Good morning. US equity futures are a little higher, SPX +8pts, we’re set to open at 5018. USD is -0.05% at DXY 105.86. The precious metals are significantly lower, Gold -$25 (printing $2304), with Silver -1.3% (printing $26.72). WTIC is -0.7% in the $81s.

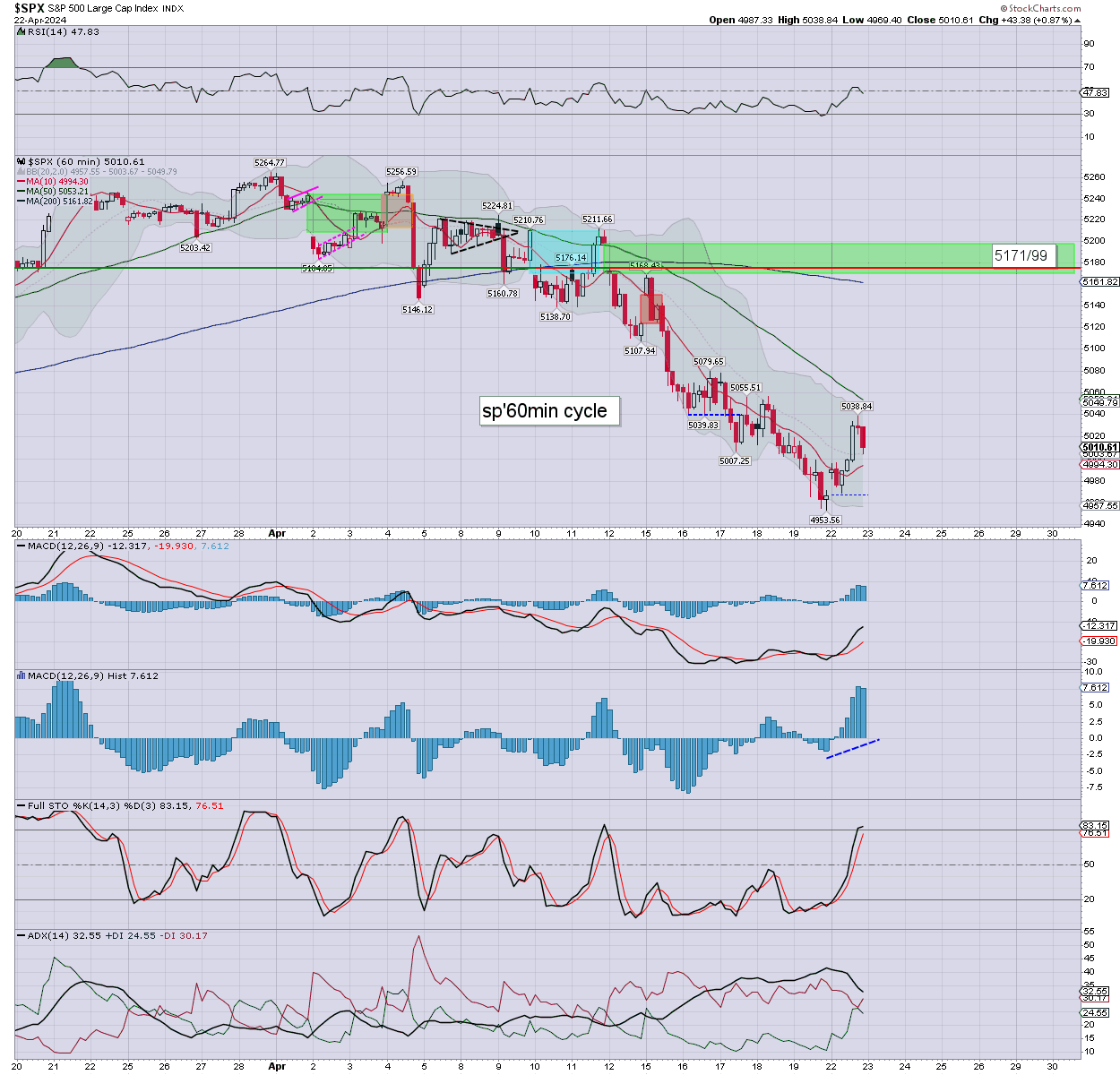

sp’60min

Summary

Yesterday saw the market bounce, with s/t momentum settling on the high side.

Overnight futures have been leaning on the upward side, we’re set to open +5/10pts. First resistance is around 5050.

The only issue is whether we’re in the early phase of a bigger bounce to around 5200. The daily charts certainly offer it. The concern should be geo-political.

—

Early movers

AA -2.7%

AAL -2.1%

AAPL -0.3%

AG -2.3%

–

AMD +2.3%

AMZN +0.7%

–

CDNS -6.6%, post earnings depression

CLF -2.5%, post earnings depression

–

COIN -1.1%

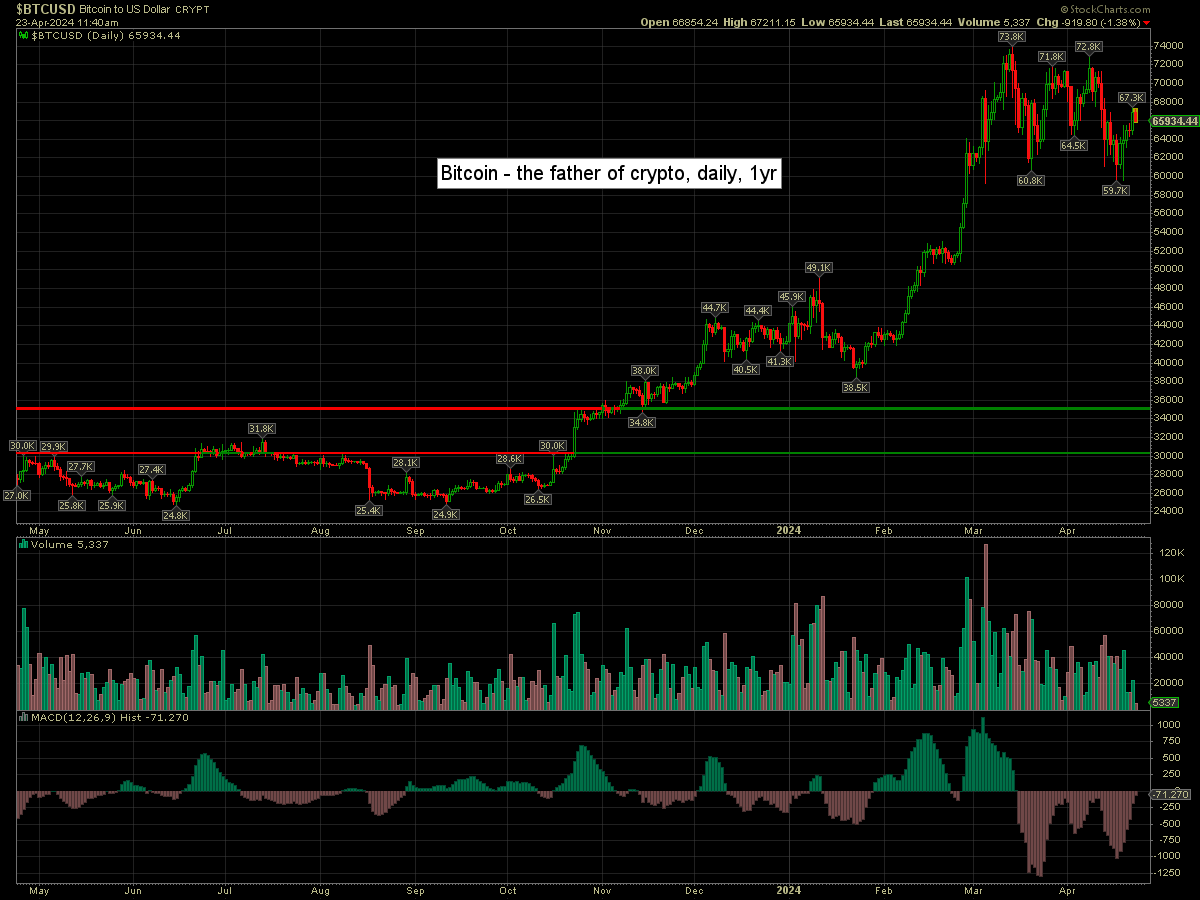

Bitcoin is currently -1.4% at $65934.

–

DIS +1.0%, Wells Fargo, overweight, 128>141

F +1.9%, helped by GM

–

FCX -1.9%, EPS 32cents vs 27est. Rev’ y/y +17.3% to $6.3bn vs 5.7est. Broadly good. Copper -6cents to $4.41

–

FDX +0.7%, helped by UPS

–

GE +4.8%, EPS 82cents adj’ vs 70est. Rev’ $16.0bn vs 15.7est. Strong demand for jet engines.

–

GM +4.7%, EPS $2.62 vs 2.13est. Rev’ y/y +7.6% to $43.0bn vs 41.1est. Positive guidance.

–

GOLD -1.2%

–

HAL +0.7%, EPS 76cents vs 74est. Rev’ y/y +2.2% to $5.8bn vs 5.7est.

–

JBLU -10.0%, EPS -43cents vs -52est. Rev’ y/y -5.5% to $2.2bn inline. Weak guidance.

–

LMT +1.9%, EPS $6.33 vs 5.86est. Rev’ y/y +13.7% to $17.2bn vs 16.0est.

–

META +1.5%

NEM -1.5%

NUE -6.1%, post earnings depression

–

NVDA +1.4%

PENN +4.8%, Truist, hold>buy, $23

–

PEP -0.1%, EPS $1.61 vs 1.52est. Rev’ y/y +2.3% to $18.2bn vs 18.1est. Guidance held.

–

PHM +3.9%, EPS $3.10 vs 2.36est. Rev’ y/y +10.4% to $3.9bn vs 3.6est.

–

RBLX +4.2%, JPM, neutral>overweight, 41>48

–

RTX +0.6%, EPS $1.34 vs 1.23est. Rev’ y/y +12.1% to $19.3bn vs 18.5est. Guidance held.

–

SAP +3.8%, post earnings gains

SCCO -3.0%, lower copper

SMCI +1.8%

–

SPOT +8.3%, EPS 97cents vs 62est. Rev’ y/y +19.5% to $3.6bn inline. Premium subs y/y +14% to 239M. Active MAUs y/y +19% to 615M

–

TECK -3.5%, lower copper

TLT -0.4%, as yields climb

TSLA +0.3%

UAL -0.4%

–

UPS +0.8%, EPS $1.43 vs 1.30est. Rev’ y/y -5.3% to $21.7bn vs 21.8est. Guidance inline. The annual decline in rev’ should be a concern.

–

VIX -1.9% at 16.61

–

WBD -2.2%, Wolfe Res’, peer-perform>underperform, $7

—

Overnight markets

Asian markets were mixed, whilst European markets are broadly higher…

Japan: +0.3% to 37552

China: -0.7% to 3021

Germany: currently +1.1% at 18064

UK: currently +0.6% at 8070

—

Have a good Tuesday