Good morning. US equity futures are significantly higher, SPX +65pts, we’re set to open at 5046. USD is -0.3% at DXY 103.61. The precious metals are leaning upward, Gold +$4, with Silver +0.7%. WTIC is -0.4% in the $77s.

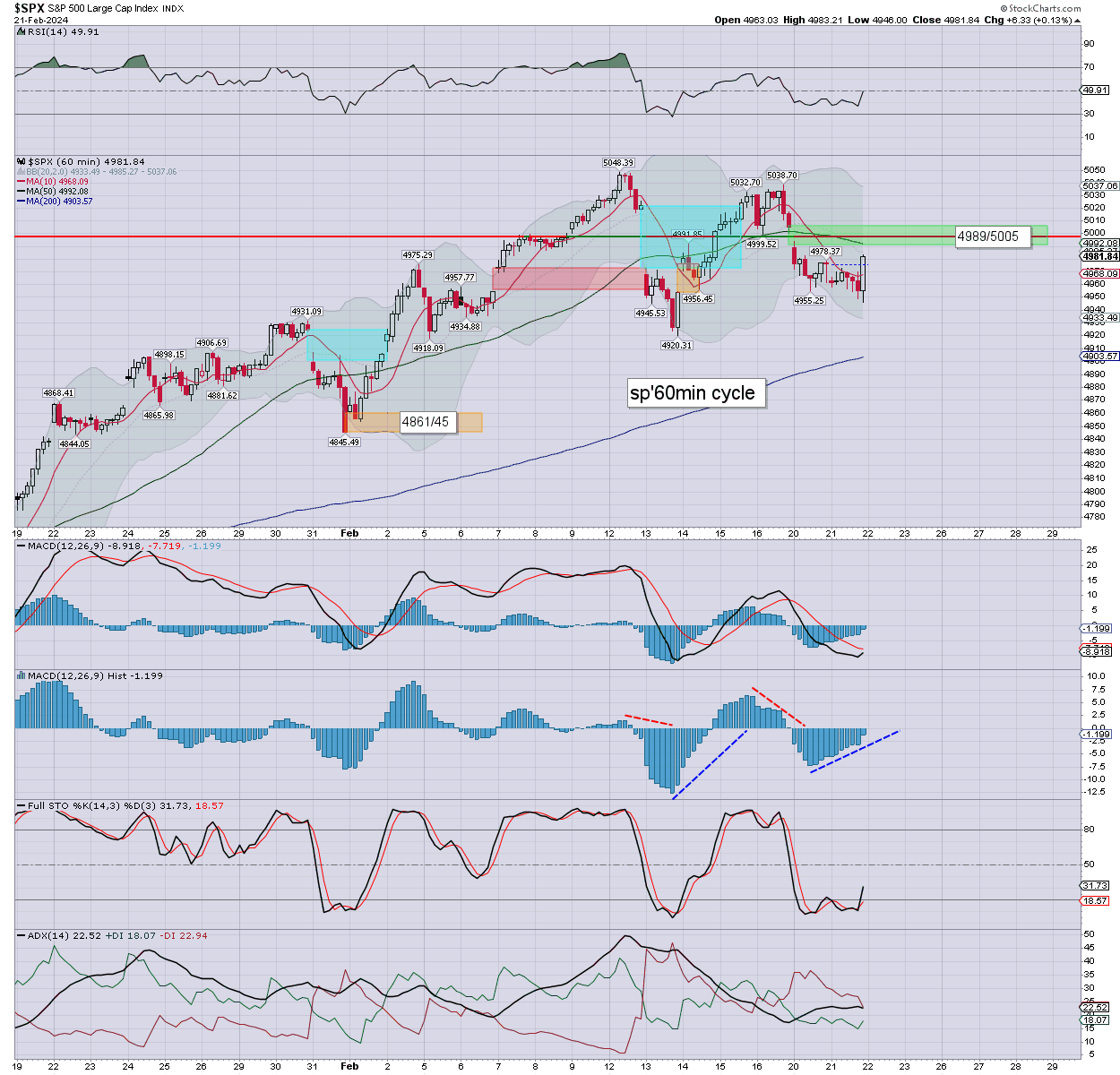

sp’60min

Summary

Wednesday saw considerable chop, if mostly weak leaning. The closing hour saw a distinct upside reversal, settling (surprisingly) positive… if only fractionally.

Overnight futures have been distinctly positive, helped by other world markets, but it would seem… especially Nvidia.

S/t momentum will turn positive at the open. The SPX will be prone to printing a new hist’ high (>5048), making it a day and week for the bulls. A push into the 5100s is clearly viable before end month.

Call it AI hysteria, call it a ‘blow-off top’, call it whatever you like, but such a new hist’ high, will keep things at effectively 100% bullish, with spring due in just four weeks.

—

Early movers

AAPL +0.5%, distinctly laggy to the main market.

–

AG +1.6%, EPS **

–

AMD +5.3%, helped by Nvidia

AMZN +2.0%

–

APA -1.8%, earnings (Wed’ AH), EPS $1.15 vs 1.33est. Rev’ y/y -12.3% to $2.17bn vs 2.07est.

–

ARM +6.1%

BROS +6.7%, post earnings jump

CCL +5.2%, helped by RCL

–

COIN +3.0%

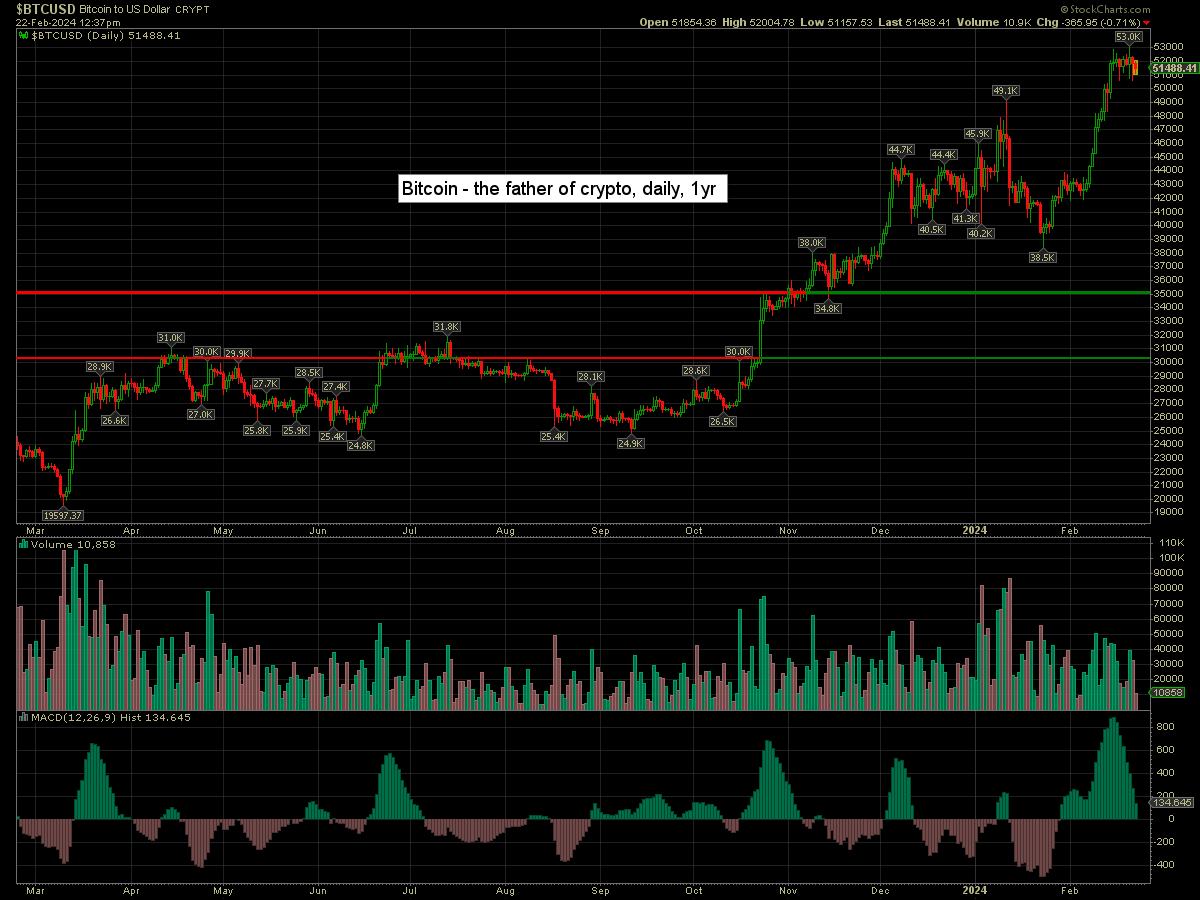

Bitcoin is -0.7% at $51488. Every day is can hold >50K, increases the probability it will make a broader push to next resistance of $61K.

–

CRWD +4.6%… as everything is fine again, with most already forgetting about Palo Alto.

–

ETSY -7.9%, earnings (Wed’ AH), EPS 62cents vs 78est. Rev’ $842M vs 827est. Warns Q1 sales will be weak.

–

ENVX +3.0%

FCX +0.3%, with copper +1cent to $3.88

–

FVRR -2.7%, EPS 56cents vs 48est. Rev’ y/y +10.1% to $91.5M vs 92.6est. Weak guidance.

–

GOLD +0.3%

INTC +2.5%

–

LCID -8.4%, EPS -29cents vs -30est. Rev’ y/y -39% to $157M vs 180est. Lucid make 2391 vehicles in Q4, 8428 full year. Guides for 9K vehicles (full year)

–

LNG -1.2%, EPS $5.76 vs 2.69est. Rev’ y/y -46.9% to $4.8bn vs 4.4est. Lower Natgas prices sure didn’t help.

–

META +2.4%

–

MOS +3.7%, earnings (Wed’ AH), EPS 71cents vs 87est. Rev’ y/y -29.7% to $3.15bn vs 3.09est.

–

MRVL +6.0%

–

MRNA +4.8%, EPS 55cents vs -93est. Rev’ y/y -44.9% to $2.8bn vs 2.5est. Maintains guidance. Moderna expects regulators to soon authorise the RSV shot.

–

MSFT +1.7%

–

MU +2.9%, all those NVDA and AMD graphics cards require a lot of memory chips

–

NEM +0.1%, EPS 50cents vs 44est. Rev’ y/y +23.7% to $4.0bn vs 3.4est. Newmont is looking to sell six ‘non-core projects’.

–

NVAX +8.0%, Novavax reaches a settlement with Gavi

–

NVDA +13.2%… printing $775, a new hist’ high, with the market cap’ nearing $2trn.

Earnings (Wed’ AH): EPS $5.16 vs 4.59est. Rev’ y/y +265% to $22.1bn vs 20.1est. Positive guidance

–

PLTR +5.8%

RCL +5.7%, updated guidance

–

RIVN -15.7%, earnings (Wed’ AH), EPS -$1.36 vs -1.35est. Rev’ y/y +98% to $1.3bn inline. Rivian guides for 57K vehicles for the year, touting a Q4 2024 ‘modest gross profit’. Emphasis on the GROSS… not net, as I struggle to see Rivian surviving.

–

SMCI +11.4%, renewed hysteria

SQ +2.8%, earnings due in AH

–

TLT +0.3%, as yields cool

TSLA +0.5%

TSM +3.6%

UAL +0.7%

UBER +2.5%

–

VIX -7.4% at 14.21

–

W +6.2%, EPS -11cents vs -15est. Rev’ y/y +0.4% to $3.1bn inline. I struggle to see a l/t future for Wayfair.

–

WBD +1.0%, earnings due early Friday

—

Overnight markets

Asian and European markets all pushing upward…

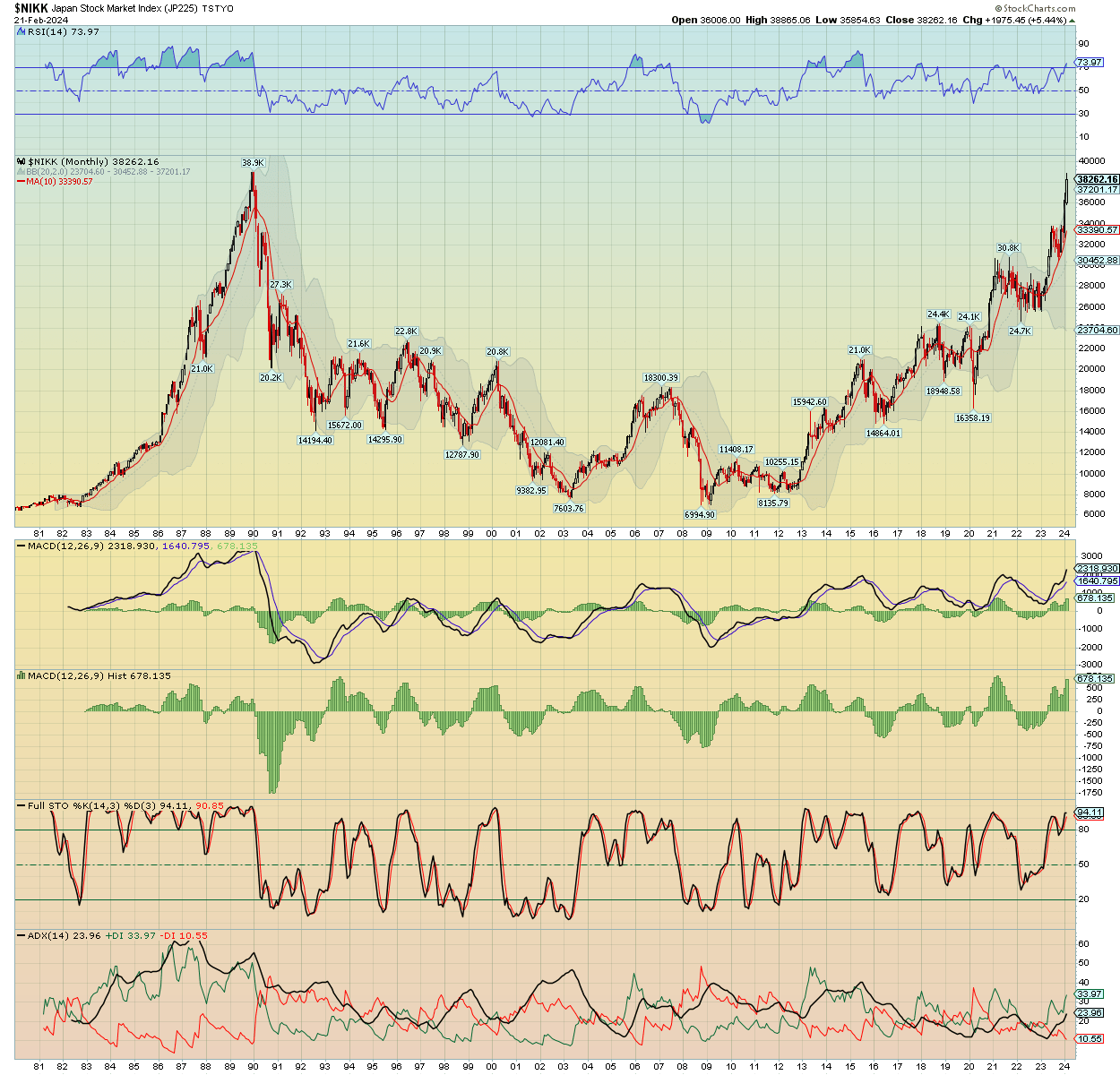

Japan: +2.2% to 39038, a new hist’ high, finally clearing the 1990 high of 38915

—

—

China: +1.3% to 2988

Germany: currently +1.4% at 17353

UK: currently +0.2% at 7679

—

Have a good Thursday