Good morning. US equity futures are broadly flat, SPX -4pts, we’re set to open at 5629. USD is -0.2% at DXY 104.56. The precious metals are leaning upward, Gold +$8, with Silver +0.5%. WTIC is u/c in the mid $82s.

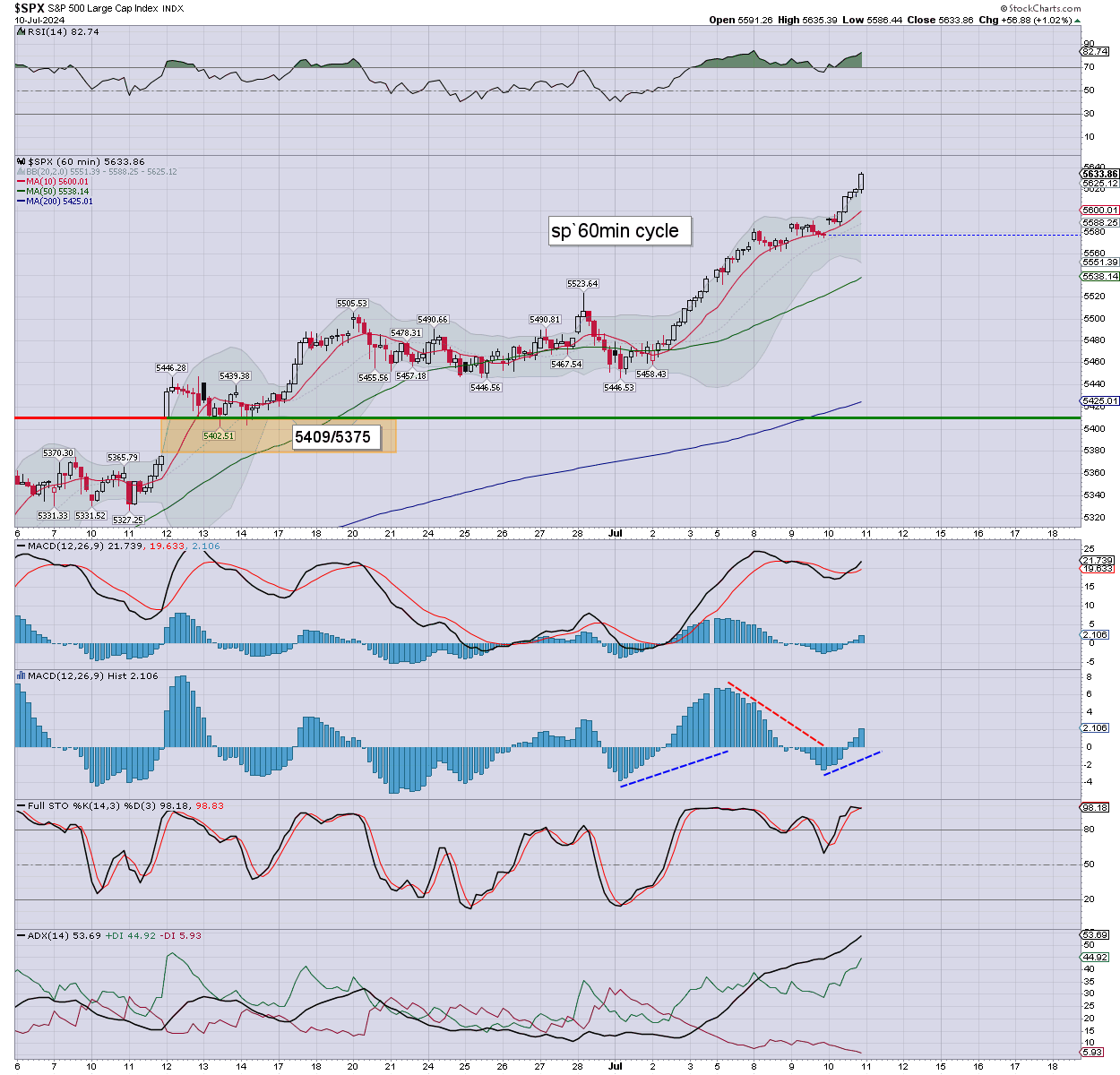

sp’60min

Summary

Yesterday was a mere continuation… with algo-bot upward melt, breaking a new hist’ high. S/t momentum settled on the moderately high side.

Overnight futures have been subdued… with the market naturally churning ahead of CPI. Regardless of that data, its starting to become clear the Fed will cut in Sept’ and Dec’.

—

Early movers

AA +1.9%, prelim earnings

AAL -4.2%, in sympathy with Delta

AAPL -0.3%

AG +1.1%

ALB -1.3%, Wells Fargo, 145>100

AMD -0.4%

–

BABA +1.5%

BIDU +1.9%

–

CAG -3.5%, EPS 61cents 57est. Rev’ $2.9bn inline. Outlook leaning weak on ‘tepid demand’.

–

COIN +0.7%

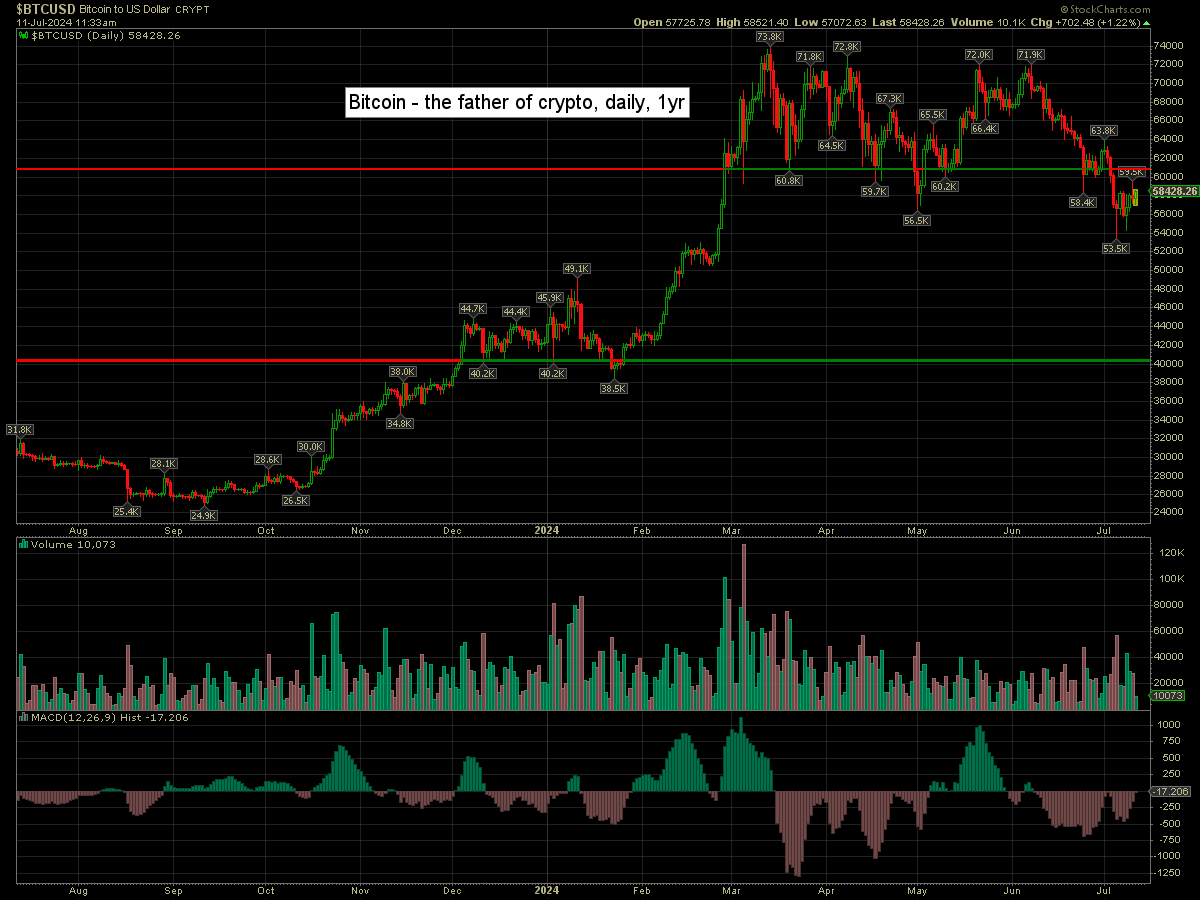

Bitcoin is currently +1.2% at $58428. Momentum due to turn positive.

–

COST +2.6%, increasing annual membership fee, 60>65, and 120>130. A truck load of subsequent upgrades, inc’. Jefferies, 860>1050, Baird, 850>975

–

DAL -9.6%, EPS $2.36 vs 2.37est. Rev’ y/y +5.4% to $15.4bn inline. Weak guidance.

–

EXK -1.7%, just a retrace.

FCX +0.4%, with copper -3cents to $4.57

GOLD +0.6%

HL +0.9%, prod’ data.

–

INTC -0.7%

LUV -2.7%, in sympathy with Delta

NEM +0.6%

NIO +2.4%

NVDA +0.5%

PAAS +0.6%

–

PFE +1.8%, Pfizer pushing ahead with a ‘once daily’ weight loss pill, for the fat western populace.

–

PEP -1.9%, EPS $2.28 vs 2.16est. Rev’ y/y +0.8% to $22.5bn vs 22.6est. Guidance inline.

–

QS +40.0%, deal with PowerCo of Volkswagen to ramp up production of solid state batteries. Effectively, QS will receive royalites on the licensed technology. VW owns 17% of QS, so they will ironically (partly) be paying themselves.

–

SLB +0.3%

UAL -4.6%, in sympathy with Delta

–

VIX +1.0% at 12.98

–

WDFC +11.5%, post earnings jump

—

Overnight markets

Asian markets were broadly higher, whilst European markets are a little higher…

Japan: +0.9% to 42224

China: +1.1% to 2970

Germany: currently +0.2% at 18441

UK: currently +0.3% at 8217

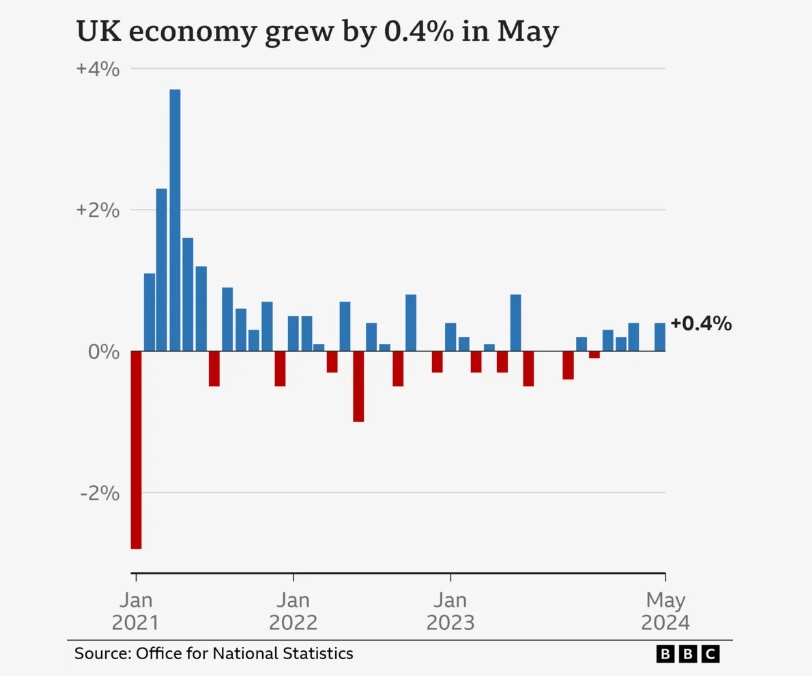

> https://www.bbc.co.uk/news/articles/cp682nprlw7o

May GDP +0.4%… but broadly, its been a flat-lining economy since early 2022…

Strip out the Govt’ deficit spending, and the ‘real economy’ is -4% or so… much like the USA.

Meanwhile…

https://x.com/davidkurten/status/1811322919470964845

… as Starmer gives Ukraine permission to use UK missiles to strike Russia.

The UK, not least its capital of London, is a valid military and civilian target.

I hope it gets incinerated. The sooner the better.

—

Have a good Thursday