Good morning. US equity futures are leaning weak, SPX -14pts, we’re set to open at 4961. USD is +0.05% at DXY 104.03. The precious metals are leaning upward, Gold +$4, with Silver +0.2%. WTIC is -0.5% in the $76s.

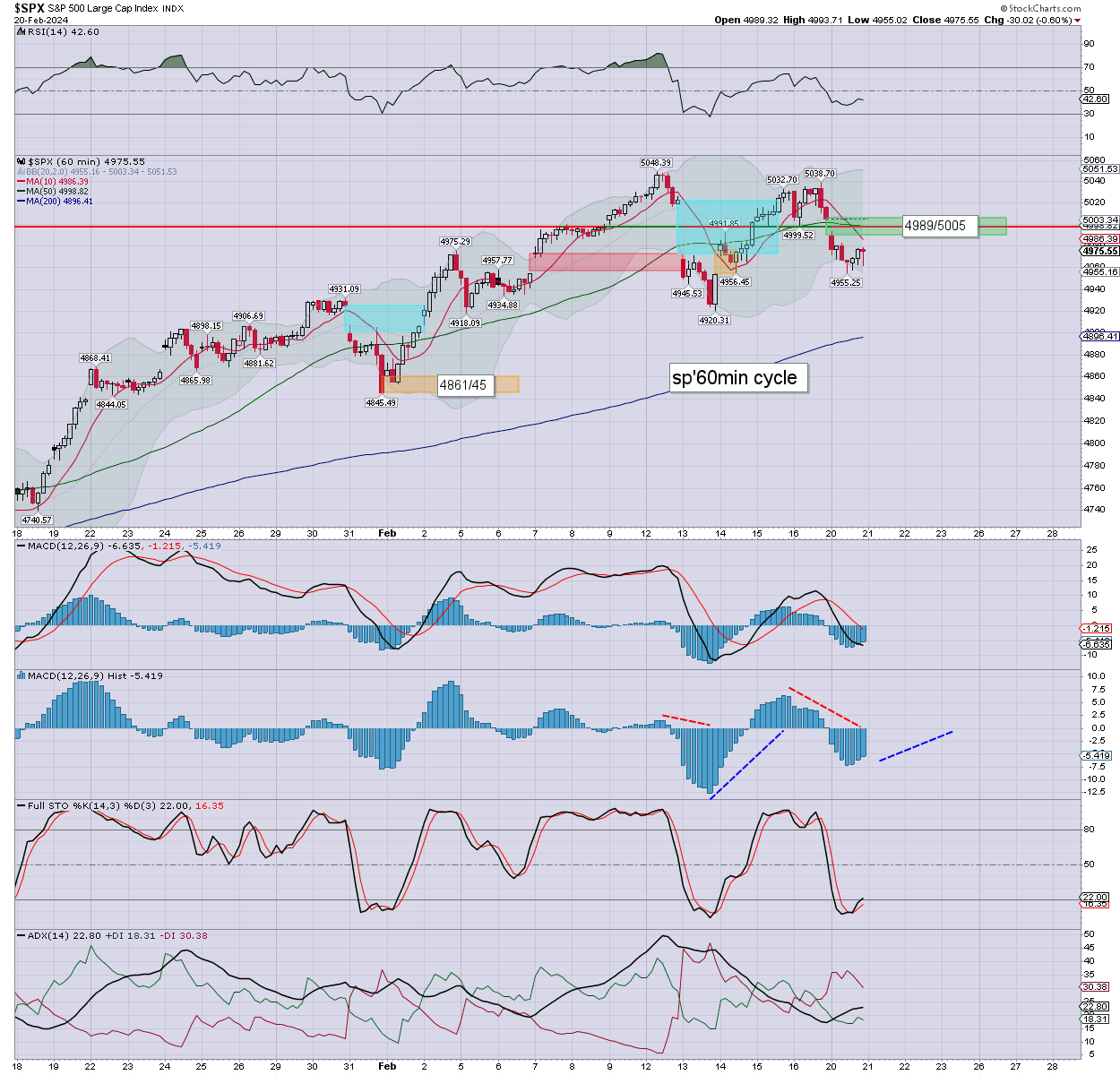

sp’60min

Summary

Yesterday opened weak, with a latter day recovery to settle moderately lower. S/t momentum settled on the low side. Structure offers a baby bear flag (set to play out), with next support around psy’ 4900.

Overnight futures have been choppy, if mostly leaning a little weak. We’re set to open -10/15pts.

Clearly, if Nvidia earnings aren’t at least inline with expectations, the market is going to have a… ‘difficult’ Thursday. For today though, we appear set for a net daily decline of some degree.

—

Early movers

ADI -1.3%, EPS $1.73 vs 1.70est. Rev’ y/y -22.7% to $2.5bn inline. Weak guidance. Divi +7% to 92cents

–

ALIT -7.1%, EPS 30cents vs 26est. Rev’ y/y +1.8% to $960M vs 1031est. Mixed guidance. Company to begin a ‘strategic review’, aka… ‘Will someone please buy us?’.

–

AMD -1.4%

–

AMZN +0.9%, Amazon to replace Walgreens in the Dow’30… as I’ve repeatedly suggested. Taking effect early Feb’26th. > https://en.wikipedia.org/wiki/Dow_Jones_Industrial_Average

–

ARM -2.9%

BABA +1.7%

CCJ -2.4%, weak Uranium miners

–

COIN -3.7%

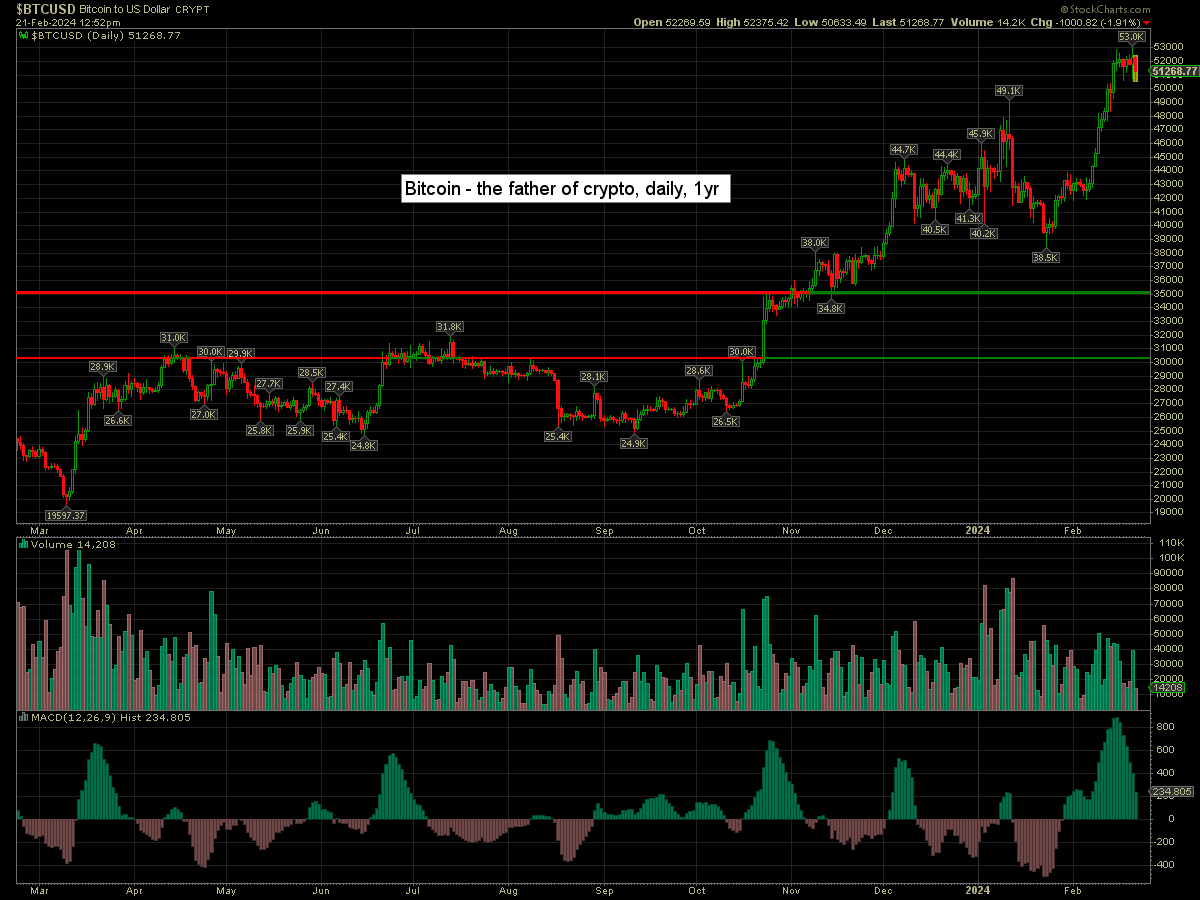

Bitcoin is -1.9% at $51268. Momentum might turn negative on Friday, and bodes problematic into the weekend.

–

CRWD -10.1%, in sympathy with Palo Alto

DIS -0.3%

ENVX -9.2%, post earnings upset. Cowen, 11>12

–

EXC +2.6%, EPS 60cents vs 58est. Rev’ y/y +15.0% to $5.4bn vs 3.9est. Guidance inline. Divi +5.6% to 38cents

–

FTNT -6.9%, in sympathy with Palo Alto

–

GLBE -13.5%, EPS -13cents vs -12est. Rev’ y/y +32.5% to $185M vs 182est. Weak guidance.

–

GRMN +4.7%, EPS $1.72 vs 1.40est. Rev’ y/y +13.3% to $1.48bn vs 1.41est. Mixed guidance. Divi’ 75cents. $300M buyback

–

HD -0.8%

HSBC -7.5%, post earnings upset

–

MED -10.3%, post earnings horror

MSFT -0.7%

NEM +0.3%

–

NVDA -1.7%, earnings due in AH

PANW -23.4%, post earnings horror

–

PLAB -13.0%, EPS 48 cents vs 49est. Rev’ $216M vs 220est.

–

PLTR -3.3%

SEDG -20.0%, post earnings horror

SMCI -3.1%

TDOC -21.3%, post earnings horror

–

TOL +2.4%, post earnings gains

TSLA -0.5%

UAL -0.4%

–

UBER -0.1%, Uber to join the Dow Trans’20 index… replacing Jetblue (JBLU). Taking effect early Feb’26th. > https://en.wikipedia.org/wiki/Dow_Jones_Transportation_Average

–

UEC -4.9%

UNG +10.6%, with Natgas $1.75

–

VIX +3.6% at 15.98

–

VRT -10.6%, EPS 56cents vs 53est. Rev’ y/y +12.7% to $1.87bn vs 1.88est. Weak guidance.

–

WBA -2.4%, kicked OUT of the mighty Dow!

–

WING -4.5%, EPS 64cents vs 57est. Rev’ $127M vs 120est. UBS, neutral, 280>330

–

WIX +5.7%, EPS $1.22 vs 0.96est. Rev’ y/y +13.7% to $404M vs 403est. Guidance inline.

–

WMT +0.5%

ZS -9.5%, in sympathy with Palo Alto

—

Overnight markets

Asian and European markets were mixed…

Japan: -0.3% to 38262

China: +1.0% to 2950

Germany: currently +0.5% at 17153

UK: currently -0.8% at 7659

—

Have a good Wednesday