.4bn vs 11.8est. Guidance inline… on steady demand.

–

LMT +2.2%, EPS $7.11 vs 6.46est. Rev’ y/y +8.6% to $18.1bn vs 17.0est. Guidance leaning positive.

–

MEDP -13.1%, post earnings horror

MU -0.4%

–

NXPI -8.1%, earnings (Monday AH), EPS $3.20 inline. Rev’ y/y -5.2% to $3.1bn inline. Q3 rev’ guidance a little weak on auto weakness.

–

PHM +1.9%, EPS $3.83 vs 3.27est. Rev’ y/y +9.8% to $4.6bn vs 4.5est.

–

PII -11.1%, EPS $1.38 vs 2.25est. Rev’ y/y -11.5% to $1.96bn vs 2.18est. Lousy guidance.

–

PM +2.6%, EPS $1.59 vs 1.57est. Rev’ y/y +5.6% to $9.5bn vs 9.2est. Guidance inline.

–

QCOM +1.2%, Baird, 200>250

SAP +6.1%, post earnings gains

SNAP +3.2%, Morgan Stanley, 12>16

–

SPOT +13.4%, EPS €1.33 vs 1.05est, and vs -1.55 prior yr. Rev’ €3.8bn inline, and vs 3.2 prior yr. A distinct improvement.

–

TSLA +1.2%, earnings due in AH

TSM +1.1%

TXN -2.4%, earnings due in AH

UAA -3.3%, Morgan Stanley, 8>4

UAL -0.6%

–

UPS -8.5%, EPS $1.79 vs 1.99est. Rev’ y/y -1.1% to $21.8bn vs 22.2est. A double miss. Guidance somewhat positive. Restarting buyback, $1bn a year. Desperate measure.

–

VIX -0.1% at 14.90

–

X +0.7%

ZION +3.7%, post earnings gains

—

Overnight markets

Asian markets were mixed, whilst European markets are broadly higher…

Japan: -0.01% to 39594

China: -1.6% to 2915

Germany: currently +1.2% at 18622

UK: currently +0.3% at 8225

—

Have a good Tuesday.