Good morning. US equity futures are broadly flat, SPX -1pt, we’re set to open at 4941. USD is +0.05% at DXY 104.38. The precious metals are a little mixed, Gold u/c, with Silver -0.4%. WTIC is +0.5% in the $73s.

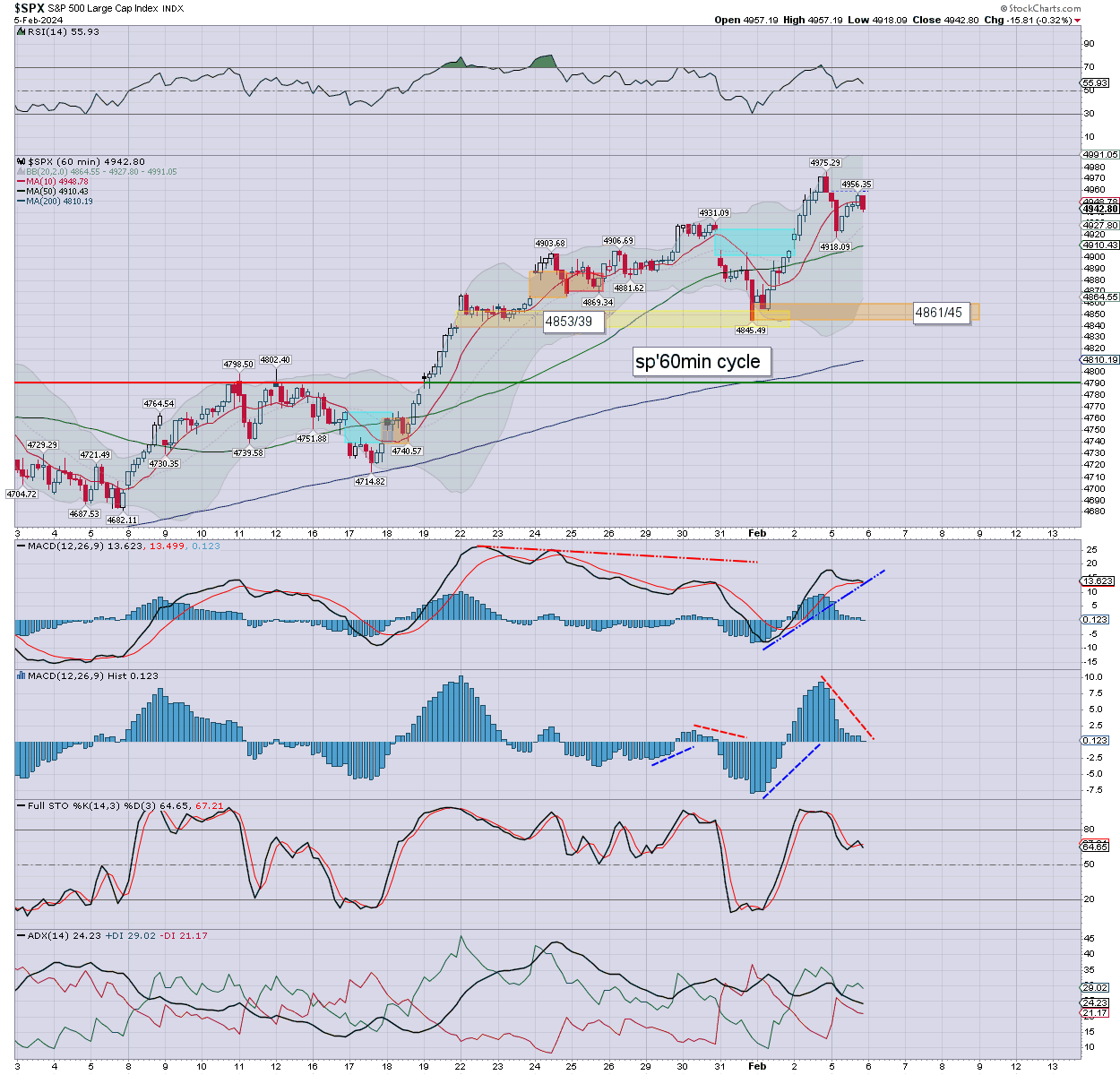

sp’60min

Summary

Yesterday saw morning weakness, with a latter day recovery, if settling on the weaker side. S/t momentum settled fractionally positive.

Overnight futures have been subdued, we’re set to open broadly flat. S/t momentum is due to turn negative, and will likely be a pressure into at least late morning.

—

Early movers

AMD -1.1%

AMGN +1.3%, earnings due in AH

–

AMKR -5.5%, post earnings depression

AMZN -0.7%

BABA +3.1%, bouncing Chinese stocks.

CHGG -7.2%, post earnings depression

–

COIN -0.1%

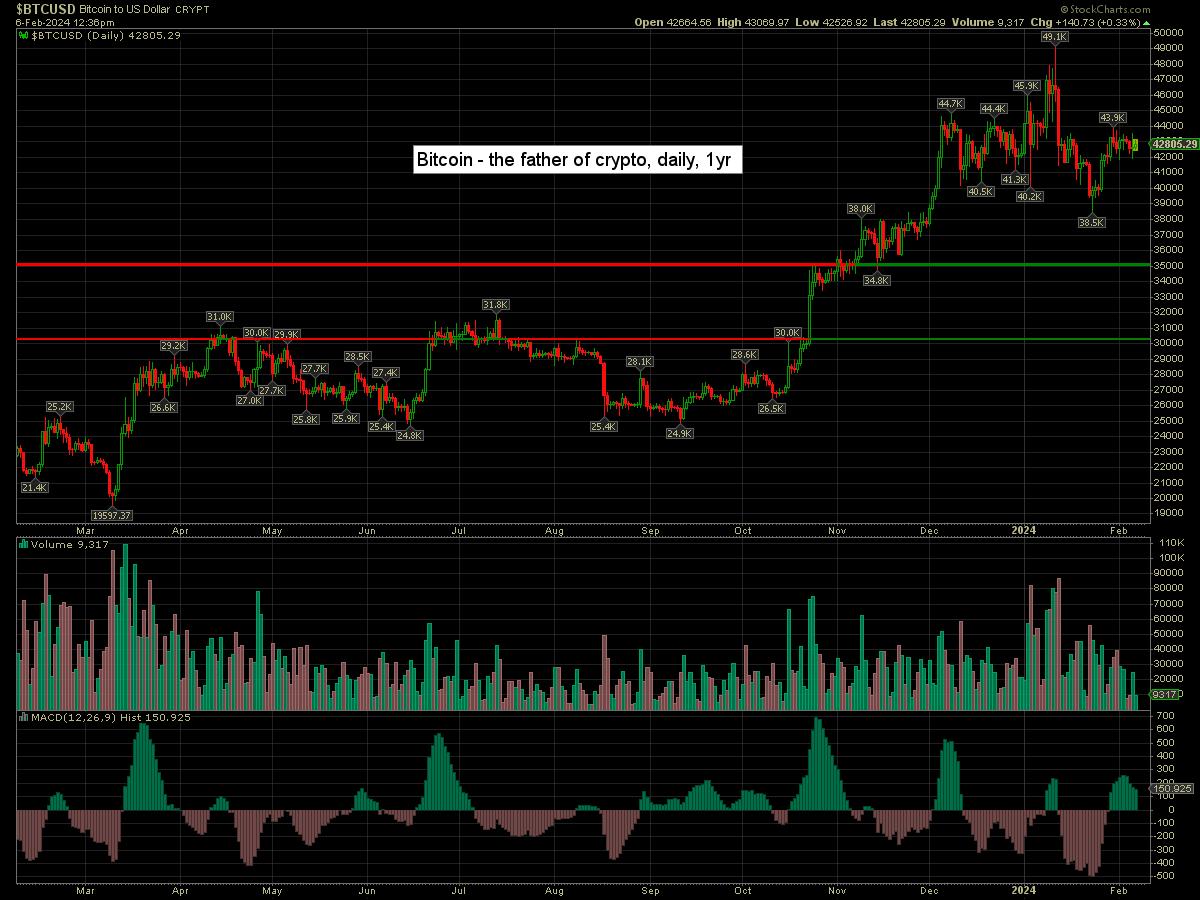

Bitcoin is currently +0.3% at $42805

–

CSCO +1.3%, Cisco partnering with Nvidia for AI

–

DIS +0.4%, Blackwells pushing board members, and argues for the company to be split. Earnings due Wed’ AH

–

FMC -13.6%, earnings (Monday AH), EPS $1.07 vs 1.08est. Rev’ y/y -29.3% to $1.15bn vs 1.24est. Weak guidance.

–

GEHC +3.3%, EPS $1.18 vs 1.07est. Rev’ y/y +5.3% to $5.2bn vs 5.1est. Guidance inline

–

GOLD +0.4%

–

HTZ -7.5%, EPS -$1.36 vs -1.05est. Rev’ y/y +7.3% to $2.18bn vs 2.15est. The relisted Hertz still can’t make money.

–

INTC -0.5%

JD +5.4%, bouncing Chinese stocks.

–

LLY +4.2%, EPS $2.49 vs 2.30est. Rev’ y/y +28.1% to $9.3bn vs 8.9est. Positive guidance on hopes of weight loss drug sales (I refer you to the video by Denniger last evening)

–

NEM +0.3%

NIO +4.1%, bouncing Chinese stocks

NVDA +0.4%

–

NXPI +3.0%, earnings (Monday AH), EPS $3.71 vs 3.65est. Rev’ y/y +3.3% to $3.4bn inline. Guidance inline.

–

OXY +0.6%

PLTR +16.7%, post earnings jump

PYPL +0.5%, earnings due Wed’ AH

RMBS -10.4%, post earnings upset

SLB +0.5%

–

SPOT +7.0%, EPS €-0.36 ($0.39) vs -1.40 prior yr. MAUs y/y +23% to 602M…. of which Premium subs, y/y +15% to 236M. All these years… and Spotify still can’t turn a profit.

–

SYM -17.0%, post earnings horror.

–

TSLA -2.6%, Piper Sandler, overweight, 295>225, Daiwa, outperform>neutral, $195

–

TM +3.7%, post earnings gains

–

UBS -4.1%, EPS -9cents vs +9est. Rev’ y/y +35.2% to $10.9bn vs 10.6est. Company touting buybacks to resume in H2 of 2024.

–

VIX +0.4% at 13.73

–

XOM +0.4%

—

Overnight markets

Asian markets were very mixed, whilst European markets are a little mixed…

Japan: -0.5% to 36160

China: +3.2% to 2789

Germany: currently -0.1% at 16894

UK: currently +0.5% at 7653

Here in the failed state of the UK…

https://www.bbc.co.uk/news/business-68204358

EV van maker Arrival (ARVL)… collapses.

Just three years ago it was valued at $13bn

Fines for companies not meeting ‘Heat pump’ targets might be dropped…

https://www.bbc.co.uk/news/uk-politics-68207355

With regime leader Sunak arguing that ‘cost of living’ pressures are easing…

https://www.bbc.co.uk/news/business-68204195

You can argue the rate of inflation has declined, but prices are still higher than last year, with the UK/western consumer increasingly broken.

—

Have a good Tuesday